Undershoot on Inflation

US Stocks kicked off the week on a sour note, as the S&P 500 and Nasdaq lost 1% and 1.2%, respectively, while Dow Jones plunged 398 points.

The benchmark 10-year Treasury yields climbed above 4% for the first time since August.

This week, key inflation data will be closely watched as the earnings season begins, featuring reports from major banks like JPMorgan, Wells Fargo, and Bank of New York Mellon.

Sector-wise, utilities, communication services and consumer discretionary dragged the most, while the energy sector finished in the green.

Among tech giants, Apple (-2.2%), Microsoft (-1.6%), Alphabet (-2.4%), Amazon (-3%) and Meta (-1.9%) were down, while Nvidia (+2.5%) advanced.

We came into Friday's jobs report with the Fed projecting two additional quarter point cuts into the end of the year, with "unexpected weakness" in the labour market as an explicit condition that would prompt them to move faster.

The jobs report came in unexpectedly strong.

This follows the recent upward revisions that were made to Q2 economic output, personal incomes, consumer spending, and the personal savings rate. In the words of Jerome Powell, that removed what the Fed perceived to be "a downside risk to the economy."

So, with this good jobs report, we have more new information that suggests the economy (maybe) isn't as fragile as many have feared, including the Fed. Does that mean the Fed's September cut was a mistake? Is inflation coming back?

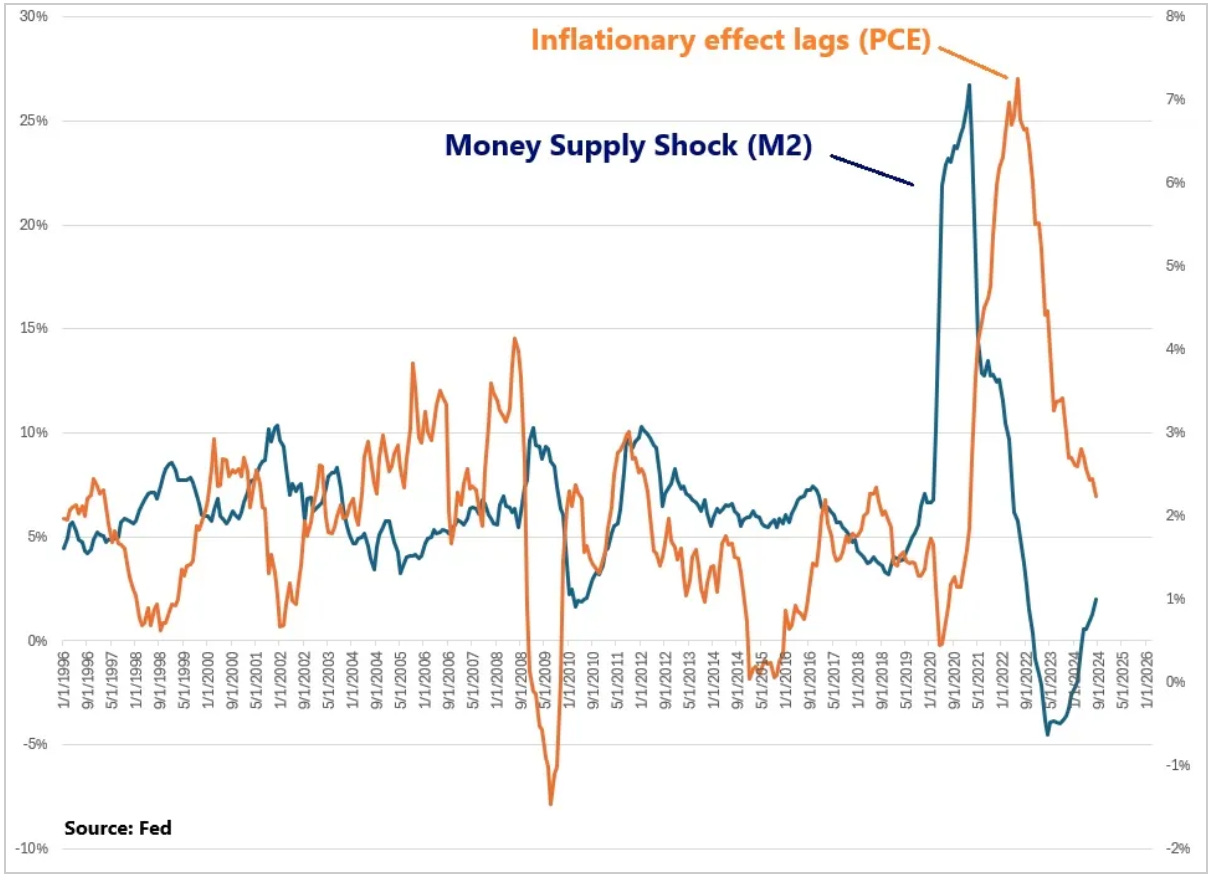

Let's revisit my chart from my 08 May 2024 piece, where we looked at the relationship between the change in money supply, and inflation.

As you can see, we had a growth shock in money supply (the blue line), from the 2020-2021 policy response to the pandemic - that was the inflation catalyst. And you can see the lagging effect on inflation (orange line), as it peaked 16 months after the peak of money supply growth.

We've since had the disinflationary effect (falling inflation) from the decline in money supply growth. Not only has money supply growth dramatically declined, it contracted for sixteen consecutive months - contracting money supply is historically deflationary.

From this, we should expect the pressure on prices to continue to be downward.

With that in mind, let's take a look at a few comments made by the Chicago Fed President (and voting member) Austan Goolsbee.

He said, he's "extremely happy with the jobs report." But he wanted to make clear that the "large majority of Fed policymakers feel rates are going to come down a lot over the next year to 18 months."

And he said, "there are some signs that inflation might undershoot target."

GRYNING | Signals - Performance of the ensemble and benchmarks

Weekly return of the ensemble: -0.3%

Year to Date Performance

Tactical asset allocation, mean reversion, cross-sectional momentum, and equity long-short with weekly and monthly updating. For more information and to access the reports, click on the link below.