As we've discussed many times in my daily notes, we need a period of hot growth, rising wages (to restore the standard of living), and stable, but higher than average inflation to inflate away debt.

Yesterday's headline inflation for August came in at 3.7% - that's a second consecutive uptick in inflation, following twelve consecutive months of declining inflation.

It's far from the 9% of early last year, but it's double the inflation of the decade prior to the pandemic.

The Fed spent the better part of that decade using all of its tools to promote inflation - to escape the deflationary forces of a weak post-global financial crisis economy. Now, with this inflation number, we're probably looking at what will be a persistently "higher than average inflation" level - something hanging around 4%.

With the rise in oil prices, over the past two months, the upward pressure on this headline number, from here, is pretty much assured.

That said, as we discussed yesterday, this rise in oil prices further squeezes the consumers ability to keep spending (i.e. softening demand). So we may have a scenario in the coming months where the inflation that the media talks about is "hot," but the inflation the Fed is focused on (excluding food and energy prices) is not hot, but falling.

From the chart above we can see, if both core and headline inflation were to grow at around the average of the past three months (monthly rate of change), the paths would cross by the end of the year, and the core (what the Fed cares most about) would be in the mid-2s by mid-2024, which happens to be when the market sees the beginning of rate cuts.

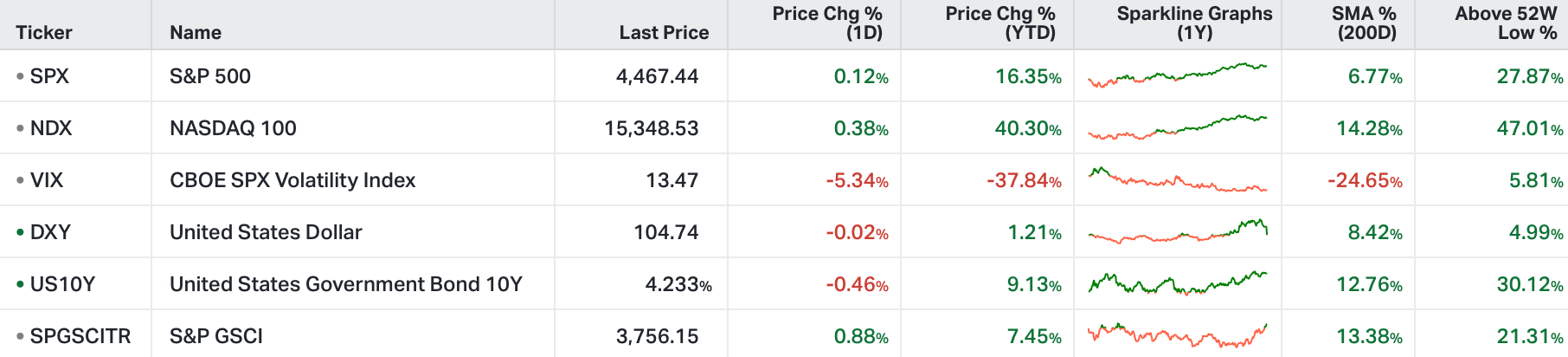

With all of this in mind, we ended the day with an "outside day" (a technical reversal signal) in the very important 10-year yield - that's a reversal signal into the 4.3% area in yields, which has proven a top on two other occasions.

Consider this: Going into the day’s inflation report, we've had a 30% rise in oil prices and a 55 basis point move in the 10-year yield, all since the end of the first half (end of June). Meanwhile, stocks (Nasdaq, S&P 500, DJIA) are left virtually unchanged over the same period.

Click on the link above to become a member of The GRYNING | Portfolio, where you’ll have access to;

Institutional Grade Portfolio’s - return characteristics similar to the hedge fund.

Actionable Trade Idea’s - stock, etf & crypto analytics powered by explainable artificial Intelligence

Broad Market Observations - robust relationships between a driver and a broad market etf’s subsequent price action.