This is for traders and portfolio managers who want to hit the ground running with access to robust, institutional-grade daily, weekly, and monthly signals and trading strategies. Below is a list of offerings:

Market Signals for Position Traders

We use six quantitative strategies to generate systematic trading signals with precise entries and exits in the weekly timeframe. The strategies cover price series and cross-sectional momentum, mean reversion, and long/short with major ETFs and large-cap stocks. Signal updates are published during the weekend, with all entries and exits occurring at the following open.

Hybrid asset allocation and dynamic momentum signals (precise entry and exit signals every month) for four models are generated to give you a total portfolio solution.

For more information about the strategies, including performance, click here. Membership’s are on a quarterly or annual basis and is for the signals only, it does not include any strategy rules.

DGM - Next Day Move

DGM is a machine learning algorithm (statistical model) based on alternative data – dark pool data and options dealer gamma exposure (DIX and GEX) – with the goal to predict the direction of the next day move in the S&P 500 index (SPX).

The model uses data made available courtesy of squeezemetrics and is updated daily. It is re-trained with every update using an extensive optimisation and selection process (part design, part randomisation, part brute-force), then executed to attempt a prediction and tested against past data.

Each update contains three sections:

Latest daily data and prediction for the subsequent day

Backtest return and simulated success rate for the recent history

Recent history backtest details (mostly for eyeballing)

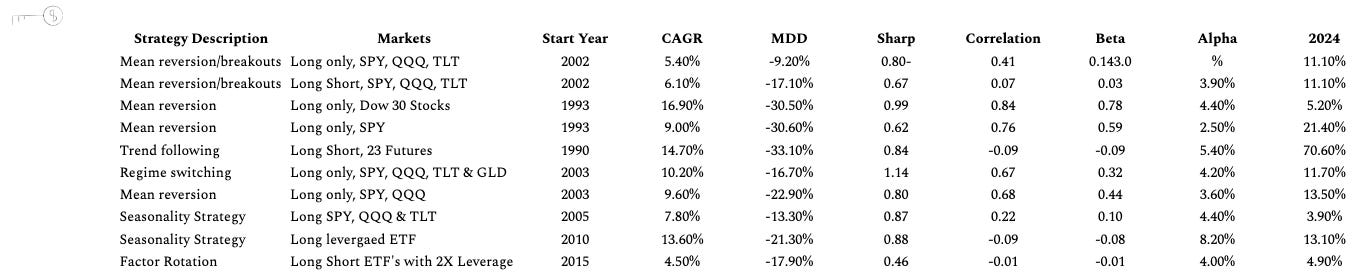

10 Trading Strategies for Sale

Trading success depends on three key factors: sufficient capitalisation, discipline, and edge. We cannot do anything about the first two, but we can try to help with the third. The strategies we have developed are based on the following two principles: simplicity and economic value.

Simplicity reduces the probability of overfitting and data-mining bias. Economic value is necessary in the form of reasonable alpha and risk-adjusted returns.

The strategies are suitable for traders with basic knowledge of programming and testing rules on backtesting platforms. We provide the rules only. We do not provide any code.

The rules of 10 strategies are available for sale in a bundle. The rules we provide are sufficient for programming the strategies on a trading platform. The strategies are not data-mined and have simple rules. Do not expect anything overly complicated.

*The correlation, beta, and alpha are with SPY ETF. The skew is for the equity curve’s daily changes.

Delivery: The trading rules are in the form of “secure content” via private email.

Terms: All sales are final, and no refunds will be made on any purchase. No refunds are given for cancellations or under any circumstances, and there is no exception.

Strategy code: We provide the rules in plain English. The customer will need to convert those rules to code before testing them on a backtesting platform.