Two Clues

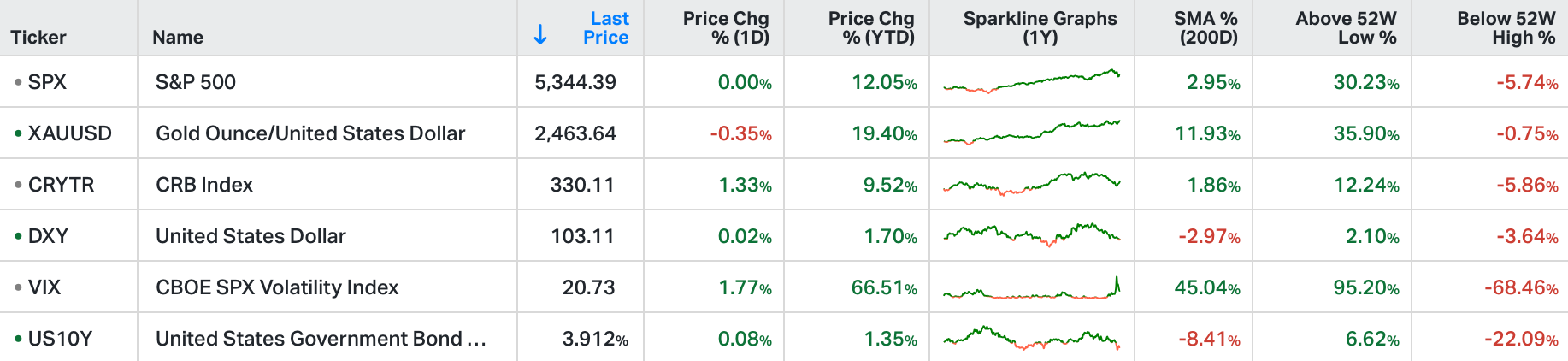

US stocks swung between gains and losses on Monday, as market volatility remained high and traders brace for a week packed with key data that will help to assess the strength of the US economy and inflationary pressures.

The CPI report will be in the spotlight, alongside PPI, retail sales and industrial production.

The tech sector managed to stay in the green while communication services was the worst performer.

Megacaps were mixed, with Microsoft (-0.4%), Amazon (-0.2%) and Meta (-0.5%) declining while Apple (0.5%), Nvidia (2.3%) and Alphabet (0.8%) were higher.

Tesla was also down over 2.5% and Home Depot lost about 1.4%.

In my June 29th 2023 note, here, we talked about this picture …

This was a central banking forum in Portugal hosted by the European Central Bank. On this stage were the four most powerful central bankers in the world (from Japan, the U.S., Eurozone and UK). They fielded questions spanning from the inflation outlook and rate path, to geopolitical concerns (Russia and China), fiscal policy, digital currencies, and AI.

As we discussed in that note, the guy on the left is the Governor of the Bank of Japan (BOJ), Kazuo Ueda, and he was the most important person in the room that day.

He was the only one in the room trying to get inflation UP to 2%, and therefore was the only one in the room with negative interest rates, and printing yen each month and buying both domestic and global assets with that freshly printed yen (with no limits).

This BOJ policy not only suppressed Japanese government bond yields, and promoted inflation and economic growth in Japan, it also suppressed the U.S. benchmark government bond yield (the 10-year yield), and served as a liquidity offset (to a degree) to the Fed's (and Western world) tightening.

The Western world's inflation fight (via the tool of "normalisation" interest rates) only worked with assistance of the Bank of Japan.

And it was clearly well coordinated. Japan continued ultra-easy policy, printing yen, and manipulating/suppressing global market interest rates so that the tightening policies of its G7 counterparts didn't blow up their own respective government bond markets (and trigger a cascade of global sovereign debt defaults).

With this context, there's probably a good reason that Ueda said, while on that stage with his global central banking counterparts, that rates would go up by a large margin in Japan, "IF they GET to normalise policy."

Let me repeat that: He said, IF they GET to normalise policy.

He made that comment more than a year ago.

Fast forward a year, and Ueda just tried (on July 31) to initiate the second step toward normalising policy in Japan — announcing a plan to taper the asset purchase program that has pumped liquidity into the world.

And instead of providing some offset to Japan's actions, the Fed, almost simultaneously, chose to hold rates at historically tight levels (the highs of the tightening cycle).

It didn't go well. This policy combination created a crisis-like shock across key global markets.

And within days the Bank of Japan was verbally walking back on their policy path. From the behaviour of markets over the past few trading days, it looks like they may be directly intervening (buying assets) to stabilise the Nikkei and the yen, and as a by-product the most liquid, widely-held U.S. stocks.

So, what are the clues that Japan went back into emergency policy mode, filling the cracks that emerged in the global financial system (and in communication/coordination with its global central bank counterparts)?

The first clue is that the Fed speakers we've heard from over the past week have been mostly apathetic to the recent market shock.

They haven't tried to assuage markets by signalling any greater appetite to cut rates — no acknowledgement of a policy mistake. And keep in mind, the U.S. 2-year yield had the type of extreme decline only associated with major market crisis events (each of which were followed by a Fed response).

The second clue: Gold.

If this extreme market reaction is further evidence that the global economy can only be held together with central bank life support, then quantitative easing is a permanent feature.

Printing money means the purchasing power of the money in your pocket goes down. Gold goes up, relative to the value of fiat currencies. Indeed, gold closed testing record highs, yet again.

With that, we've often looked at this longer term chart of gold over the years, since it was trading in the $1,600s in March of 2020 and $1,800s in November 2020 (here). Spot gold is now closing in on $2,500.

And this classic C-wave (from Elliott Wave theory) projects a move up to $2,700ish.

I'll be away the remainder of the week, so you will not receive a Macro Perspectives note from me - however, Gryning is expanding!