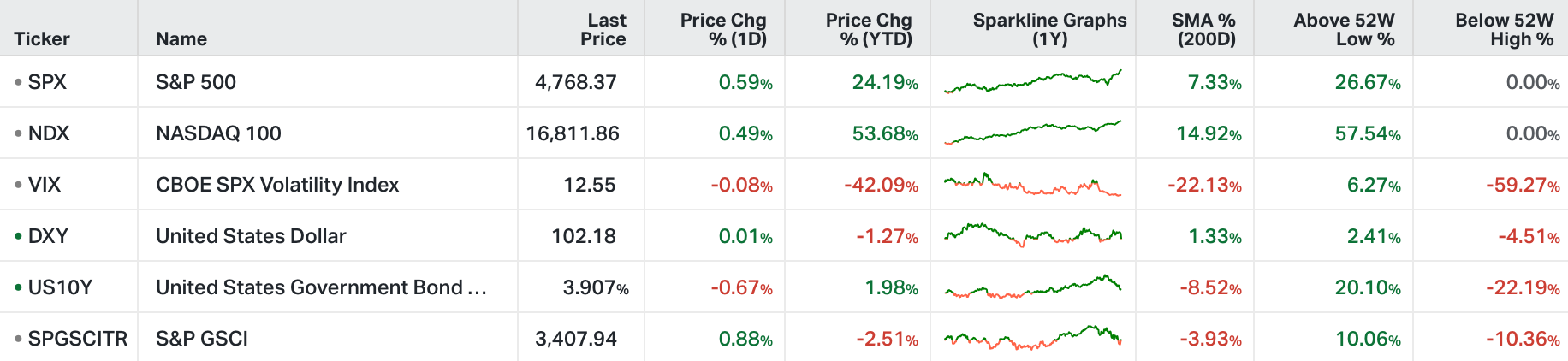

US stocks advanced on Tuesday, amid mixed statements from Fed officials.

Investor sentiment leaned towards the belief that the Fed is orchestrating a soft landing, with expectations of three rate cuts in 2024.

The Nasdaq 100 rose 0.6%, nearing its all-time high, the S&P 500 set a new record with a 0.6% gain, and the Dow Jones surged 251 points to close at fresh record levels.

Housing starts unexpectedly rose, suggesting a housing market recovery.

Affirm soared 15.5% after announcing an expansion of its “buy now, pay later” partnership with Walmart to over 4,500 of the retailer’s self-checkout kiosks.

Macro Perspective

Earlier this month, we looked at the Fed's new financial conditions index, which gauges the impact of financial conditions on future economic growth. The index is designed to incorporate the lags of monetary policy, and project (in this case) one-year forward what the impact will be on real GDP growth. They just made an update to it on December 15th . . .

As you can see to the far right of the chart, it's still projecting nearly 1% drag on growth one-year forward. Remember, this index factors in the current Fed Funds rate, the 10-year yield, the 30-year fixed mortgage rate, the lowest investment grade corporate bond rate, the DJIA stock market index, the Zillow house price index, and the value of the dollar.

With all of this in mind, this recent update to the index is from data up to November 10th and as we discussed in my note earlier this month, from the chart above, we can see that these current levels in the index tend to be turning points for financial conditions (i.e. more favorable financial conditions for growth ahead).

Indeed, the turning point is already underway. Take a look at what has happened in the components, just since the last index update:

The 10-year yield has dropped from 4.63% to 3.91%.

Mortgage rates have dropped more than half a percentage point.

Corporate bond rates have dropped almost a full percentage point.

The Dow is up 8%.

The dollar is down 3%.

With the above in mind, last week we looked at what this move in the 10-year yield should mean for mortgage rates. The average spread of the past 20-years between the 10-year yield and mortgage rates is 1.8%. So we should expect the mortgage rate component of this index to have an even more dramatic move lower (settling in the high 5% area, assuming the 10-year yield at current levels).

As for the dollar, a turning point in financial conditions means a weaker dollar, and that comes as the dollar is testing this big multi-year bull trend. This increases the probability of a break of this trendline (i.e. a break lower) . . .

For the stock market component of the index: Remember, if we look at stock market performance one-year forward from these turning points, stocks do very well in the subsequent 12-month period . . . and small caps outperform.