Yields Rising, Stress Rising, Chances of Intervention Ris...

Macro Perspectives

Friday's report on core PCE was good. As with the broader inflation data we've seen lately, the path lower continues.

The monthly change in core PCE was just +0.14% - that's the slowest monthly rate of change in prices in three years (since late 2020). If we annualize the data of the past three months, the Fed's favored inflation gauge comes in just above the Fed's target of 2% (2.16%, to be precise).

So, that's good news.

How did the bond market respond. Yields fell sharply to start the day on Friday, but reversed into the end of the day.

That was bad news.

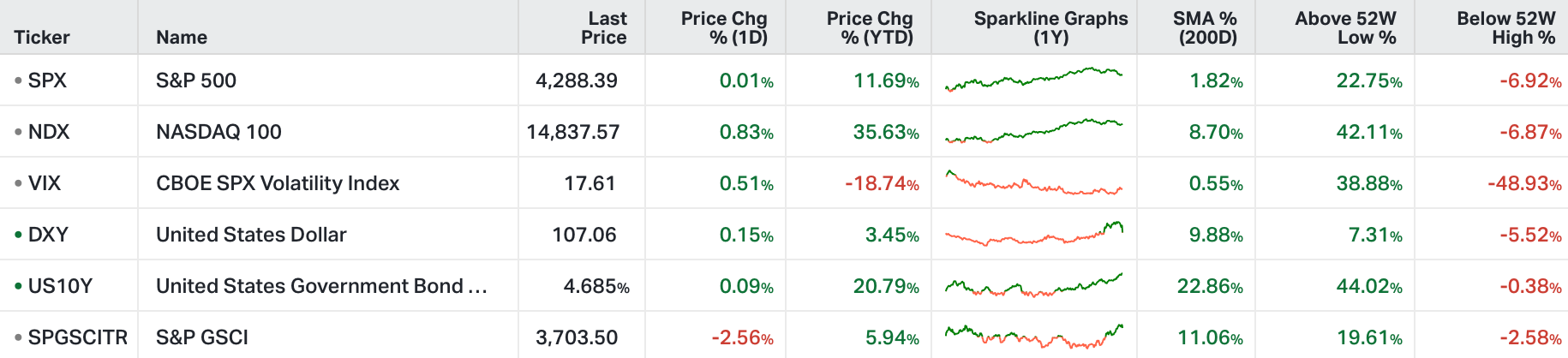

With that, not surprisingly, yields continued to push higher yesterday, to open the week - we now have the U.S. 10-year yield on 16-year highs, and this chart . . .

As we discussed last week, with record global government indebtedness, this level in the benchmark U.S. interest rate market puts high stress on the domestic and global economy.

This interest rate anchor (the U.S. 10-year yield) pulls global government bond yields higher.

In Europe, German 10-year yields are approaching 3%, Spanish yields near 4% and Italian yields toward 5%. This is unsustainable territory for these weak spots in the euro zone (Spain and Italy) to service debt. With that, the future of the common currency (the euro) comes into question. Indeed, the euro is looking vulnerable to another run toward, and below, parity versus the dollar.

Add to this, let's take a look at the chart of U.S. investment grade corporate debt, as a barometer of stress . . .

The highest volume corporate bond ETF, LQD, is trading at levels that have coincided with some form of intervention. That intervention, of course, in the recent history of this chart, has resulted from extreme stress and uncertainty in global financial markets (namely, disconnected government bond yields).