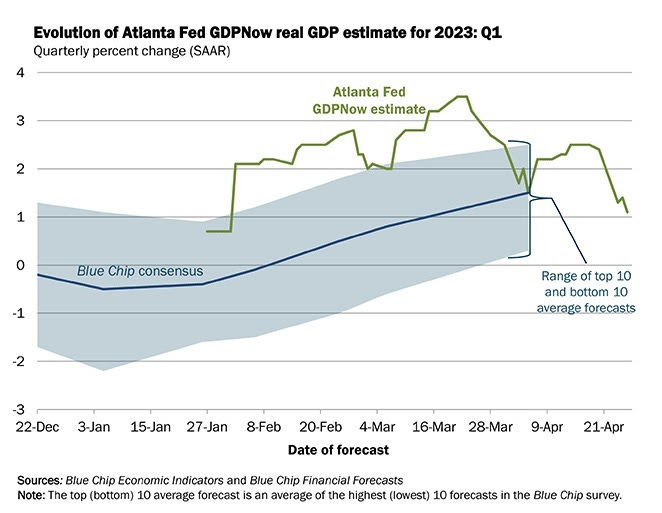

The first estimate on Q1 GDP came in yesterday morning. It was weak. In fact it was spot on with the recent adjustment in the Atlanta Fed's model (1.1% growth).

As you can see in the graphic above, this model was tracking north of 3% growth for the quarter, before the bank shock of last month.

With this in mind, the Fed has wanted to see a slowdown in economic growth, and a loosening of the labor market, as a means to ensure inflation is on a sustainable path lower.

Well, they now have economic slowdown. Growth has gone from 3.2% in Q3 of last year, to 2.6% in Q4, to 1.1% in Q1. That 1.1% is well below long-term trend growth (3+%).

They've gotten some job losses, particularly in the over-staffed tech sector. The number of job openings (which Jay Powell has specifically referenced) has dropped by 1.3 million jobs since December (probably related to tech).

The important inflation number comes in today - it's the March core PCE. This measures the change in prices of goods and services that people have actually paid, not just a selling price. "Core," means excluding food and energy prices. This March number will incorporate the fear, albeit brief, surrounding the safety of bank deposits.

The last reading was at 4.6%, year-over-year change. This is the number the Fed wants to see back toward 2%. But importantly, it's lower than the current Fed Funds rate, which should be applying downward pressure on inflation.