Student Debt Cancellation - Struck Down - and Inflation.

Macro Perspectives

Conveniently, just days after the election, a court struck down the Biden administration's plan to cancel student debt (as unlawful).

This (student debt cancellation) was an issue young voters were said to back at double the rate of older voters (twice as likely to vote in favor of) - voter turnout for the young demographic was the second highest on record for a midterm.

Fair to say, it was an executive order that never had a chance, but served as bait to voters. Again, interesting timing on the court decision.

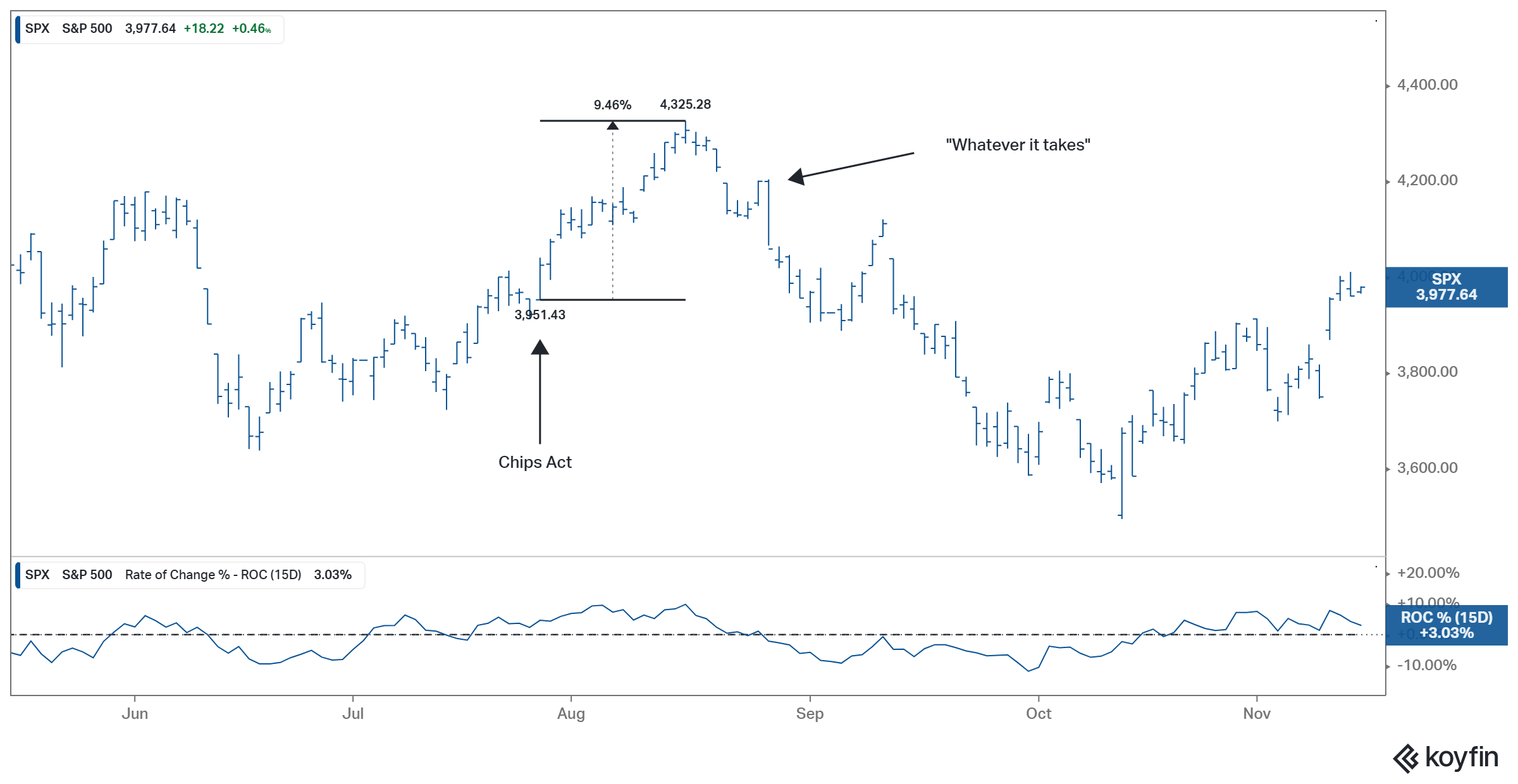

If we think about the inflation picture, this (student debt "relief") was a considerable influence on the inflation outlook. On July 27th, after 225 basis points of rate hikes (a Fed Funds rate of 2.25-2.5%), Jerome Powell told us they had reached the "neutral level" for rates (no longer accommodative, but also not restrictive).

It was an unsolicited message to markets, that appeared to imply they were ready to sit and watch (perhaps they had done enough).

Stocks soared 9% over the next fifteen trading days.

What also happened that day in July? Congress passed the $280 billion Chips Act - the Fed was well aware that was coming.

And by the end of the day, July 27th, the key holdout in Congress from getting the clean energy agenda done, flipped. Manchin was ready to make a deal. And unexpectedly, Congress was ready to add another $500 billion in deficit spending (that's the amount of spending and tax breaks estimated by the consulting firm McKinsey).

Now, how inflationary will these programs be? We don't know. Objectively, both are long-term government spending programs.

If we look back at the 2009 "American Recovery and Reinvestment Act," that was the biggest fiscal stimulus spend on record, but did little-to-nothing to reverse the deflationary pressures in the economy (i.e. it wasn't inflationary). The heavy lifting to fight-off deflation (at the time) was done by the Fed over many years.

It was about a month after the very important events of July 27th that the Fed went back on the offensive against inflation. Jerome Powell revived the rhetoric about doing 'whatever it takes' to slay inflation, at his keynote speech at the big global economic symposium in Jackson Hole.

That was on August 26th. What happened two days prior? Biden announced his plan to cancel student debt.

With this in mind, what has been the most direct driver of inflation within the trillions of dollars in fiscal stimulus over the past two-plus years? Putting money directly into the hands of consumers. What does cancelling a long-term debt burden do for consumers? It redirects debt service into consumption. It's wildly inflationary - and to the tune of half a trillion dollars worth of debt cancellation.

The point: While the student debt promise may have influenced the outcome of an election (not good) ... looking beyond that, the blocking of it may have a major influence on the inflation outlook, and therefore may give the Fed good reason to believe the peak in the inflation data is in (i.e. less restrictive monetary policy, which would be good news).

PS: Having been asked about “longer” form market commentary, I’m looking for feedback to gauge the level of interest. Please click on the link below and vote at the bottom of the page. Thanks!