Tariff Escalation

US stocks fell sharply on Wednesday, as tech stocks led a broad selloff amid mounting concerns over impending US tariffs.

The S&P 500 declined 1.1% and the Nasdaq 100 dropped 2%, ending a three-day rally, while the Dow Jones lost 134 points.

Auto stocks also weakened after reports that President Trump would introduce new tariffs on vehicle imports at 4 p.m.

ET, with General Motors slipping 3%.

Uncertainty surrounding the scope and impact of these tariffs has fuelled market volatility, raising fears of retaliation and broader economic fallout.

Let's revisit the coming tariff escalation ...

Rebalancing global trade has been a well telegraphed cornerstone of the Trump economic and national security agenda.

April 2nd will widen the reach (with reciprocal tariffs for all trading partners) but the big bang already happened earlier this month, with tariffs implemented on the three biggest exporters to the U.S. (China, Canada and Mexico).

In just his second week in office, Trump kicked things off by putting a blanket 10% tariff on China (in addition to any existing tariffs). As we've discussed here in my daily notes, this "trade war" is really all about China. And it's reflected in this chart (and post) ...

In short, China is the global producer (blue bar), we are the global consumer (light blue bar), and that dynamic has over the past three decades led to the rapid gain in China's share of global GDP (light grey bar).

Why does that matter? It matters because this imbalance has persisted (and continues on that path) only because China cheats on its currency (keeping it cheap).

Currencies are the natural balancing mechanism to prevent the bubbles and global imbalances from forming.

If China's yuan were freely traded, the aggressive growth in the economy over the past three decades would have come with a rise in the value of the yuan (rise in demand of yuan-denominated assets), making its exports more expensive.

The Chinese would have consumed more with a more valuable currency and richer asset values and produced less.

The global pursuit of cheaper goods would have shifted demand to weaker economies in the world, with weaker currencies and cheaper assets, which would result in foreign investment, economic development and export-driven growth.

And so the rebalancing cycle would go. It all goes bad when a major trading partner is deliberately manipulating its currency (keeping it cheap). But only if its trading partners keep trading with it.

Western world politicians have done very little over the years to disrupt the spiral for a variety of reasons (it's politically unpalatable ... constituents like cheap stuff, governments like cheap credit, and politicians like political and financial favours).

With that, we've had a multi-decade wealth transfer.

China sells us cheap stuff. We send them the world's most valuable currency, U.S. dollars. They offer those dollars back to us in the form of cheap credit (buying our Treasuries), which has fuelled more consumption of cheap Chinese products.

This is how China has grown its economy from $300 billion in the early nineties to $18 trillion, and the U.S. debt load has gone from $4 trillion to $36 trillion.

It's a multi-decade economic war (driven by its currency manipulation). They have extracted from the world the largest pile of foreign currency reserves, which they have wielded to exert influence and expand their economic warfare into hybrid warfare (economic, psychological, biological, information, political and cyber).

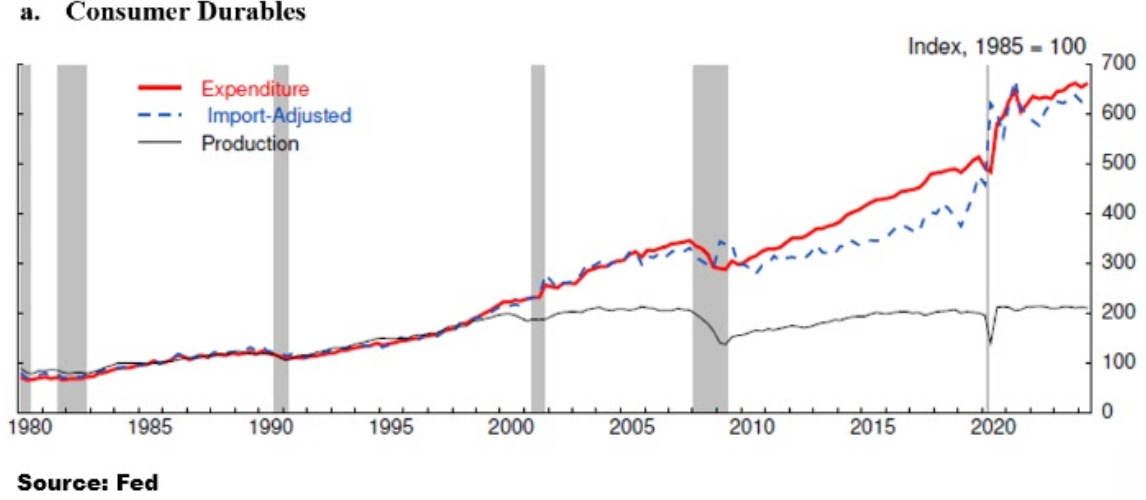

So, dealing with China is priority number one. Here's another good visual (U.S. Consumer Durables) that highlights the imbalance timeline.