Stocks in the US finished in the green on Tuesday, following a selloff in the prior session, as investors adjusted their expectations after remarks from Federal Reserve Chair Jerome Powell.

Powell suggested that a rate cut may not be imminent in March, leading to uncertainty among investors.

The technology sector experienced the most significant decline, while materials and real estate sectors showed resilience.

Meanwhile, earnings season reached its midpoint, as Palantir Technologies surged by 30.8% after announcing a higher-than-expected profit outlook.

GE Healthcare Technologies shares jumped 11.6% on upbeat earnings results.

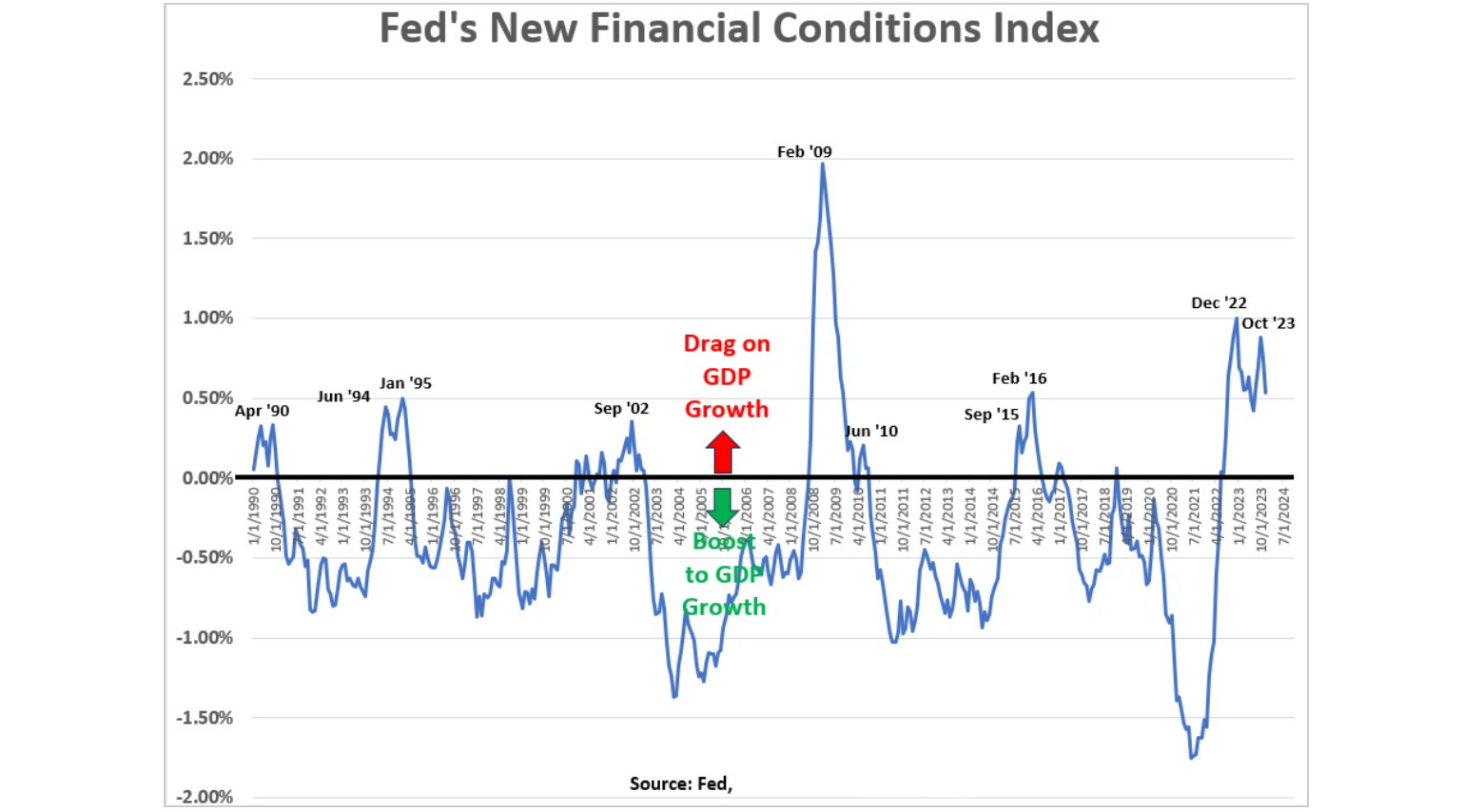

We've looked at the below chart on the Fed's New Financial Conditions Index over the past couple of months. Let's revisit this, and talk about how it relates to what the Fed did with "real interest rates" (Fed Funds rate adjusted for inflation) in the late 90s…

Remember, this index is designed to incorporate the lags of monetary policy, and project (in this case) one-year forward what the impact will be on real GDP growth;

if the line is above zero, it represents tight financial conditions, which project a drag on economic growth (from restrictive policy).

if it's below zero, it's a boost to growth (stimulative policy).

If we look back at moments when financial conditions were historically this tight (denoted in the chart above), every moment was soon followed with some form of Fed easing (either rate cuts, QE or, in the case of 2015-2016, removing projected rate hikes).

In the 1994-1995 period, the Fed continued raising rates into a low inflation, slow economic recovery. It was a mistake. Financial conditions were tight. By July of '95, the Fed did indeed start cutting rates (i.e. easing), and in doing so, they set into motion a boom-time period for growth and stocks. The economy went on to average 4.5% quarterly annualised growth through the end of the 90s, with stocks putting up five big, double-digit return years, averaging 26% per annum.

But as you can see in the next chart, the Fed kept real rates at historically high levels throughout this boom.

So how did the economy and markets do so well, with the Fed holding real rates high (which is restrictive to economic output)? We were in a technology revolution - rapid adoption of the internet. Productivity was high, inflation was low. The economy was booming, even with the Fed tinkering with interest rates around 5%.

So, with this late 90s period, we can see parallels to the current environment. Could the Fed hold real rates here (at historically high levels), and still get a boom-time period, driven by the technology revolution of generative AI?

Growth solves a lot of problems. But U.S. debt/gdp has doubled since the late 90s. And while the debt service/gdp is comparable to the late 90s period at the moment, it won't be as they continue to refinance at high nominal rates.

Does the Fed doesn't have the luxury to sit around and watch for long, or will they have to cut.

ps: You should become a member of our sister offering, GRYNING | AI - where we bring AI-derived market intelligence and actionable insights. The Daily free offering provides you with stock & etf ranking scores alongside a “Market Movers” section (example shown below).