US 10 Yr - Manipulation, Intervention & Crisis Aversion

Macro Perspectives

In my note yesterday, we discussed the significance of the level of the 10-year yield (around 4%). In past notes, we discussed the historical spread between the 10-year yield and the Fed Funds rate - the 10-year yield tends to run about 90 basis points (on average) ABOVE the Fed Funds rate, historically.

As of yesterday morning, the 10-year was trading over 50 basis points BELOW the Fed Funds rate.

This has created the inversion of the yield curve, an historic predictor of recession - and with that, people are expecting recession. But as we discussed yesterday, the U.S. 10-year government bond market has been a highly (and overtly) manipulated market over the past fifteen years - by the Fed, and by global central banks.

It's fair to assume that this manipulation continues, to suppress this key global interest rate benchmark. Let's talk about why.

Throughout the past year, we've talked about the stress that rising global interest rates would put/ have put on the global financial system (global rates which have been pulled higher by the U.S. monetary policy anchor). History gave us reason to expect things to break as the world tried to escape zero interest rates and QE. Remember, we've yet to see an example of a successful exit of QE.

The attempted exits have only led to more control and more intervention by central banks over markets - to plug leaks in the global economic system. This round looks to be more of the same;

First, it was Europe's sovereign debt market, in June of last year. European sovereign debt markets were breaking, as the U.S. 10-year yield was hitting about 3.30%. The European Central Bank had to intervene to avert another sovereign debt crisis.

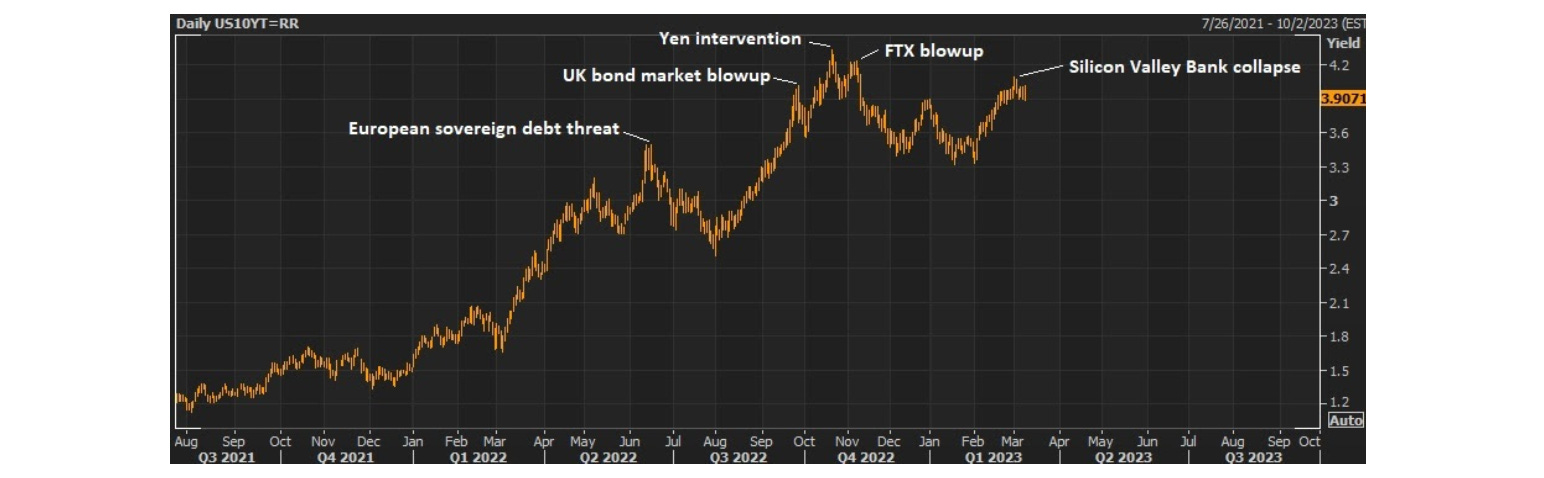

Intervention. Crisis averted.

Then, in September, it was the UK bond market that broke. The Bank of England had to intervene to avert a financial system meltdown. U.S. yields traded up to 4% when that UK bond market crisis was revealed.

Intervention. Crisis averted.

Then U.S. yields surpassed 4% and climbed sharply, to 4.34%, in just three days. The dollar was racing, and the yen was crashing (driven by the aggressively widening interest rate differential). The Bank of Japan was forced to step in, to rescue the rapidly declining value of the yen.

Intervention. Crisis averted.

A month later, the 10-year yield was back above 4% and rumors started swirling that a major cryptocurrency exchange, FTX, was in trouble. Forty-eight hours later, it was insolvent.

That was the last time the 10-year yield traded above 4%. Until last Thursday . . .

Over the weekend, a big Silicon Valley bank (banker to major VCs and startups) started to crumble (more below).

Below is the chart of the 10-year yield - you can see the levels where these events triggered.

So, as we suspected heading into this tightening cycle, another Volcker-like inflation fight was never in the cards. Why? Because even if the U.S. economy could withstand the pain of higher interest rates (which includes our government's ability to service its debt), the rest of the world can't.

The market implications of this situation are far and wide. We have a $210+ billion balance sheet (which was a mere $86 billion 2 years ago) that could well have an unwind. It is not a stretch to argue that on a current mark to market basis that equity is negative to the tune of of billions - you can be insolvent but liquid and survive as a bank.

Of note;

$15.1 billion of unrealized losses on the HTM. Average yield on this book is a mere ~190 bps. How can they can't sell this - I suspect its frozen.

Preferred stock trade down 15% yesterday - it’s is at $16.60 and my par (napkin maths) is $25 for reference.