You can check out, but you can never leave...

Macro Perspectives

The historical track record of QE exits is not good. We know that in each case (globally and domestically), the "quantitative tightening" experiments ended with...more QE.

In my note last month, I posed the question of whether the Fed will even get the opportunity, this time, to start the process of "normalising" the Fed balance sheet (i.e. quantitative tightening)? We know the Fed formally announced their intentions in its meeting last week. But with the start date set for June 1, and the air quickly coming out of the QE sponsored tech-stock and crypto bubbles, they may be back to damage control by June 1.

But it won't be because of stocks. It will likely be because of the side-effects of QT (the unwind of the tech bubble, related).

Without question, all along the path of the post-financial crisis, the Fed has wanted and needed stocks higher (and they behaved accordingly). Higher stocks drove the wealth effect, and confidence, and that underpinned demand, in a world of weak demand (following the very long, slow recovery from the debt-induced financial crisis).

This time, the Fed is explicitly trying to slow demand, to align with supply disruption (though much of it is by the design of bad government policy-making).

With that motivation (slowing demand), they are probably quite satisfied with the quick haircut in the stock market - particularly, the high flying, high valuation, high speculation tech sector. It will slow the animal spirits, and therefore the 'rate of change' in prices (inflation).

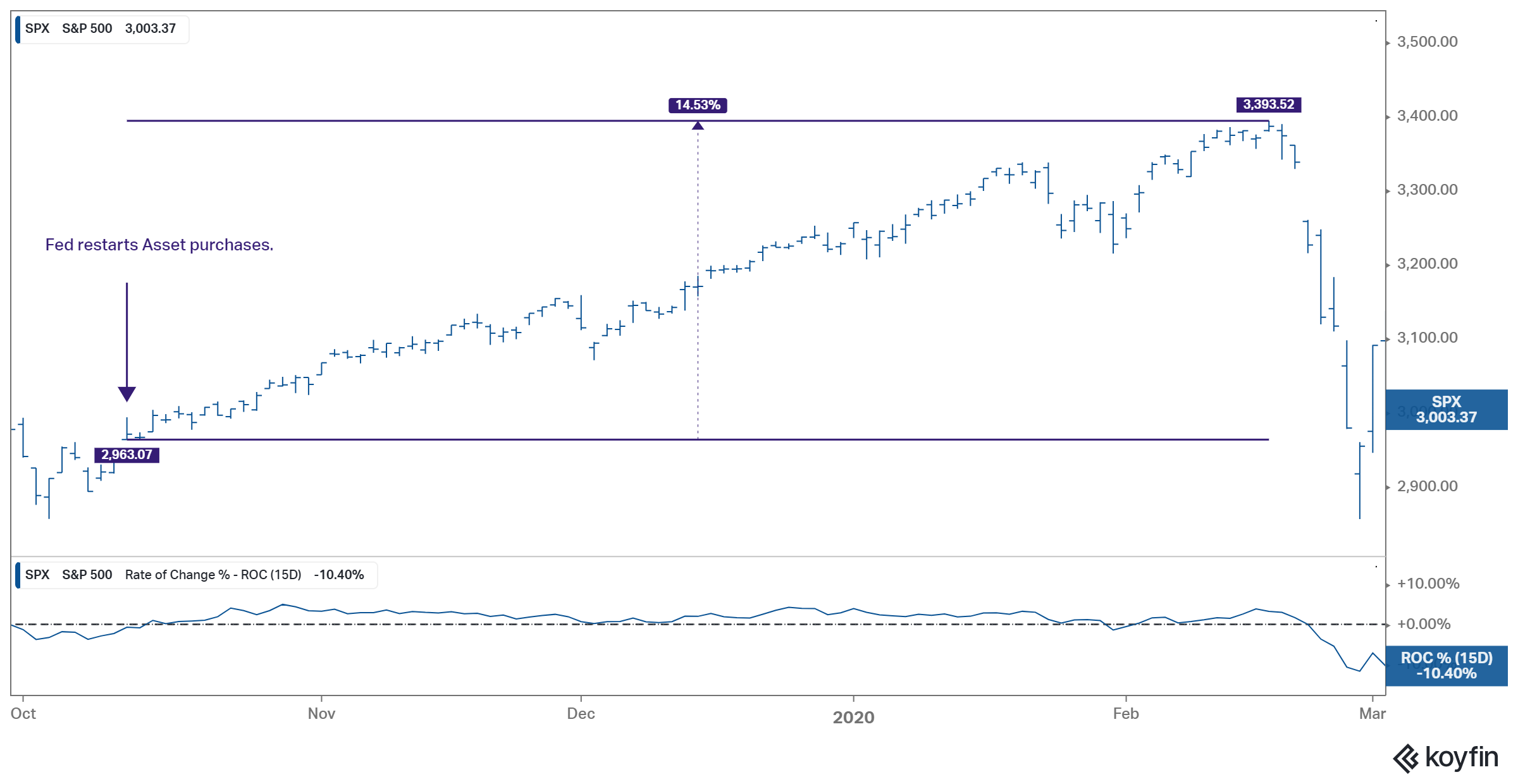

However, putting the QE genie back in the bottle doesn't have a good record. Unforeseen consequences tend to arise; after spending eighteen months shrinking the balance sheet (2017-2019), the Fed quietly started reversing course in late 2019. By the time Jay Powell acknowledged it, in a prepared speech (in October of '19), they had already bought $200 billion worth of assets.

This was a response to what they called "strains in the money market." Things started breaking, and interestingly, the Fed refused to call the resumption of balance sheet expansion "QE." Nevertheless, here's how stocks responded to the stealth QE of late 2019...up 15% in a near perfect 45 degree angle in 4 months(...then covid lockdowns, and the response: more QE).

As much as the Fed might like to move on from QE, from what we know of it, QE is "Hotel California."

"You can check out, but you can never leave."

Again, it highlights the eventuality of a reset of global debt, and a new monetary system.