Value Stocks - Not Happening Yet...

Macro Perspectives: Wed 27 Oct 21

Earnings continue to come in strong. As of Friday, 84% of the S&P 500 companies that have reported thus far have beat earnings estimates, and 75% have beat revenue estimates.

After this week, we will have heard from about half of the S&P 500 companies.

The big question coming into this Q3 earnings season was about "costs." So far, so good - margins seem to be holding up, in the face of rising prices and rising wages. That means companies are having success passing along prices to customers.

Microsoft and Google both reported record earnings after the close yesterday. We'll hear from Amazon and Apple today. Despite the big earnings numbers, these "big tech" stocks should start feeling some pain from the outlook for higher interest rates. Higher rates, for growth stocks, tends to bring about lower multiples and lower discounted cash flow valuations.

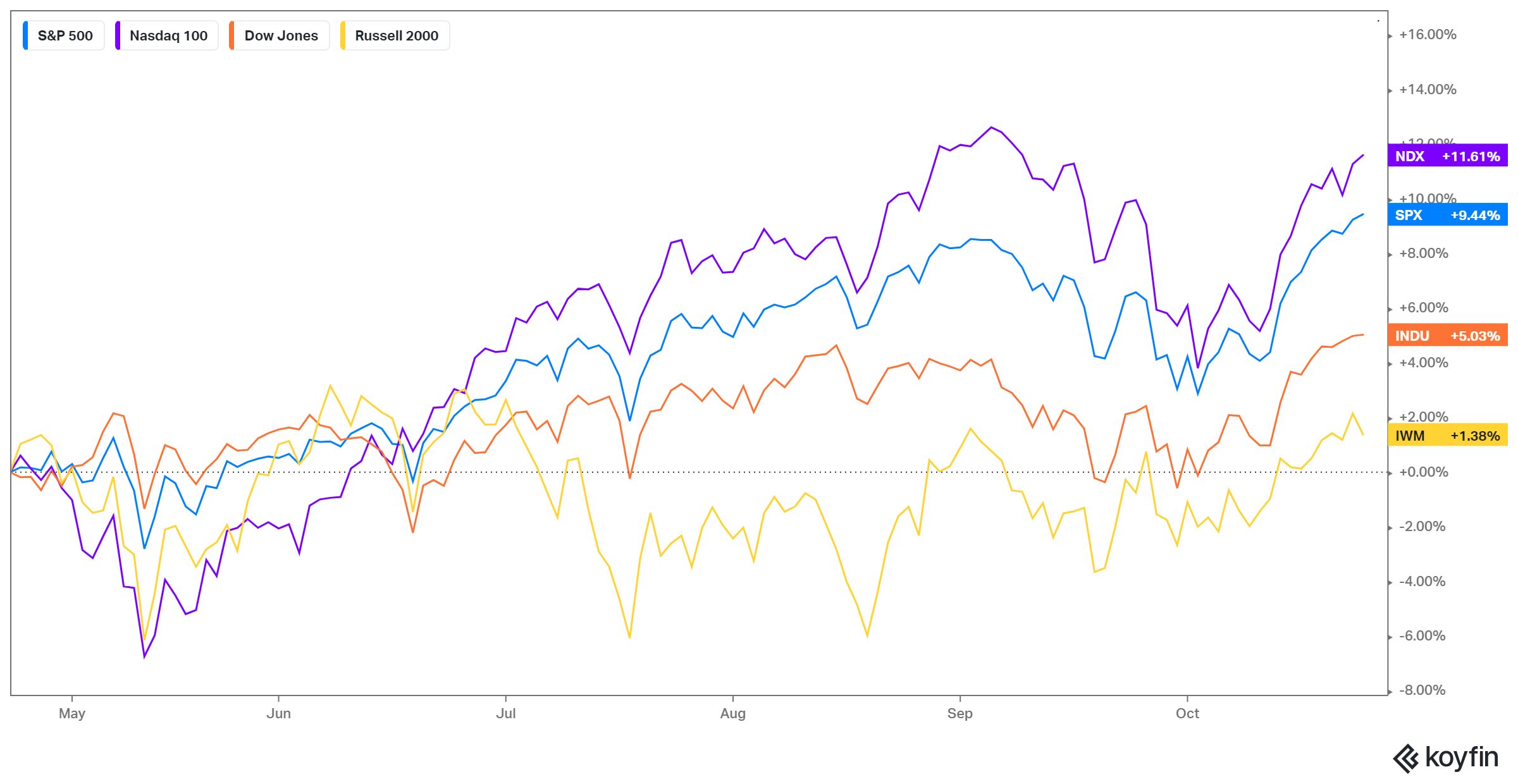

That's why value stocks should be in favor, but it's not happening yet. While the S&P and the Dow have both returned to new record highs. The Russell 2000 (small caps) are lagging behind - still 2.7% from the March highs.

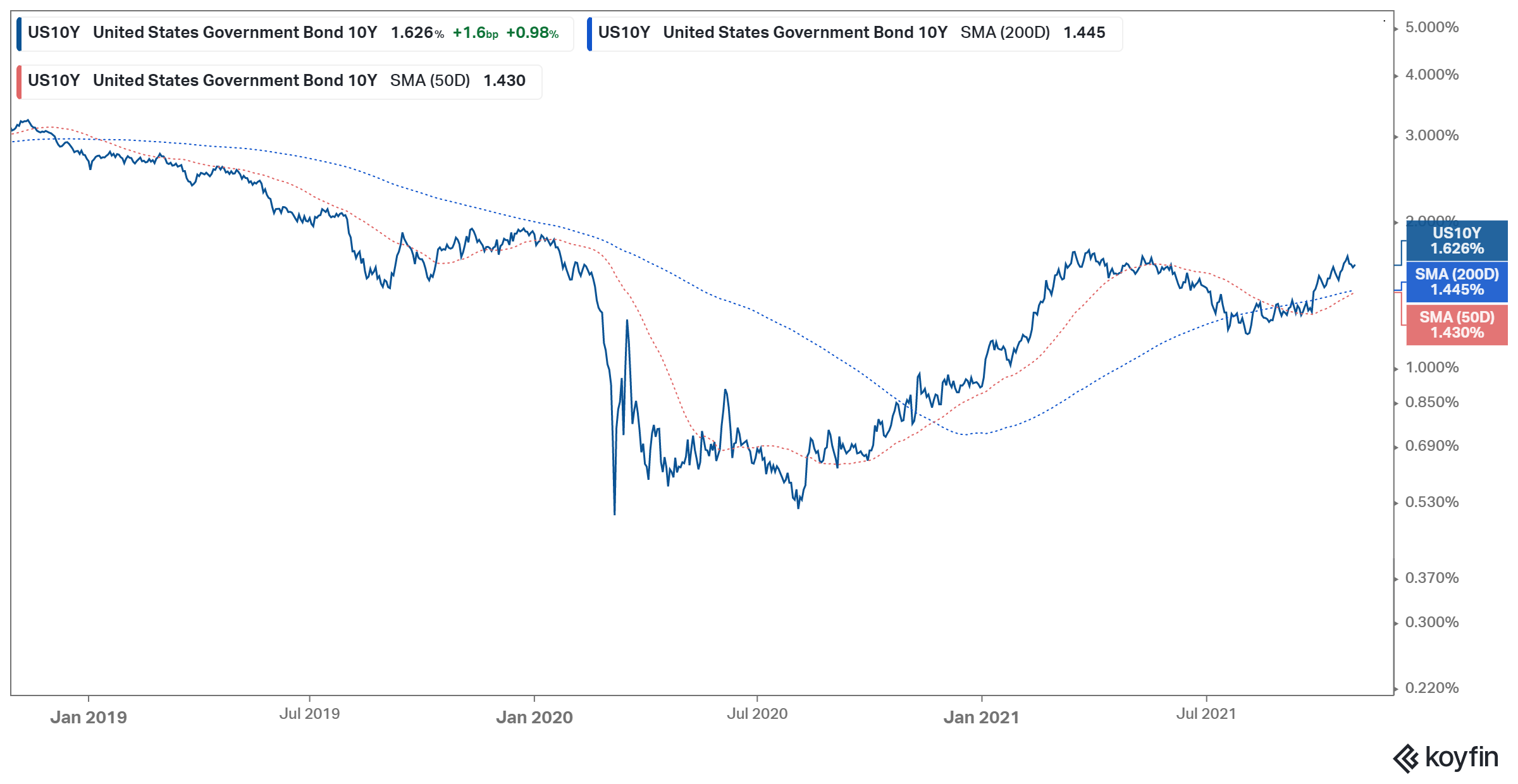

And it’s all because of this chart…

With the 10-year yield at just 1.62%, rates have not been moving up fast - thanks to a Fed that is still in control of the Treasury market.

As we've discussed in past notes, coming out of recession, small caps historically track rates higher, and go on to outperform large cap growth over the following decade (post-recession). With the above in mind, small cap value stocks continue to be the spot of relative opportunity in the stock market.