Signals

Introducing GRYNING | Signals - providing durable and consistent return streams independent of beta.

One Membership | Two Solutions | Ten Strategies

Systematic Solutions

Access six quantitative strategies - not data mined and based on sound hypothesis about price action behaviour and the formation of anomalies - generate systematic trading signals with precise entries and exits in the weekly timeframe (for the open price of the next weekly bar). The strategies cover price series and cross-sectional momentum, mean reversion, and long/short with major ETFs and large-cap stocks.

STOCKBOND (SB) [252.037] is a long-only systematic tactical allocation (SPY & TLT) strategy using price series momentum for timing and cross-sectional momentum for position sizing.

MEANREVERSION (MR) [248.771] is mean-reversion strategy for SPY ETF based on sound mathematics that generates long-only signals while avoiding bear markets.

SECTORROTATION (SR) [372.141] trades several sector ETFs long-only based on momentum and can hold up to four ETFs at a time based on a ranking method.

ETFROTATION (ER) [510.173] trades several ETFs long-only based on momentum and can hold up to three ETFs at a time based on a ranking method.

DOWBULL (DB) [264.546] is a mean-reversion strategy based on sound mathematics that generates up to 6 long-only signals in Dow 30 stocks while avoiding bear markets.

LONGSHORT (LS) [148.555] is a long/short strategy that trades up to six stocks long/short from the Dow 30 group of stocks using a proprietary ranking method. The strategy is dollar-neutral: 3 long and 3 short stocks of equal dollar allocation.

Equity Performance | Six Strategies

Comparison of the Average Performance [329.553] of the five strategies excluding LONGSHORT (LS) to SPY ETF performance (Strategy vs Buy & Hold)

Annualised Return: 8% vs 9.3%

Maximum Drawdown: -8.3% vs -55.2%

Volatility: 7.7% vs 20.3%

Sharp Ratio: 1.05 vs 0.46

MAR Ratio (CAGR/MDD): 0.97 vs 0.17

The main benefit of using an ensemble of strategies is the low volatility of the equity curve. Leveraged alpha is possible while maintaining a low maximum drawdown. Note that the Sharpe ratio stays nearly constant under leverage. Yearly Return (%) charts for the five strategies ensemble and LS is shown on the next page.

Price: £500 / 3 months or £1500 / year (25% off)

Become a member: Quarterly Membership | Annual Membership

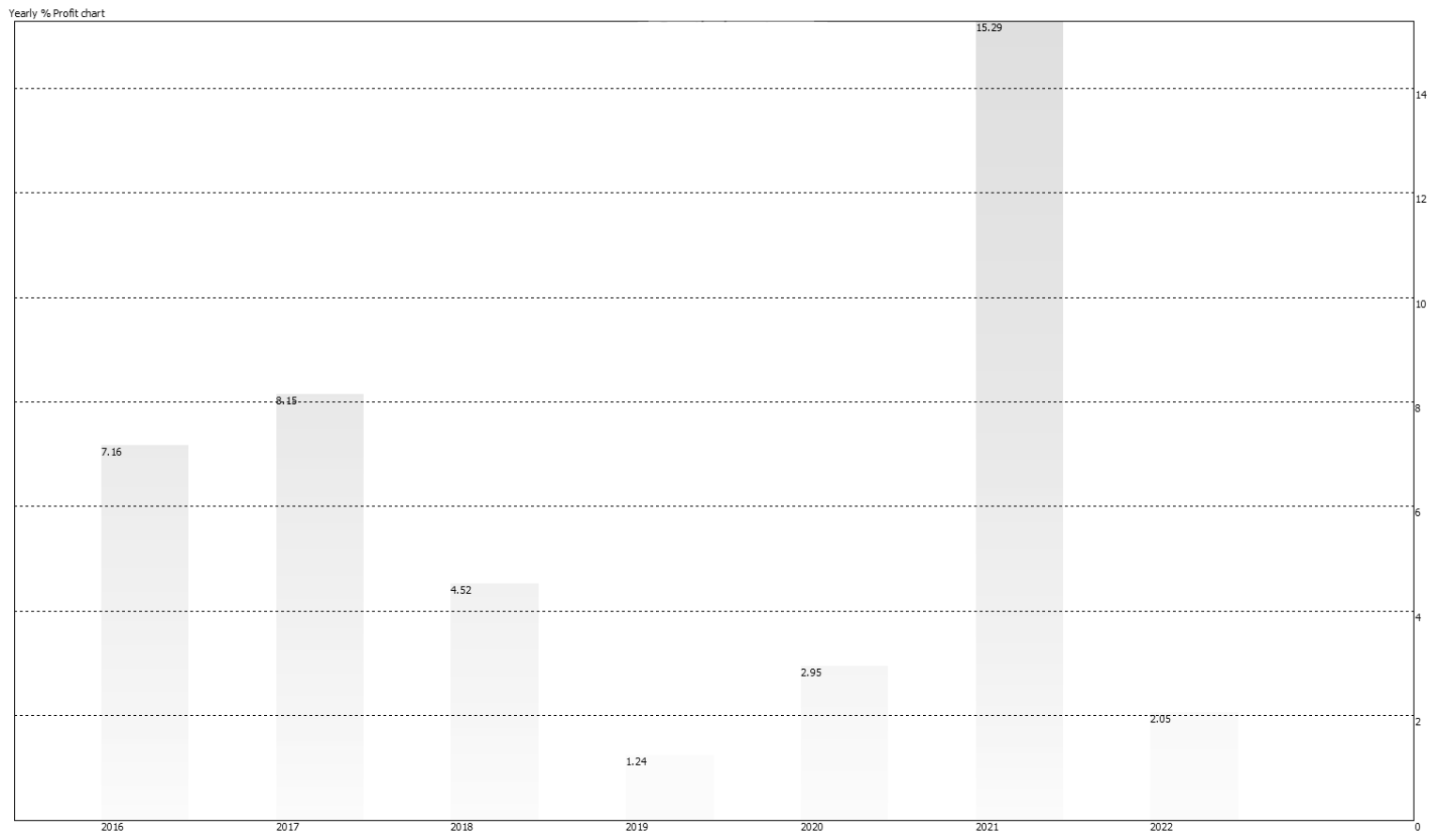

Yearly Return % | Five Strategies (excluding long-short)

Yearly Return % | Long-Short

Portfolio Solutions

Hybrid asset allocation (HAA) employs two strategies: asset cross-sectional momentum and strategic allocation. Both strategies use ETFs to generate signals.

The asset cross-sectional momentum strategy (CS) and the strategic allocation strategy (SA) generate signals in the monthly timeframe. The rebalancing of SA occurs annually and includes both tactical and passive components.

On top of that, we have also developed a dynamic momentum strategy. The Dynamic Momentum Strategy (DM) is a proprietary timing algorithm that trades the SPY ETF. Its objective is to maximise the Sharpe ratio and avoid market corrections. It generates signals on a monthly basis.

The signals of both HAA and DM are available after the last trading day of each month. We provide precise entry and exit signals every month.

Relative performance of HAA [68.17], CS [77.03], SA [59.32], DM [87.13], and SPY [75.11] ETF, January 2, 2020 to May 31, 2024

The orange line shows the performance of the HAA with a 50% allocation to CS and SA. Since 2020, the total return for HAA is 73.3%, and for SPY ETF, it is 83.5%. Below is a performance comparison table for HAA vs SPY from January 2020 to July 2024 (in the monthly timeframe).

Annualised Return: 13.0% vs 14.1%

Total Return: 73.3% vs 83.5%

Maximum Drawdown: -5.9% vs -23.9%

Equity Volatility: 8.8% vs 18.8%

Equity Sharp Ratio: 1.48 vs 0.77

Equity Beta (S&P 500): 0.24 vs 1.00

The Sharpe ratio of HAA is nearly double that of a buy-and-hold SPY ETF. The maximum drawdown is about 25% of the drawdown of the buy-and-hold SPY ETF.

Yearly Return % | HAA

The annualised return is 7.7%, with a 10.2% maximum drawdown. The Sharpe ratio stands at 0.97. These results allow the application of 2X leverage below to give an annualised return of 11.3%, with a 13.3% maximum drawdown. The Sharpe ratio stands at 0.97.

The Dynamic Momentum Strategy (DM) is a proprietary timing algorithm that trades the SPY ETF. Its objective is to maximise the Sharpe ratio and avoid market corrections. Signals are generated monthly.

YTD Performance (no leverage): 16.6% Return | -4.0% YTD Max Monthly Drawdown

Yearly Return % | DM

Annualised Return: 9.7%

Maximum Drawdown: 18%

Sharp Ratio: 1.08

Total Trades (since 2005): 22

Win Rate: 91%

Average Profit/Loss: 9.3%

Market Exposure: 65%

The analysis of the results shows that this strategy has avoided the 2008, 2018, 2020, and 2022 corrections. According to historical backtests, DM has the potential to reduce risk while improving performance based on risk-adjusted returns. The strategy’s high win rate, reduced market exposure, and high Sharpe and skew ratios can help decrease the probability of experiencing a significant loss.

Price: £500 / 3 months or £1500 / year (25% off)

Access Signals: Quarterly Membership | Annual Membership

Start Date: Monday, September 02, 2024

Limited Membership: 10 annual & 30 quarterly memberships are available.

No ambiguity, no buzzwords, no fundamental analysis, no obscurantism: well-defined entry and exit signals for major and liquid ETFs.