Taking It in Stride

US stocks struggled for direction on Friday, with the S&P 500 finishing mostly flat, while the Nasdaq gained 0.4% and the Dow slipped 165 points.

Retail sales fell 0.9% in January, the largest drop in a year, missing expectations and raising concerns over consumer spending.

Investors welcomed a delay in reciprocal tariffs, helping stocks post solid weekly gains.

Tech stocks led gains, while Consumer Staples and Health lagged.

Among individual movers, Airbnb surged 14.4% on strong earnings, GameStop rallied 2.6% on bitcoin speculation.

Friday 08 February, the stock market sold down as the University of Michigan’s latest consumer survey showed the one-year expected inflation rate up at 4.3% from 3.3% in January. By the end of the next trading day, the market recovered a majority of its losses.

Last week, the total Consumer Price Index (CPI) was reported at up 3% year-over-year versus 2.9% in December. The S&P 500 opened a percent lower and then recovered the majority of its loss intraday. The 10-year treasury rate climbed from a low of 4.4% to a high of 4.64% in the past week.

With heavy news flow and concerns about persistent inflation and fewer Fed rate cuts, the S&P 500 has traded essentially sideways for the past three months.

The CBOE Volatility Index (VIX) is unchanged from November 6 (day after the presidential election) to today at about 15. The VIX measures implied volatility—what traders are pricing into the options market. The long-term average level of the VIX is around 18.5% meaning the current implied volatility level of the market is below average.

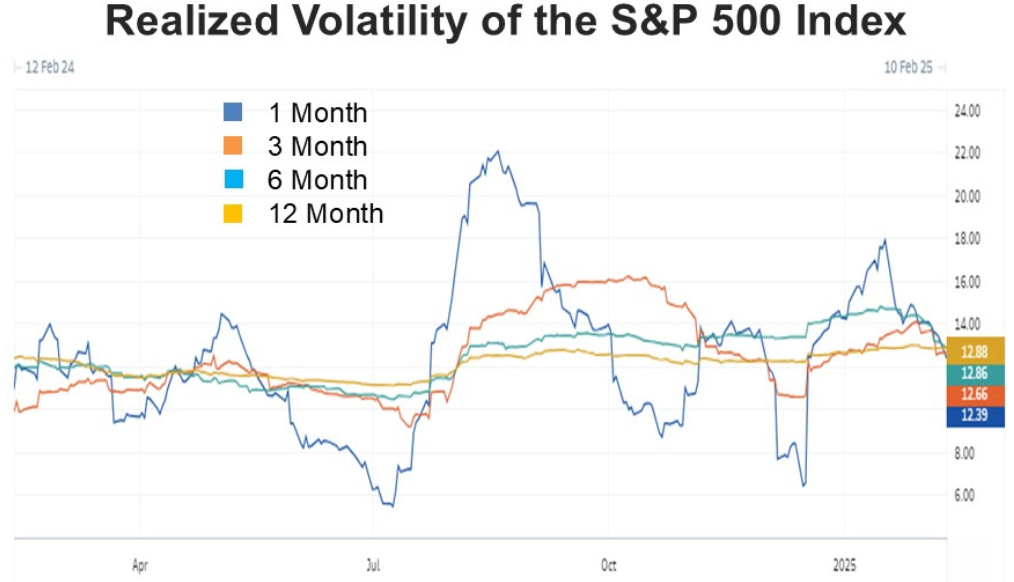

The realised volatility (standard deviation) of the S&P 500 over the past year, six months, 3 months, and 1 month ranges from 12.39 to 12.88. The long-term average standard deviation is roughly 15.

Some of the reasons why the stock market is taking the recent news flow in stride is because the investment backdrop remains fundamentally bullish:

During earnings season, META announced it is budgeting $60-65bn for capital expenditures (capex), MSFT $80bn, GOOG $75bn, and AMZN $100bn. The Magnificent 7 companies raised their capex plans for 2025 to $331bn, up from $263bn. The Mag 7 will spend 31% more on capex in 2025 than they did in 2024.

With over 60% of the S&P 500 having reported, the blended earnings growth rate is 16.4% versus an expected 11.8%.

According to FactSet, analysts estimate S&P 500 EPS will grow 13.0% to $272 in 2025 and 13.8% to $309 in 2026.

The labour market is healthy, with a 4% unemployment rate and initial jobless claims that indicate employers are looking to add workers and reluctant to cut staff.

Low volatility in the stock market is a reflection of a low probability of recession and double-digit earnings growth. Historically, this market backdrop leads to further market appreciation.

Single Stocks: Stay informed on need-to-know macro and utilise our unique single stock strategies to help with idea generation and risk management.

Asset Allocation: Leverage innovative quantitative techniques to drive asset allocation decisions and stay ahead of key structural themes.

Global Macro: Get less correlated inputs for idea generation, as well as a systematic and repeatable approach to macro.

The information content is for a limited readership. We have five (5) membership spots remaining.