This was expect...This is good

Macro Perspectives: Wed 26 Jan 22

As we head into today’s Fed announcement we have the proxy for high-growth tech stocks (the Nasdaq) near the bottom of an 18% correction. We have the key market interest rate (the 10-year yield) trading at 1.78% (up to pre-pandemic levels).

For some perspective on how the financial market and economic environment has evolved in just two short months, I want to take a look back at my November 23 note, with the Nasdaq having topped the previous day...

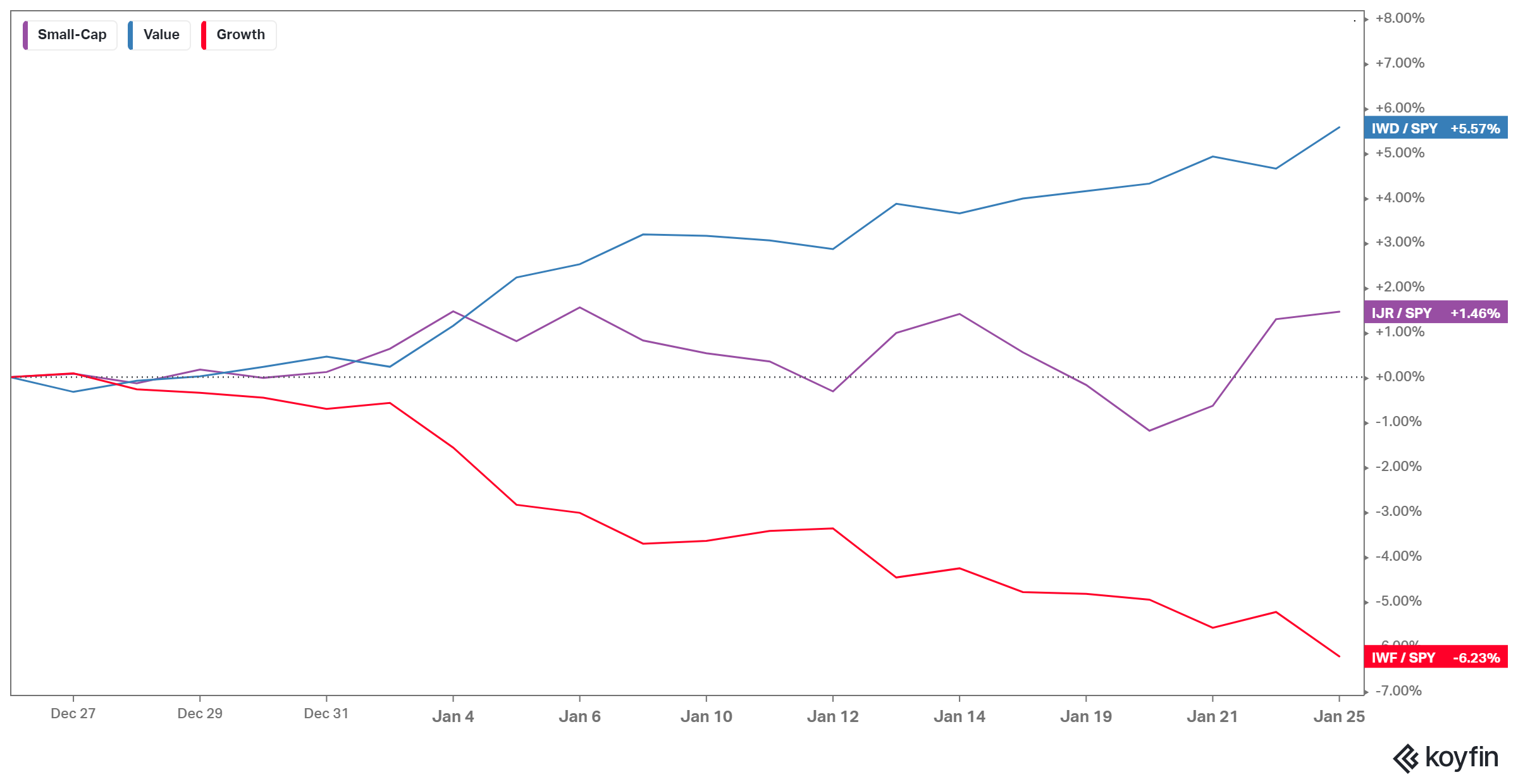

Within the above note, I posted an Alpha Idea - below is the relative previous month performance…

Now, as we know, this trigger from November 23nd, the re-nomination of Jay Powell, cemented the outlook for the exit of the Fed's emergency policies (and the onset of a new tightening cycle). Thus, we have indeed seen the unwinding of growth stocks, and a sharp rise in the 10-year yield.

This has brought about more of the Pavlovian expectations that the Fed (based on market conditions) might back-peddle today on the policy path. But as we discussed yesterday, the environment the Fed is faced with now is very different from much of the past decade (post-financial crisis). The Fed is dealing with a 5%+ growth economy and 7% inflation - it's the inflation problem (in this case), not tighter money, that is the biggest threat to economic activity.

Remember, we also looked at this chart below a couple of months ago (surrounding this top in the Nasdaq) - it shows how inflation has affected the consumer outlook.

As you can see in the far right of the chart, prices up (the purple line)...sentiment down (the orange line). Ultimately consumer sentiment dictates consumer behaviour.

The Fed clearly knows they are dangerously close to the point of losing control of consumer behaviour. So, despite some of the emotions we're hearing surrounding the recent decline in stocks, a faster path to normalising rates (and stabilising prices and sentiment) should be good for markets and economic stability.