A Big Deal

Stocks in the US finished a choppy session lower on Tuesday, as investors awaited signals from the Federal Reserve on future interest rate cuts.

The S&P 500 and Nasdaq 100 snapped an eight-day rally, closing 0.2% lower each, and the Dow Jones lost 61 points.

Energy and material stocks were among the worst performers, while health and consumer staples gained the most.

In corporate news, Lowe's fell 1.2% after missing revenue expectations and lowering its profit outlook, despite beating Q2 profit estimates.

Boeing dropped 4.2% after grounding its 777x test fleet due to structural cracks.

As we discussed yesterday, when Jerome Powell speaks in Jackson Hole on Friday, markets will be looking for a signal that the Fed will begin the easing cycle in September - the Fed has told us they are watching the job market “carefully” for “cracks” as a condition to start the easing cycle.

With that, we've talked about the rapid rate-of-change in the unemployment rate, which should constitute a clear "crack."

The unemployment rate is up 9/10ths of a point above the cycle low (3.4%) of just 15 months ago. The speed of this change in joblessness puts it in the unique company of the past four recessions (which came with, in each case, reactionary Fed rate cuts).

Add to this, over the past forty-eight hours, there have been reports suggesting the Bureau of Labour Statistics (BLS) will make a big downward revision in the monthly job creation data due this morning.

In this scheduled annual "benchmark revision" by the BLS (i.e. a one-off annual adjustment), Goldman Sachs thinks they could subtract as many as a million jobs from the job creation picture.

This is a big deal.

As we've discussed over the past three years, the Biden BLS already has a record of making large revisions in the jobs data which have led to very consequential misreads on the health of the economy by policymakers.

Let's revisit some analysis from my January 8th note earlier this year, where we stepped through the big revisions made in 2021 and in 2023.

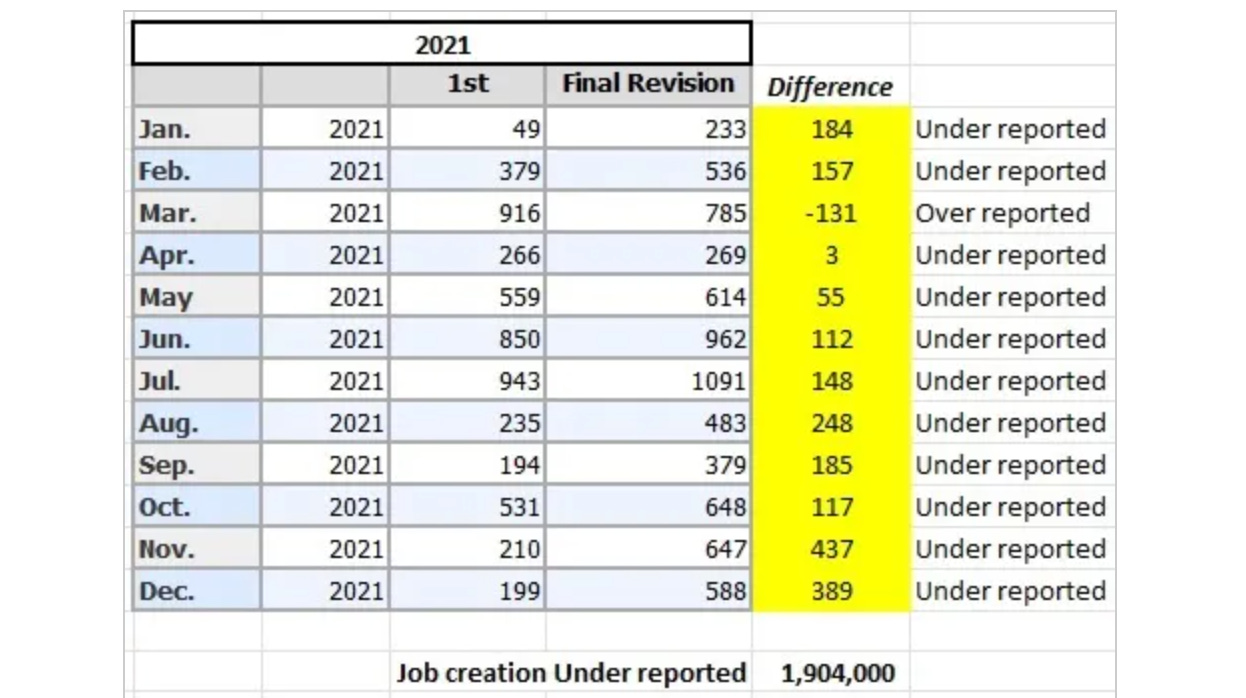

Here's a look at 2021 …

As we know, the inflation fire was burning in 2021, driven by the textbook inflationary ingredients of a massive boom in the money supply. Yet the Fed continued its emergency monetary policies all along the way (zero rates + QE), dismissing the rise in prices as "transitory."

And Congress used the Fed's assessment to rationalise even more fiscal spending (more fuel for the inflation fire).

How could the Fed justify its claim that inflation was "transitory?" A relatively modest job market recovery.

But as you can see in the table above, it turns out that the BLS revised UP eleven of the twelve months of nonpayroll numbers in 2021. After the revisions, it turns out the initial monthly reports UNDER reported job creation by 1.9 million jobs for the full year.

The economy was a lot hotter than the Fed thought.

As we know, the Fed was wrong on inflation, and well behind the curve in the inflation fight.

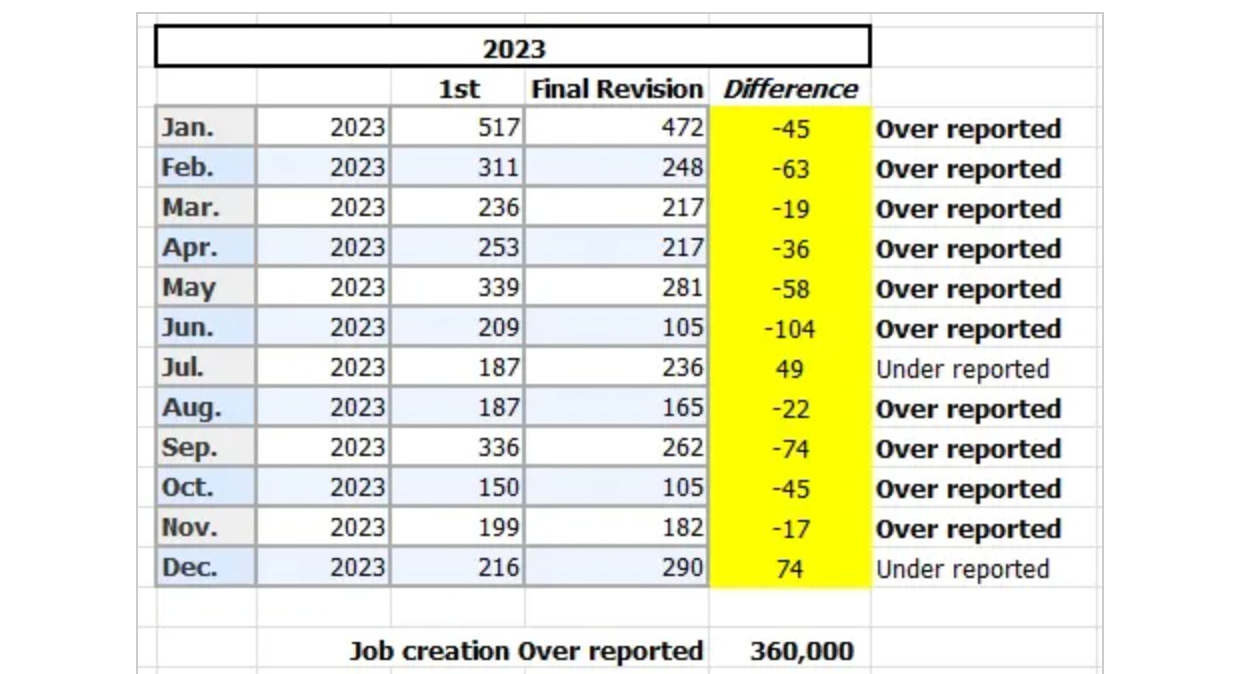

Now, let's look at 2023 …

Remember, the Fed continued raising rates through July of last year. And along the path of its tightening campaign, the Fed was explicitly trying to slow the job market.

What did the BLS do along the way?

They OVER reported job creation. As you can see in the table above, through November, the BLS revised DOWN ten of the twelve months of payroll numbers in 2023.

The job market was not as hot as the Fed thought from initial reports.

And this snapshot on the labour situation could become much dimmer with a large downward revision.

It's funny, the more I observe Powell and the Fed, the more I've come to believe that they have a plan regardless of the data and are only using the data to support their plan. given that the data has been remarkably mixed, with both strong and weak economic indicators printing regularly, depending on what they want to highlight, they have support. if they really want to cut, then today's revisions will help the case. but if they don't they can simply look at the recent trend in Initial Claims and highlight their decline supports a stronger labor market and the revisions are very backward looking