Tone Deaf

Stocks in the US closed lower on Wednesday, as the market failed to extend its Tuesday recovery following Monday's selloff.

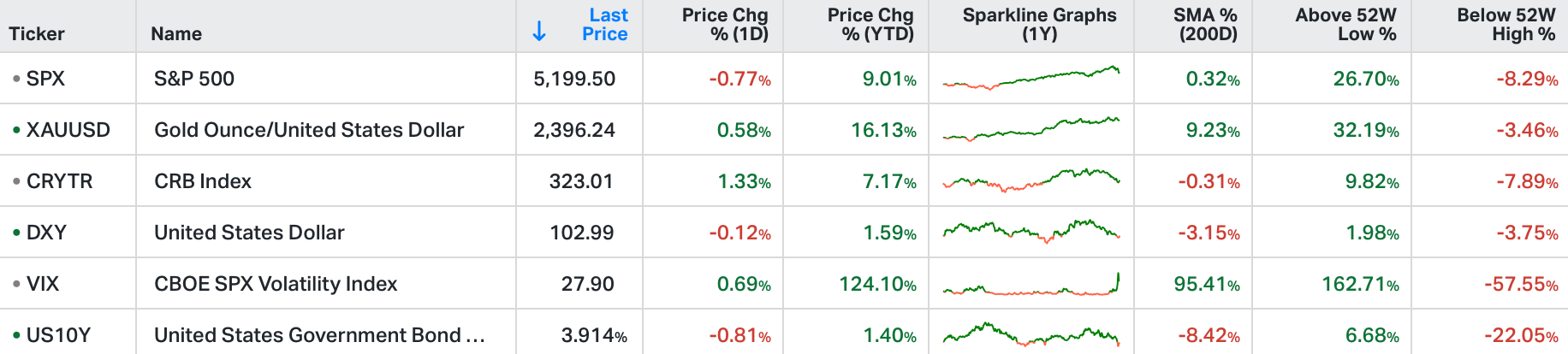

The S&P 500 lost 0.7%, the Nasdaq slid 1% while the Dow Jones fell 234 points.

Meanwhile, the Bank of Japan offered investors some confidence after Deputy Governor Shinichi Uchida said the central bank will refrain from hiking interest rates when the markets are unstable.

Consumer discretionary sector dragged the most, led by a 4.4% fall in shares of Tesla, followed by materials and technology.

On the earnings front, Disney shares declined 4.4% due to concerns over its park business despite reporting its first-ever profit in its streaming unit.

We looked at this chart on Tuesday, which shows the severity of the move in Japanese stocks relative to history ...

In each of these extreme periods of decline, there was a central bank response that shortly followed (i.e. QE).

Just hours later it was reported that the Bank of Japan, Japan's Ministry of Finance and the Financial Services Agency would hold an emergency meeting to discuss international financial markets.

Stocks went up.

The next night, the Deputy Governor of the Bank of Japan was on the wires walking back on hawkish policy path.

Stocks went up.

This was verbal and maybe actual intervention by the Bank of Japan to stem the sharp unwind of the carry trade that was shaking global markets.

But will it stabilise markets? The Bank of Japan has a long history of currency market intervention - it tends to have some short success in slowing progress, but limited long-term success.

What has a history of working? Coordinated central bank intervention.

In this case, this market instability is about the Bank of Japan laying out the plan last week for its final step in exiting its role as the world's global liquidity provider (i.e. tapering its QE program), while the Fed stubbornly held rates at historically tight levels—unnecessarily too tight, for too long.

With that comes;

the risk of a global liquidity pendulum swinging hard in the direction of too tight (i.e. a liquidity shock), and

the risk of the Fed turning deficit-funded economic growth into recession in the largest economy in the world.

The market judges the combination of central bank decisions to be a policy mistake. The Bank of Japan seems to acknowledge it. That's good. The Fed seems tone deaf to it. That's not good.

With that, if history is our guide, financial stress will probably grow until something breaks, and the Fed is forced to react.