When the Fed...

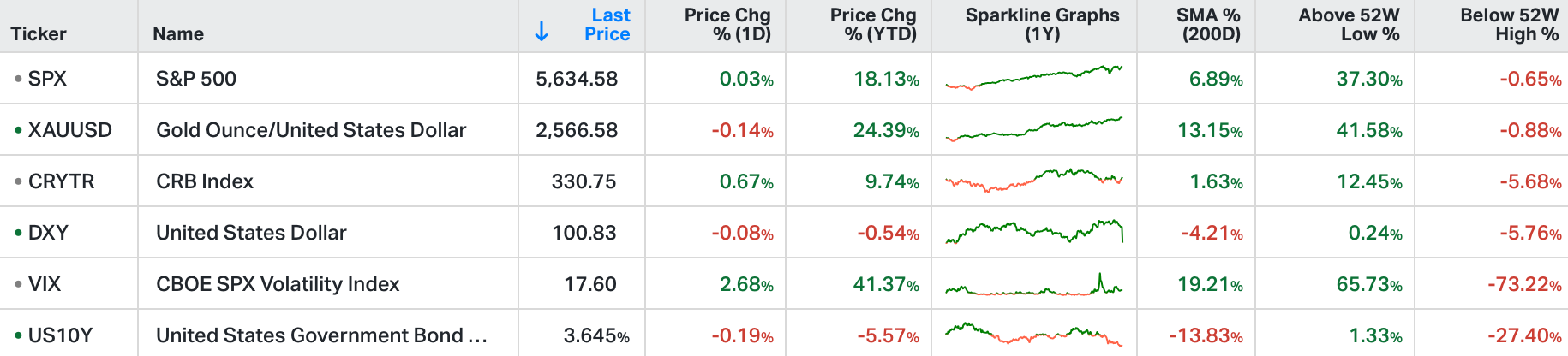

Stocks in the US were little changed on Tuesday, as uncertainty mounted about the size of the anticipated rate cut.

The S&P 500 and the Dow Jones finished muted after both hit records, while the Nasdaq edged higher by 0.2%.

Still, investors remain divided on the size of the reduction, with the odds for a jumbo 50bps cut currently standing above 60%.

Among mega cap companies, Nvidia fell 1.1%, while Microsoft was up 0.9% after the company raised its quarterly dividend.

Intel rose 2.6% following the chipmaker's new business partnership with Amazon.

With the Fed due to officially kick off an easing cycle today they will do so well behind the curve, with the Fed Funds rate sitting 283 basis points ABOVE the rate of inflation (PCE).

But the interest rate market has already determined where rates should be.

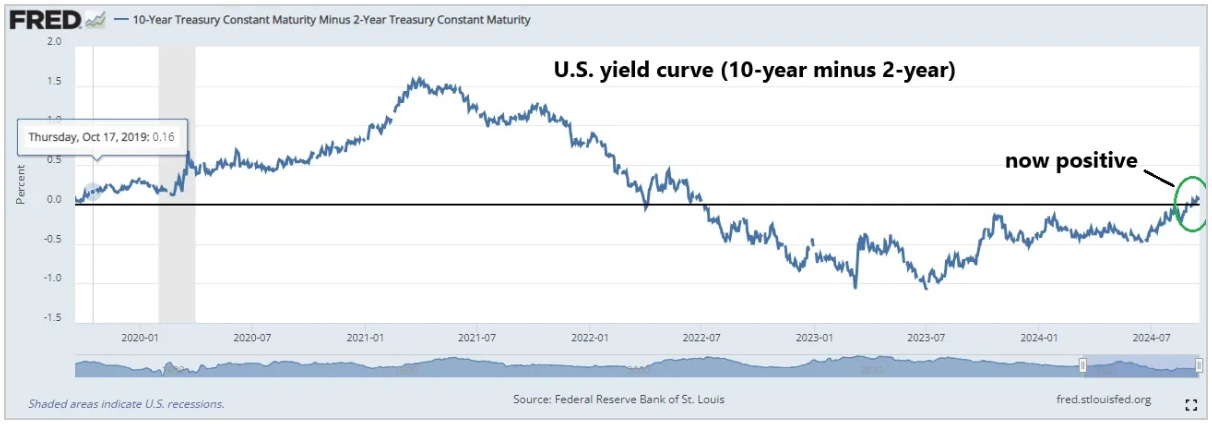

Since Jerome Powell signalled the end of the tightening cycle in October of last year, the 10-year yield (the market determined interest rate) has fallen by 140 basis points.

Moreover, with the even sharper plunge in the 2-year yield (down 166 basis points since last October) the yield curve has returned to a positive slope, after two years of inversion.

And as we've discussed here in my daily notes, yield curve inversions are historically predictors of recession - when the curve turns positive again, it tends to indicate an economy has either entered or is about to enter recession.

That said, while market interest rates have adjusted, consumer interest rates have been slow to follow.

The average 30-year fixed mortgage rate is now at 6.2%. If we look back at the historical spread between mortgages and the 10-year yield, it should be closer to 5.4% (or lower).

Average credit cards rates are 17 percentage points above the 10-year yield. It's historically closer to a spread of 10.

Auto rates? Those are running about 300 basis points above the long run average spread to the 10-year.

Maybe these spreads will finally start narrowing when the Fed proves that it will indeed kick off the easing cycle, after a lot of talk.