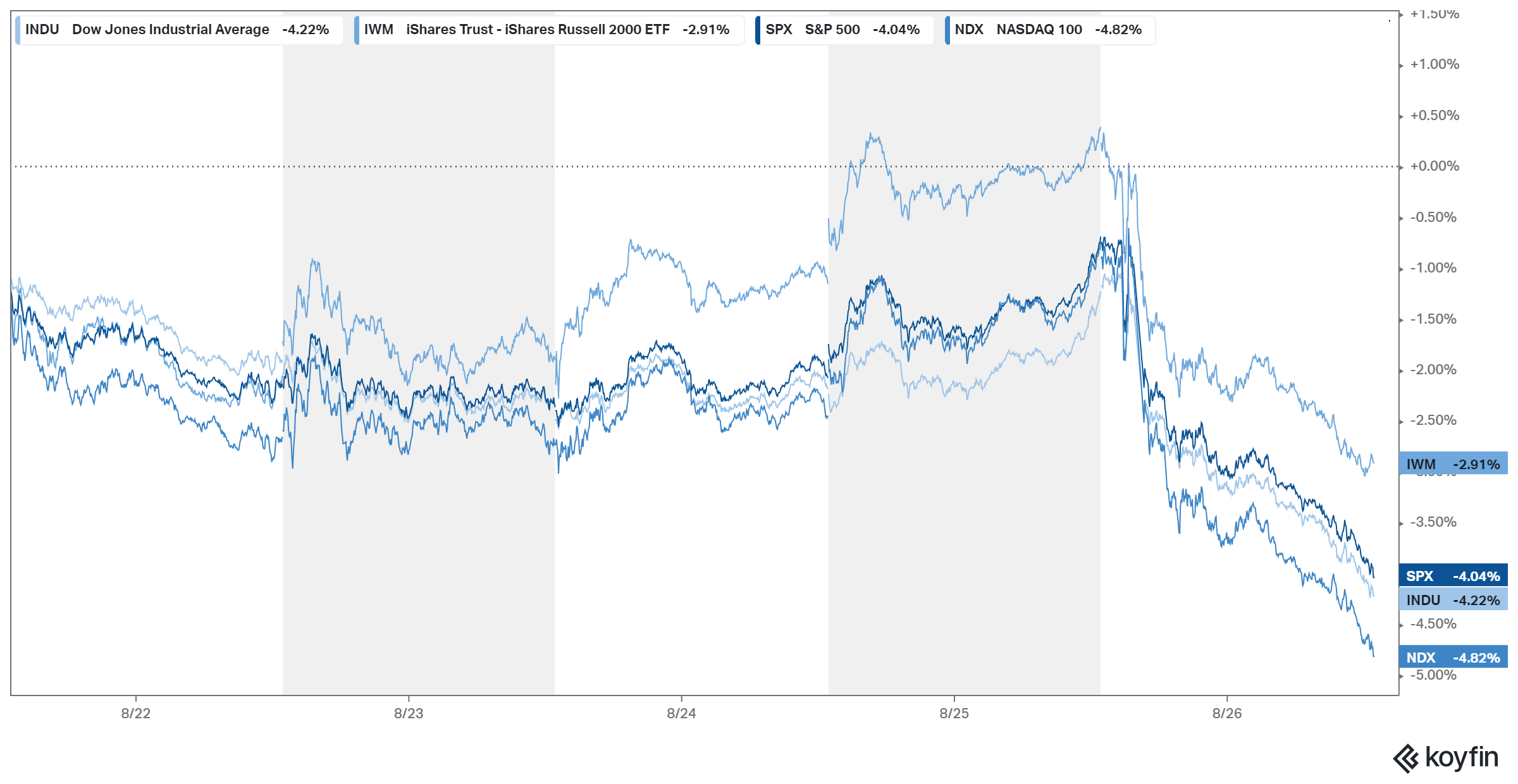

We heard from Jerome Powell at Jackson Hole; he was hawkish (not what I had expected), stocks went down.

Remember this, when listening to all of the jawboning about the Fed and interest rates, and the markets: The Fed can raise rates at any time they want, and in any amount. If they wanted to slay inflation, they could raise rates right now to 6%, 7%, 8% - whatever they want.

They haven't . . . Instead, they continue to do a lot of talking.

Did we learn anything new?

First, if we look back at the July Fed meeting, they raised rates to 2.25-2.50% (range), and Powell said they had reached the neutral level. He went on to say that they need to get to "moderately restrictive," and then he pointed to the committee's published projections of 3.25-3.5% (at year end). That's another 100 basis points.

Fast forward one month, and he said they are moving purposefully to a level that will be sufficiently restrictive, and said the current level (of neutral) is "not a place to stop or pause."

Nothing new there.

He went on to reference the 70s and 80s inflation period, and cited two former Fed Chairs, specifically their commentary on inflation expectations. Why?

As we've discussed here in my daily notes many times, the Fed is far more concerned about inflation expectations, than they are about inflation. If they lose control of expectations, people start pulling forward purchases, in anticipation of higher prices, creating a self-fulfilling upward spiral in prices.

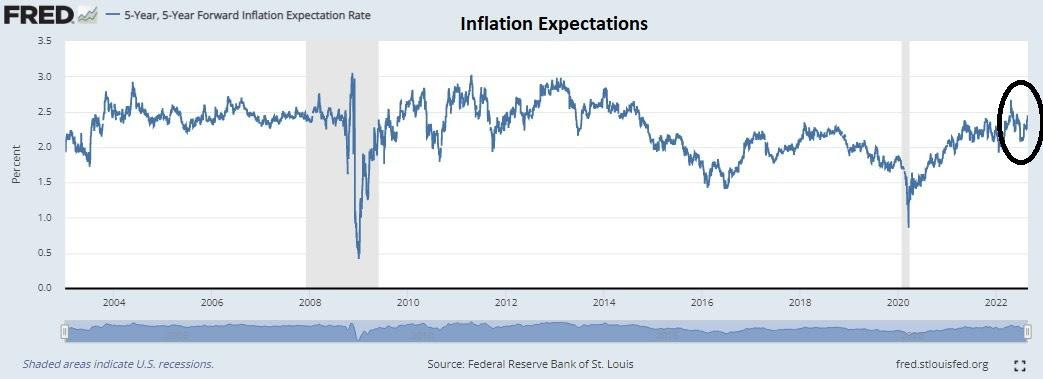

On that note, the Fed shouldn't be overly concerned. Here's a look at their favored gauge of inflation expectations ...

This is running under 2.5%, and as you can see it's well within the upper part of the range of the past 20 years. This is, in large part, thanks to the tough talk from the Fed this year.

Far more powerful than the 225 basis points of interest rate hikes, has been the Fed's threat to "bring down demand" and push unemployment up. The former has led to falling stock prices whilst the latter has led to less job security, and less leverage in negotiating wages. And both have led to two consecutive quarters of negative GDP.

The result: The Fed is doing it's job. It has crushed the animal spirits in the economy, just through threats. And with that, the rate-of-change in prices is on the decline.

The media would have you believe the Fed is in crisis, in the early stages of fighting inflation from behind (and the Fed benefits from that perception). The data tells a different story - they are doing well, especially given their constraints.

What are those constraints?

Massive domestic debt and debt service. Every 100 basis points they raise rates, the U.S. government adds $285 billion annually to the deficit.

The higher U.S. interest rates rise, emerging markets and fiscally fragile developed market countries become increasingly vulnerable, in this post-global financial crisis environment, to a debt default - which historically we know creates the vulnerability to a global debt-default contagion.

So the Fed doesn't appear to have the ability to use the brakes on the economy, but rather to govern the speed as best they can, using the tools they can (which is, manipulating perception).