Losing Control?

Stocks in the US ticked higher on Monday, building on the last week’s gains as investors braced for a week packed with key earnings reports and the Federal Reserve’s rate decision.

The S&P 500 and the Nasdaq added 0.3%, the Dow gained 148 points.

Tesla shares soared by 15.8%, leading the gains for tech mega-caps after the company received the approval of Chinese authorities to deploy its driver-assistance system.

Earnings season will reach its zenith with reports from heavyweight Amazon, Eli Lilly, Coca-Cola, McDonald's, Mastercard, Qualcomm, Pfizer, ADP, Apple, ConocoPhillips, Amgen, Booking, and Cigna.

Among mega caps, Apple and Amazon added 2.5% and 0.7%, respectively.

We're halfway through Q1 earnings season.

In a quarter that is expected to be the weakest quarter for earnings growth we will see all year, thus far, earnings growth is in-line with Wall Street's 3%+ growth expectations.

FactSet has full year S&P 500 earnings growth at 10.8%. Excluding the "re-opening" bounceback in corporate earnings in 2021, this year is projected to be the hottest earnings growth since 2018.

That's despite the swing in rate expectations, from anticipating an aggressive easing campaign from the Fed (earlier this year), to (now) maybe no easing.

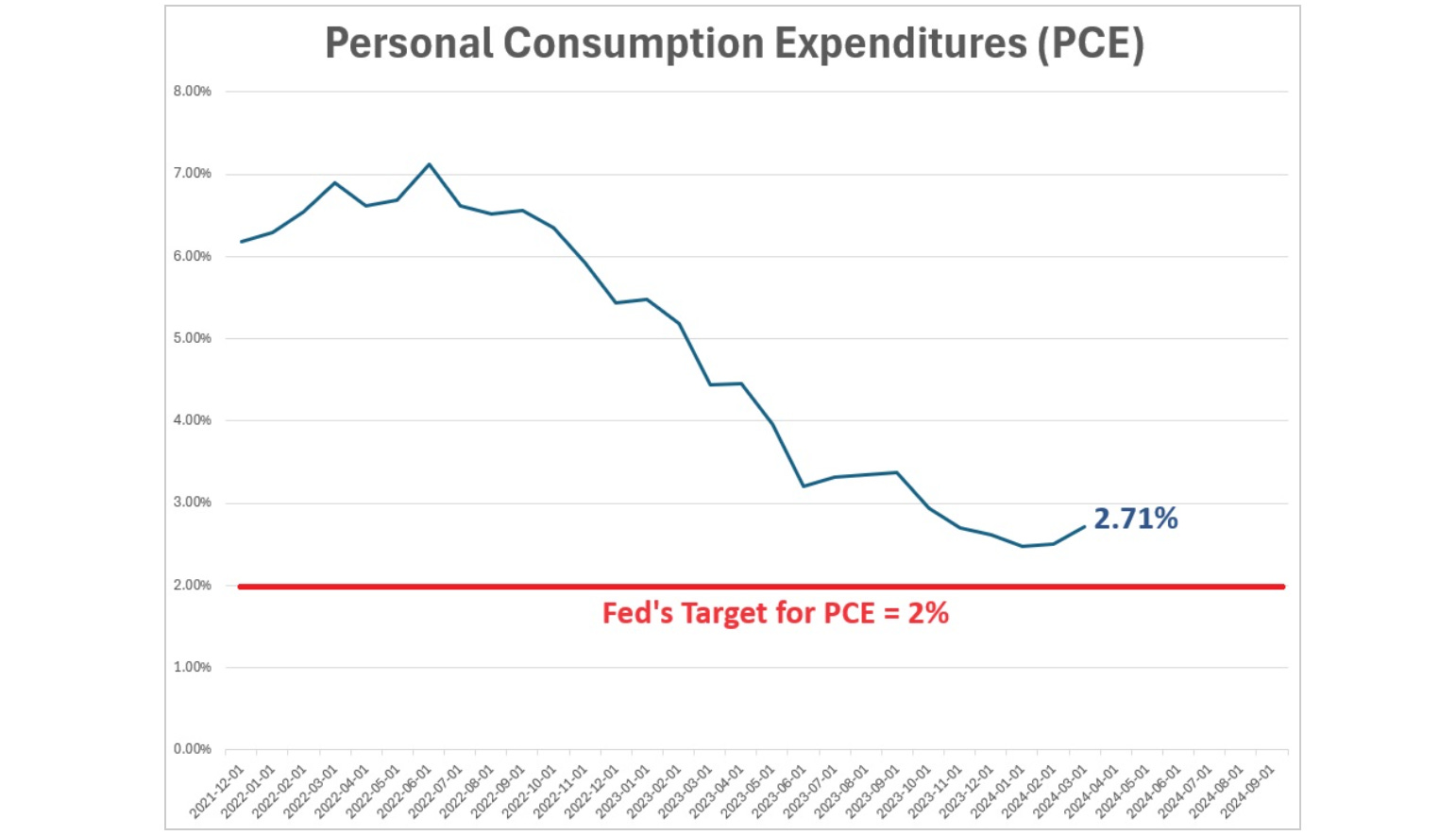

With that, the Fed meets this week. Here's the latest look at the Fed's inflation barometer, PCE.

So inflation is 71 basis points away from the Fed's target. But the Fed has the Fed Funds rate (still) 262 basis points ABOVE the rate of inflation. That's historically very, very tight monetary policy. And yet the market is only pricing in one full rate cut by year end.

That rate outlook has the 2-year yield trading back to 5% … the 10-year yield back to early November levels (as high as 4.74% last week) … and has influenced a negative surprise in Q1 GDP growth (under 2% growth).

With that backdrop, Jerome Powell should be talking down the interest rate market on Wednesday, attempting to move the rate expectations pendulum back toward the middle.

After all, it's the Fed's manipulated wide interest rate differential between the U.S. and Japan that has driven sharp declines in the yen.

A weak yen is intentional and works in Japan's favour - inflating away debt, and increasing export competitiveness. It's by design - the BOJ (and Fed) monetary policy. But they can't risk losing control (i.e. a rapid decline in the yen). So, to slow the pace of the yen decline, the Bank of Japan was forced to intervene in the currency markets to support the yen.

With that, if the Fed needed a nudge on "messaging dovish" on Wednesday, this BOJ action should be the nudge.

Gryning is Designed for Decision Makers.

Hedge fund managers, asset allocators, family offices, individual investors, and those who need leading research on where the market is going. Our research is technical and uniquely personalised for investors.

For team/group discounts on annaul memberships, shoot me an email: a.karlsson@gryningcapital.com