The race to Double Digit Inflation

Macro Perspectives: Thu 31 Mar 22

As March ends, all eyes will turn to inflation data - it's going to be a wrecking ball for central bankers that are trying to manage inflation expectations.

The Fed is far more concerned about inflation expectations, than they are about inflation. If they lose control of expectations, people start pulling forward purchases, in anticipation of higher prices, creating a self-fulfilling upward spiral in prices.

With this, you have to wonder what the first double-digit print in inflation will do to consumer psychology. I suspect we will find out on April 12, when we get CPI numbers for March.

Keep in mind, for February, the data came in hot, with prices close to 8% from the same period a year prior, and that did NOT yet account for the sharp spike in the price of oil. Add in a 30% spike in oil prices, and a double-digit March inflation number seems like a done deal.

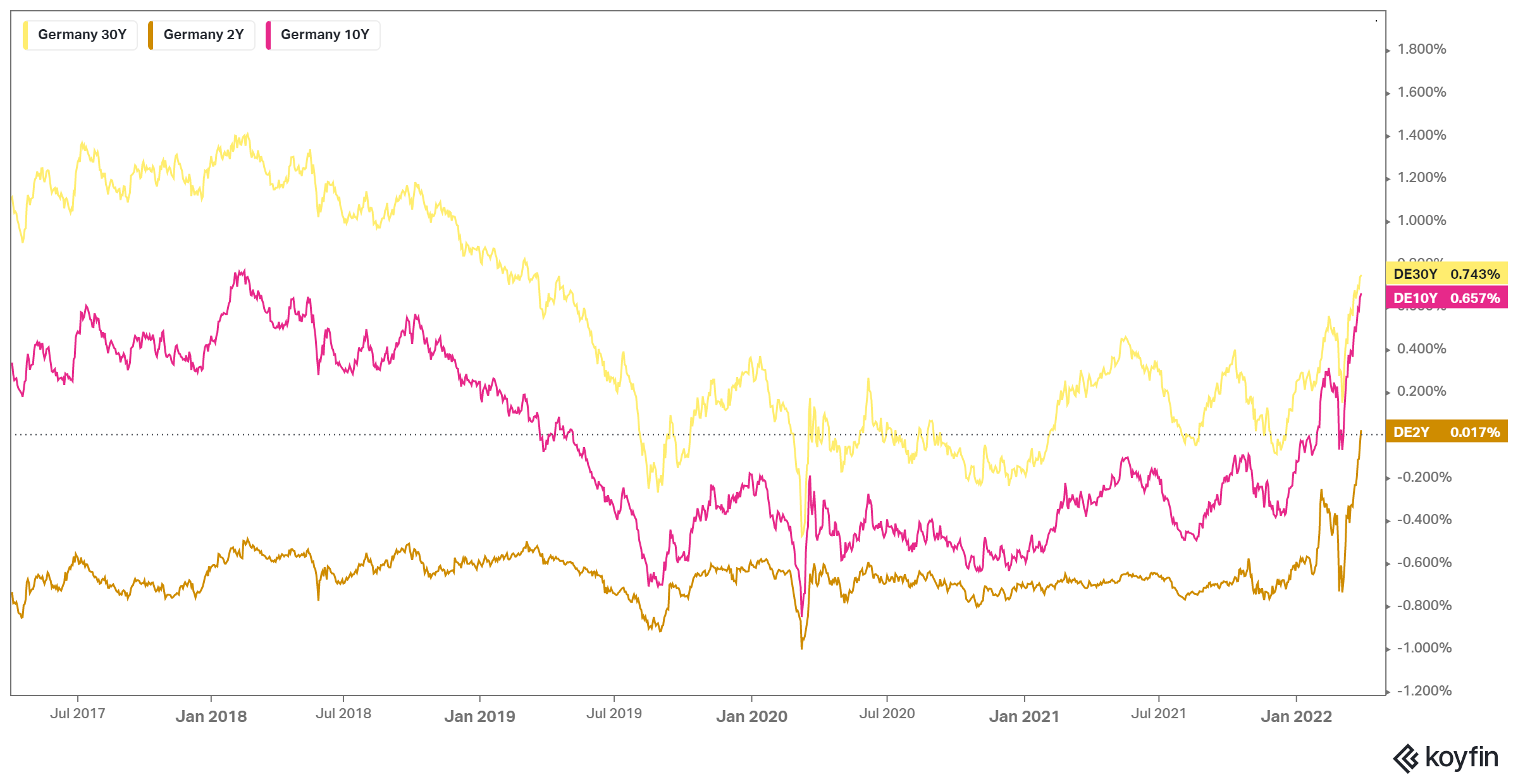

We had some clues from the German inflation data yesterday, a preliminary reading for the month of March, it was a huge negative surprise - the 7.3% year-over-year increase in prices was more than two percentage points higher than the consensus estimate.

The consensus view for March U.S. inflation (thus far) is 8.2%.

Where would a negative sentiment shift in the inflation outlook most quickly tend to manifest?

The bond market - Yields (market interest rates) would go on a tear. Not only could that signal exacerbate inflation fears, but it could also trigger global capital flight, which could lead to a currency and debt crisis. This brings us back to my note from yesterday, where we discussed the prospects of global central bankers following the Bank of Japan's lead, by setting market interest rates (i.e. yield curve control).

So, just as the Fed has exited QE, they may be forced to return to the QE game very quickly (buying treasuries to maintain an orderly rise in market interest rates).