We closed last week with the Jobs report on Friday morning - it wasn't weak, but it wasn't strong.

Following on from Thursday Macro Perspective, in this environment, bad news is good news. The Fed wants to bring demand down. Therefore, any data, to that end, is a "positive," because it takes the pressure off of the Fed to carry out a draconian campaign of aggressive rate hikes.

So, it wasn't good news, but it wasn't bad news (confused yet?).

The Fed has targeted employment, as a tool to influence demand lower, primarily through correcting the imbalance between job openings and job seekers. It's this imbalance (two openings for every one job seeker) that has given job seekers the leverage to negotiate higher wages.

How are employers dealing with paying a higher wage? They are passing it along to consumers through higher prices (inflation).

If we look at the wage component of Friday’s report, it may be signaling some softness. The month-to-month change is just 0.3% - annualised that's 3.7% wage growth. That's well below the roughly 5.5% year-over-year wage growth numbers we've seen over the past eight months.

And while it's not showing up in the employment data yet, we know that employers are pulling back on jobs.

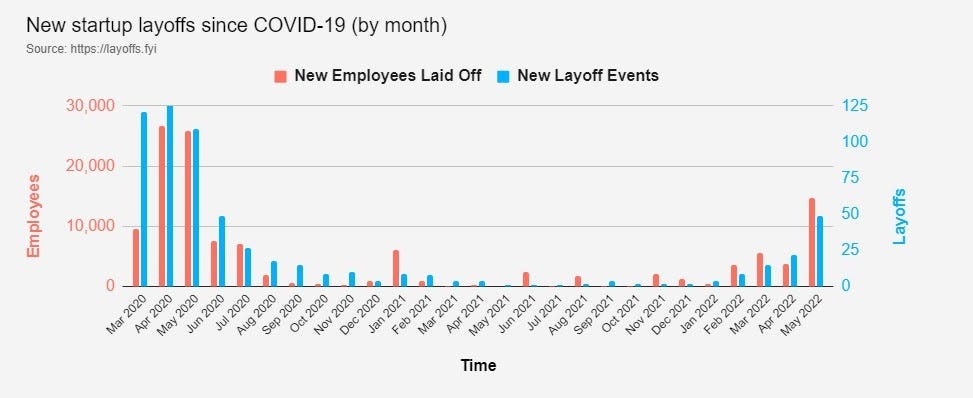

We looked at this chart above last week. With the telegraph of higher interest rates, and less liquidity in the system, the start up and early stage technology businesses had the biggest layoffs in May, since the depths of the lockdown-induced recession. Big tech is now announcing hiring freezes and headcount reduction too.

So, again, the market is doing the Fed's job for them.

Layoffs and softer wages sound like bad news…but it's good news within the context of the probable outcomes that are on the table. A looser labor market, softer wage growth, lower stock valuations and higher gas prices are a formula for lower demand. That should keep the path of interest rates shallow and, therefore, lower the probability of an economic crash scenario.

That said, the Fed's attack on demand will do little to contain the prices driven by structural supply deficits, namely oil. With that, a lower standard of living seems to be a common denominator in both the soft and hard landing scenarios for the economy.