What’s Not To Like?

Stocks in the US finished higher on Friday, as the S&P 500 and the Nasdaq added 0.2% each, the Dow Jones gained 96 points, building on Thursday’s strong rally.

A busy week of economic data helped the market's recovery from earlier losses in August.

Additionally, investor sentiment was boosted by signals from Federal Reserve officials suggesting a possible rate cut in September, sustaining the week's momentum.

Communication services and the financial sector led the gains of the session while real estate dragged the most.

GRYNING | Signals can help you navigate the complexities of the financial markets and achieve your investment objectives.

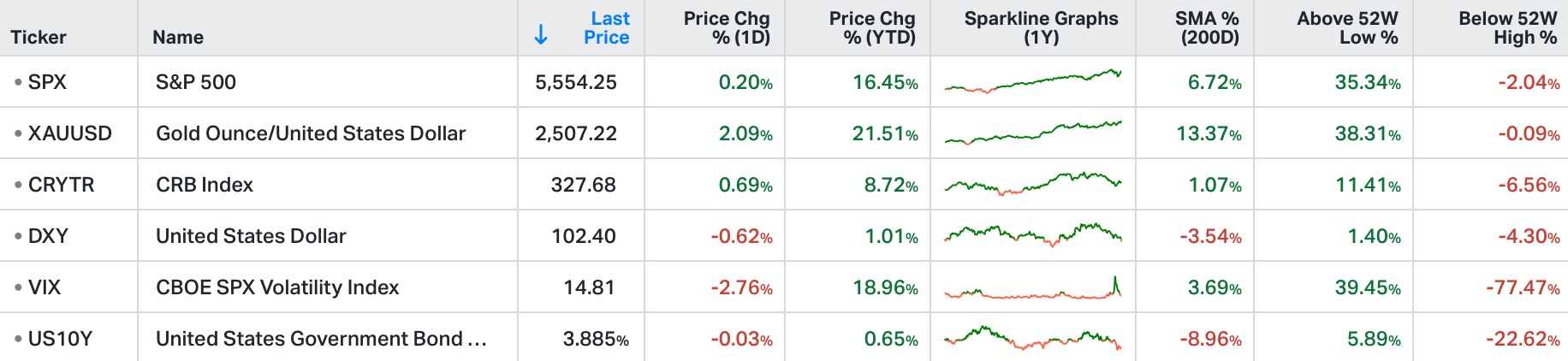

The market is resilient.

It digested a $20 trillion yen carry trade crisis in three days last week - the S&P 500 is back to within 2.7% of its all-time high.

The economy is expanding - the Atlanta Federal Reserve Bank is forecasting 2.9% real GDP growth in the third quarter.

Earnings and revenues were better than expected for the second quarter. With over 90% of the S&P 500 having reported, revenue growth was 5.2% and earnings growth was 10.8% versus expectations of 4.5% and 8.5%. Consensus estimates for S&P 500 earnings next year are now $280, up from about $275 at the start of 2024.

According to the Producer Price Index (PPI) and the Consumer Price Index (CPI) reports last week, the disinflation trend is moving in a direction necessary to drive a rate cut by the Federal Reserve in September. The Fed Funds Futures market shows the probability of at least a 0.25% rate cut in September is 100%.

Core retail sales were up 0.4% month-over-month in June. Retail sales outpaced the rate of inflation, suggesting increased sales were driven by increased demand in addition to higher prices.

Walmart (WMT) reported better than expected earnings and raised FY 2025 guidance. U.S. comparable store sales were up 4.2%. The stock jumped 8% on the news to an all-time high. Solid levels of discretionary spending undermine recession concerns.

The primary market concern seems to be with seasonality. The chart below shows the two worst months of the year for the market on average since 1995 have been August and September.

Other concerns involve rising unemployment, rising consumer debt, delinquencies, and a potential slowdown in consumption by lower-end consumers. It is not clear if any of these concerns are the result of emerging trends or if the data is both volatile and normalising. Walmart’s management specifically said they do not see a deterioration in spending by their customers and initial jobless claims decreased for the second week in a row.

The S&P 500 is about where it was at the start of the month. Given that the volatility index (VIX) reached its third all-time highest reading at the start of the month, the recent price action of the S&P 500 is a victory for bullish investors.

Let GRYNING | Signals Help You Grow Your Portfolio – Become a Member today.

At Gryning, we pride ourselves on our unique and sophisticated investment strategies designed to capture the gains of the stock market while minimising drawdowns during bear markets. If you're seeking expert guidance in your trading and investment portfolio’s, we're here to assist you.

here's my question, according to the BIS' latest triennial survey, average daily volume in JPY, across all products, is ~$1.2 trillion. why does anybody think that the carry trade was closed out in the course of 3 days? it took at least 2 years to build it up, from the time the Fed started hiking rates. and spot USDJPY was 115 or so when it started. while late players to the game may have been caught out, I would contend there is still trillions left in place.