The Fed's thinking on Wage Growth

Macro Perspectives

Let’s continue from our Thursday discussion, the Fed's primary objective is to reduce leverage of the job seeker, and current workforce, in commanding higher wages.

Wage growth has fueled inflation and what the Fed fears is a wage (upward) spiral.

That said, after adding $6 trillion to the money supply in two years (ten years worth of money supply growth in two), we should expect higher prices - it's excess money, chasing a relatively stable quantity of assets. That's a formula for higher prices.

And as we've discussed, while the rate of change in prices (i.e. inflation) will come down, the level of prices will not - unless much of that $6 trillion is sucked out of the economy . . . that's not going to happen. It is implied that the Fed's quantitative tightening program will accomplish that, but if we look back at the 2017-2019 period, when the Fed was shrinking it's balance sheet, the money supply (M2) kept growing!

Back to Friday’s jobs report . . .

Again, the most important data point in the report wasn't jobs, but it was wage growth. Is there more evidence that the wage spiral threat is abating?

The answer is, yes.

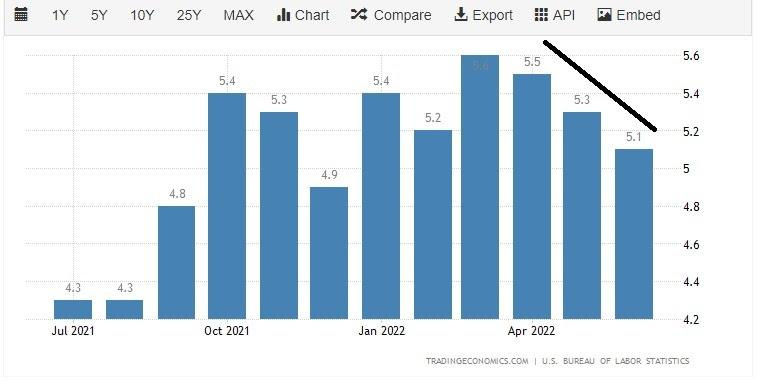

Average hourly earnings (chart above) grew by 0.3% - annualised we get 3.7% wage growth. That's significantly lower than the year-over-year change, which is better than 5% growth (but trending lower), as you can see in the chart below...

Wage growth in the 3s would get us back to pre-pandemic levels, taking some of the steam out of inflation, and pressure off of the Fed to raise rates.

To be clear, with inflation running 8%+ and wage growth running quite a bit less, we have negative real wage growth. Life is just more expensive - which begins to slow economic activity.

Given all of the available options to deal with inflation, that seems to be the Fed's favored option: Let inflation solve inflation.

On that note, the market is pricing in another 75 basis point hike from the Fed later this month. If the CPI number on Wednesday comes in lower, my bet is for another 50 basis points (to return the Fed Funds rate to 2%), and the Fed will be done.

They already gave us a clear signal last week - by executing only 15% of their June plan to shrink the balance sheet - that they are not serious about doing any meaningful tightening . . . we shall see.