Well Timed Triggers

Macro Perspectives: Tue 30 Nov 21

In the second half of 2014, the price of crude oil had fallen from $108 to the low $70s - the market was oversupplied. Prices were plunging, and OPEC was expected to deliver an announcement of a production cut, to put a floor under prices. Instead, they pulled the rug out.

On the evening of Thanksgiving, OPEC surprised the oil market with a well-timed announcement that they would not defend the price of oil with a production cut.

I say "well-timed" as their objective was, contrary to the market's view, to pulverise the price of oil - they chose a thinly traded holiday market to do it. With that, oil fell about 14% over the next 24 hours - and was nearly halved just two months later.

What was the motivation? They wanted to put the emerging, competitive U.S. shale industry out of business, by forcing prices below the point at which the shale companies could profitably produce.

They nearly succeeded - Shale companies started dropping like flies, with more than 100 bankruptcies over the next two years.

This came to mind this past Thursday, when I saw the announcement of the new variant. Well-timed - by the time many market participants were seeing the news, in thin markets, stocks, yields and commodities were all much lower.

The concern, even Thursday night, had less to do with the virus, and more to do with how governments would respond. Lockdowns? More restrictions?

Thus far, the response seems mild (as do reports on the virus). With that, markets get a good bounce to start the week. But as we know, even before omicron, parts of the world were tightening restrictions, and Austria went back into lockdown.

Bottom line: The probability of economic headwinds, associated with the virus, are higher today than where we left off before the U.S. holiday.

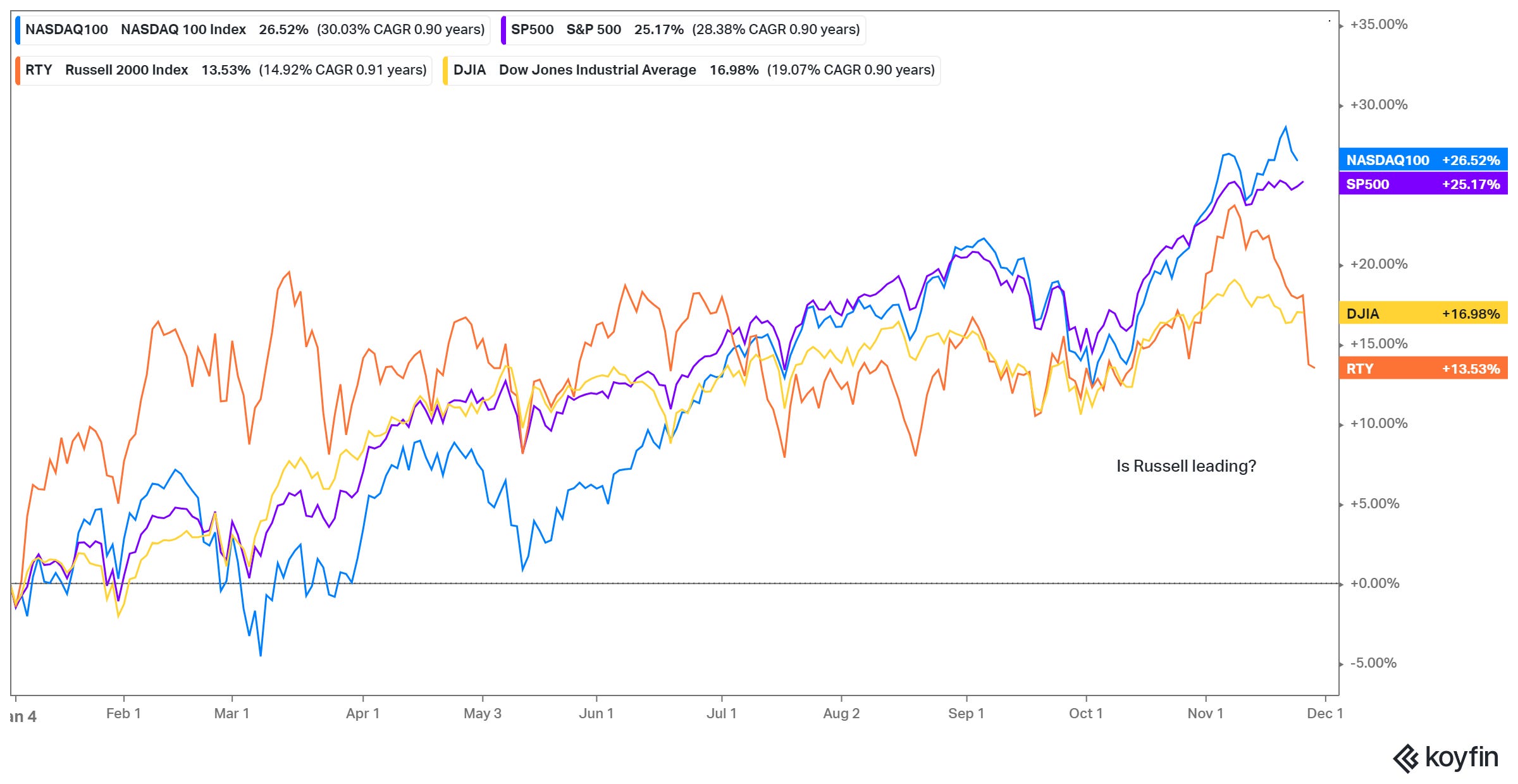

With that in mind, we looked at the key reversal signal in the Nasdaq last week (also in the S&P 500)...

Technically, the charts have already been flashing some warning signals. With the introduction of some new uncertainty for markets and the economy, the Fed will come back into the crosshairs. As we know, they have recently begun dialing down QE. They have given us a target of "full employment" as a trigger to start the lift-off of interest rates - that trigger point is already arguably close, and we get a new data point on jobs this Friday.

So, by the end of the week, with any negative virus news, we could have a deteriorating economic outlook, just as data is hitting (from last month) that shows perhaps a trigger for Fed liftoff (or closer to it).

This scenario would put pressure squarely on the Fed, to walk back on its well-telegraphed exit of emergency level policies. If the history of the past 12-years is our guide, stocks would punish the Fed (i.e. move lower) until they respond - and they would respond.