The Fed still Buying Bonds

Macro Perspectives: Tue 01 Feb 22

Stocks have recovered sharply from the lows of last week. The S&P 500 and the Dow have now closed back above their respective 200-day moving averages.

Corrections are part of investing, and despite all of the things to worry about, this looks like a garden variety correction.

After all, the economy remains on a path to do above trend growth this year, with a very hot jobs market (where employees are commanding higher wages). Consumer and company balance sheets remain strong. The tailwinds of $6 trillion of new money supply created in the past two years continue to blow.

With this, despite the hand wringing over the Fed, even assuming a more aggressive tightening path than has been projected by the Fed, they will continue to run highly stimulative monetary policy for quite some time (given the position they are starting from - zero rates).

This is all a formula for the continued march higher in asset prices.

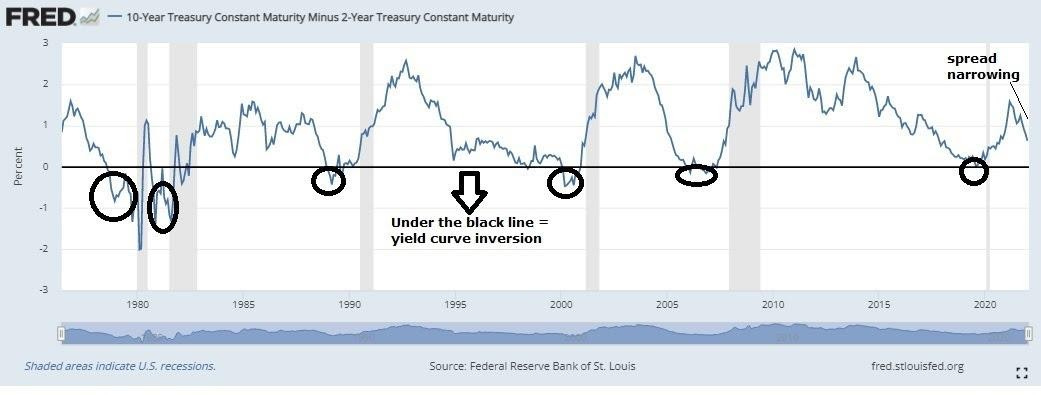

The bond market is behaving strangely. Spreads between shorter dated Treasuries and longer dated Treasuries have been narrowing - that can be a sign of concern about economic slowdown, possibly recession.

The chart below shows the yield on the 10-year minus the 2-year. When that goes negative (inverts), it has predicted the last seven recessions (the shaded bars).

As you can see on the chart, to the far right, the 10s-2s spread has been narrowing. Again, this has people asking if something bigger is coming - there's chatter about "slowing growth." But slowing from the best growth in almost four decades, to something still above long-term trend growth (based on forecasts), is still strong growth.

So why is the bond market behaving in a strange way? It's simple - the Fed is still buying bonds until March (they remain in control).