US10Y pre-empting Oil???

Macro Perspectives: Wed 7 Jul 2021

We open the week (U.S. market calendar) with some swings in markets.

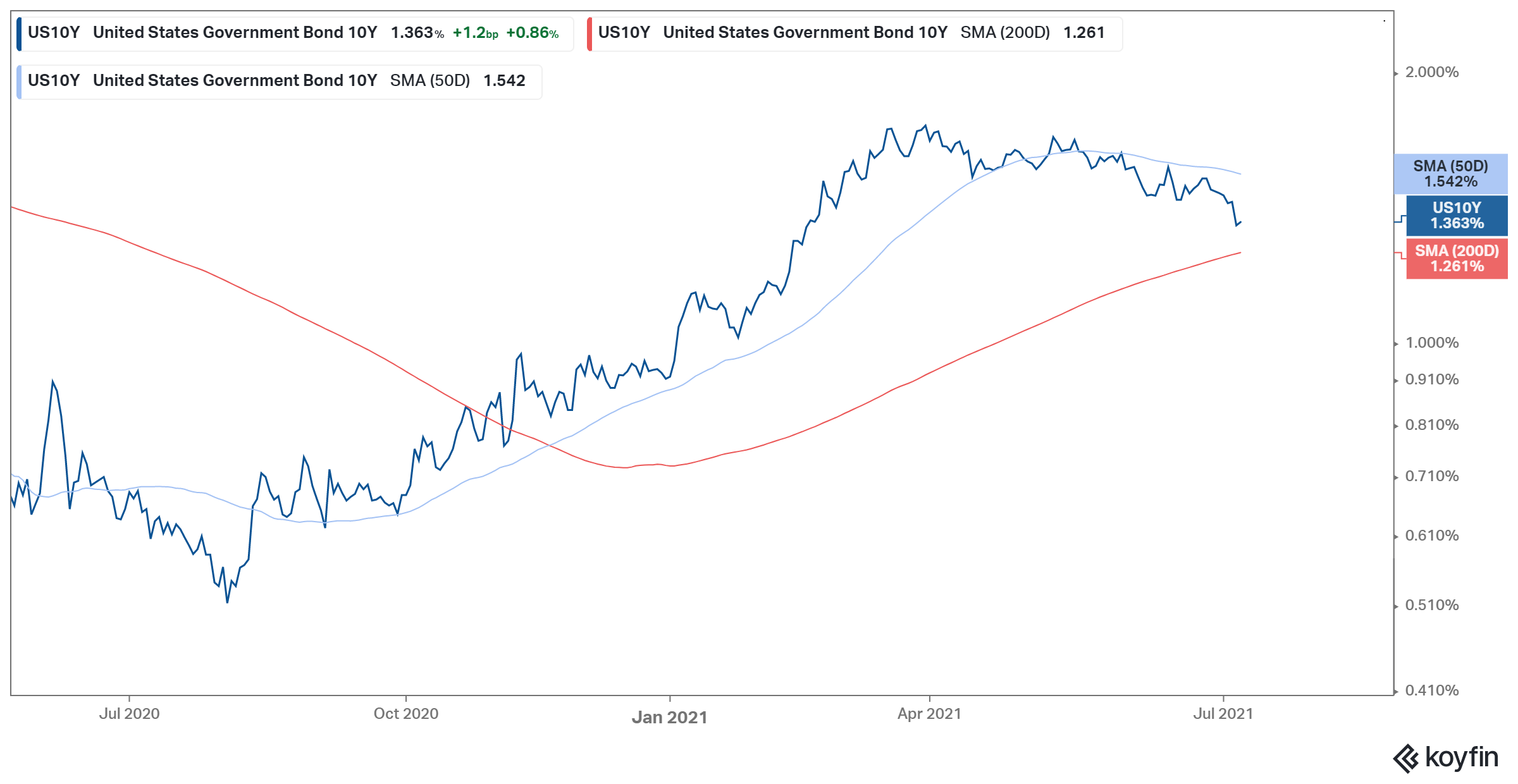

Despite a Fed that has been sending signals of an end to emergency policies sooner than the very conservative timeline they had been projecting, the 10-year yield has been moving lower, not higher. Yesterday, the 10-year traded back down to 1.35%. We sit on a technical trendline, which represents the economic recovery period...

Is the 10-year yield telling us that the bond market knows something?

Remember, the Fed continues to absorb up to $80 billion of Treasuries each month. With that, the market isn't dictating the direction and level of yields (interest rates), the Fed is. The Fed is explicitly manipulating the interest rate market.

Now, with yields sliding, and stocks and commodities selling off earlier in the session, the financial media went through its list of things to worry about: the virus variants, tough talk from China, cyberattacks…

Again, the Fed is in charge of the bond market, and perhaps the Fed is indeed pricing in some risk to the recovery story. If so, it probably has everything to do with the prospects of $100 oil.

Oil producing countries are at an impasse on negotiating oil supply (namely, UAE is in disagreement with the 23 other members). That brings about three scenarios, two of which spell out a path toward $100+ oil…

Opec+ agrees to a deal to add 400k barrels a day between August and December. That's expected. As we discussed last week, similar to its gradual bump to supply in June, it doesn't meet surging demand - prices go higher.

Opec+ doesn't agree. They do nothing - Oil prices scream higher.

UAE exits OPEC and (ultimately starts pumping). That creates cracks in the Opec armor and global economic uncertainty. This could go either way for oil prices in the very short term, but to be sure, all parties are motivated by higher prices/higher oil revenues.