Three Arrows

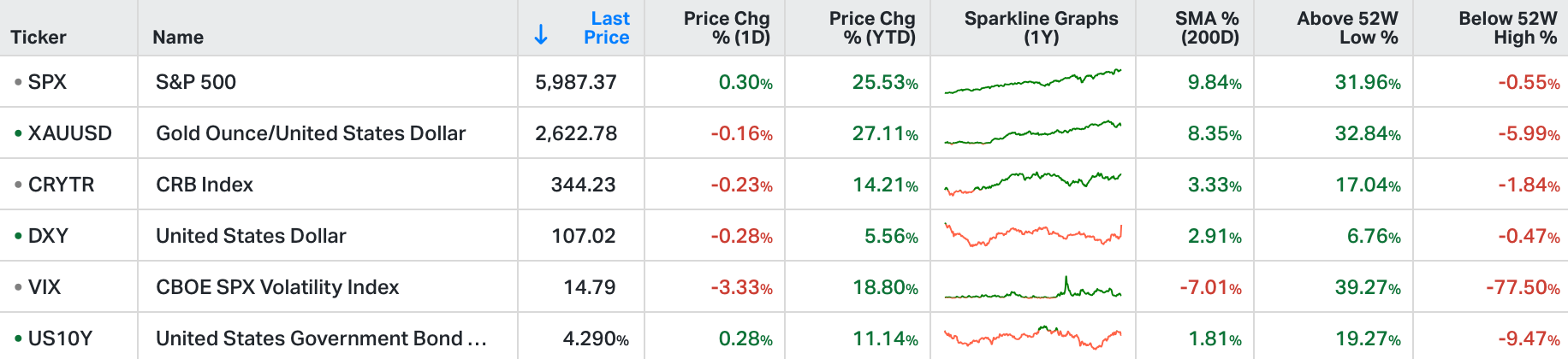

The S&P 500 and Nasdaq kicked off the week higher, adding 0.3% each, while the Dow Jones closed at a new record, climbing 440 points.

Optimism was driven by President-elect Donald Trump's nomination of hedge fund manager Scott Bessent as Treasury Secretary, as investors anticipate market-friendly policies and a tempering of extreme protectionist measures.

Big tech saw mixed performance, with Amazon (+2.2%) and Alphabet (+1.7%) rising, while Nvidia (-4.2%) and Netflix (-3.6%) declined.

In corporate news, Macy’s (-2.3%) shares dropped after delaying its Q3 earnings release due to an investigation uncovering over $100 million in hidden expenses.

Bath & Body Works (+16.5%) surged on a strong earnings forecast, while MicroStrategy (-4.4%) made a record $5.4 billion Bitcoin purchase.

After the market closed on Friday, Trump named Scott Bessent his nominee for Treasury Secretary.

This is good news.

He comes in as a Trump loyalist, with a clear stated interest in executing on the Trump agenda - he's talked about his own equivalent of Abenomics to turn the economy around.

His "three arrows" would aim for;

3% real GDP growth through deregulation, lower energy prices and giving businesses confidence to hire and invest,

bringing the deficit down to 3% of GDP by the end of the term, through cuts to discretionary government spending and better growth,

increasing energy production by 3 million barrels (boe) a day, which will bring down overall prices.

So, it's the 3/3/3 plan. Much of the execution of this plan will depend on how successful he and the Trump team are in dealing with China. As with Trump, Bessent might be "the perfect man for these times. Not all times, perhaps not most times, but these times."

He's well aware of/on high alert to the vulnerable position Yellen has left the bond market in, by financing record peacetime deficit spending with short-term maturities—a third of the outstanding government debt will need to be rolled over through the next year.

He's also a China hawk. He understands very well that the multi-decade global imbalances that have delivered the frequent booms and busts in the global economy have to be resolved—and it's brought to us by China's currency manipulation.

On the latter, let's revisit an excerpt from one of my notes during Trump's first term (from August 2019) …

"As we know, China has used a weak currency to leapfrog almost the entire world over the past 30+ years, capturing 15% of the global economic market share and rising to an economic power.

They've gone from a $350 billion economy in the early 90s, to a $13 trillion economy today (ascending from the eleventh largest country in the world to the second largest economy in the world). That's 37 times bigger. Over the same period, the U.S. economy has grown by 3x.

How has China done it?

By undercutting the global export market on price, collecting our dollars, then offering our dollars back to us in the form of credit, so that we can buy more from China.

As long as China can maintain a cheap currency (and its trading partners allow it), this cycle continues, and so does the cycle of global credit booms and busts.

Meanwhile China stockpiles/sucks foreign currency (most importantly, dollars) from the rest of the world (i.e. a wealth transfer).

Clearly, this story ends well for China, and no one else, if left unchecked. That's why it has become the top priority for Trump (and a critical piece of Trumponomics).

Reforming the way the U.S. (and the world) deals with China is the root of the global structural reform that is necessary for the world to sustainably emerge from the global financial crisis era."

Not only does this all still apply, it's arguably beyond the tipping point now. Even Bessent has openly said, this might be "the last chance to grow our way out of the [debt] problem" (the debt problem which is derived from this structural imbalance).

On that note, currencies are the natural balancing mechanism to prevent the bubbles and global imbalances from forming.

If the yuan were freely traded, with aggressive growth in the economy over the past three decades would come a rise in the value of the yuan (rise in demand of yuan-denominated assets), making its exports more expensive. The Chinese would consume more with a more valuable currency and richer asset values, and produce less.

Weaker economies would have less demand for their assets, a weaker currency, and therefore more attractive exports. They export more, consume less. And so the cycle would go.

It all spirals down, however, when a major trading partner is deliberately manipulating its currency (keeping it cheap)…But only if its trading partners keep trading with it.

Unfortunately, Western world politicians have kept trading with China. They've done very little over the years to disrupt the spiral for a variety of reasons (it's politically unpalatable … constituents like cheap stuff, governments like cheap credit, and politicians like political and financial favours).

So, as with Trump 1.0, Trump 2.0 will be about dealing with China.

Bessent has already telegraphed what he thinks will be another Plaza Accord type of "large scale globally coordinated currency, fiscal and monetary" agreement. For it to work, it seems like it will have to involve putting China in the trade penalty box.

As you might suspect, China's multi-decade economic war (driven by currency manipulation), which has evolved into hybrid warfare over the past eight years (economic, psychological, biological, information, political, cyber) will likely escalate.

APMLIFY YOUR INVESTMENT PROCESS WITH GRYNING

Become a member to any of the above to have the annaul membership period doubled for free.

Great insights sir, thanks a lot again for sharing!

I'm trying to understand exactly how China's currency manipulation may have delivered these "booms & busts in the global economy": do you mean it is directly related to it "collecting our dollars, then offering our dollars back to us in the form of credit, so that we can buy more from China"?

I've got the 1st part of the the mechanism with China accumulating USD by exporting / selling cheap goods (in USD terms). But then isn't the USD credit / debt cycle primarily dictated by the US government fiscal policy itself? Sorry, might have missed something else there :)