Stall

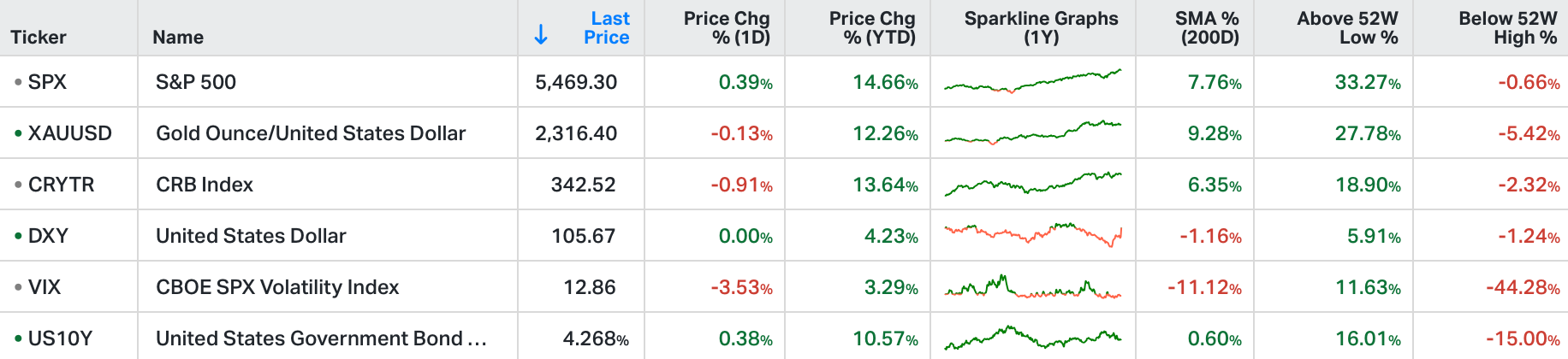

On Tuesday, the S&P 500 and the Nasdaq gained 0.4% and 1.2%, respectively, snapping a three-day losing streak, while the Dow Jones dropped by 296 points.

The tech sector outperformed following a significant sell-off the previous day, during which investors shifted away from semiconductor and artificial intelligence stocks to other sectors.

The communication services sector also advanced, while the real estate and materials sectors lagged.

Microsoft rose by 0.7% after the European Union charged the company with antitrust violations related to Teams.

Both Apple and Amazon increased by 0.4%, Meta climbed by 2.3%, and Alphabet rose by 2.7%.

A retracement in Nvidia shares to the post-stock split opening of around $120 was a welcome dip for those looking to own the most important company in the world/leading the technology revolution.

When Nvidia announced this split last month, we made the comparison to the 7-for-1 split of Apple stock back in 2014. That stock too made a big runup between the day of the stock split announcement and the day of the split. In the case of Apple, after the split, it took almost a month to make a new high.

Within this Apple analogue, we also talked about the post-split prospects of Nvidia's inclusion into the Dow (DJIA), which would be made possible by the lower share price (for a price-weighted index).

It happened in Apple nine months after the 2014 stock split. That said, the Nasdaq outperformed the Dow over that period 2.3 to 1.

Now, on Friday we get the May PCE - personal consumption expenditures - report. This is the inflation measure the Fed cares most about. It's the basis of their 2% inflation target.

We've had clues in the recent CPI and PPI data. Both came in with zero change in monthly prices. And that is the consensus view on PCE (no inflation in May). That would bring the year-over-year number down to 2.55% - a continuation of what the Fed perceives to be "a stall."