Short-lived...probably not.

Macro Perspectives: Tue 01 Mar 22

Let's take a look at the fireworks in Russian financial markets…

Below is a chart of the appreciation of the U.S. dollar vs. the Russian ruble. The price changes highlighted in this chart represent the start/end of the Russia/Ukraine conflict in 2014, and the start (November) of the latest conflict, to present, in the far right.

NB: I distinctly remember price spiking to 80 during the Crimea crisis. Sadly not shown in the chart above!

Observation: If we look back at 2014, when Russia ultimately annexed Crimea, the damage to the Ruble was worse (I’m pretty sure it get to 80.00) - about twice as bad as the current case (thus far). But it's early.

When the currency is collapsing (from a combination of capital flight and speculation), the central bank has to step in and become the buyer of last resort (defend the currency). But to buy rubles, the Central Bank of Russia has to exchange foreign currency, from their reserves. This is where it becomes dangerous for Russia. When the central bank is selling dollars and buying its own currency all day, every day to fend off speculators it can quickly bleed the country's currency reserves (a component of the country's global net worth).

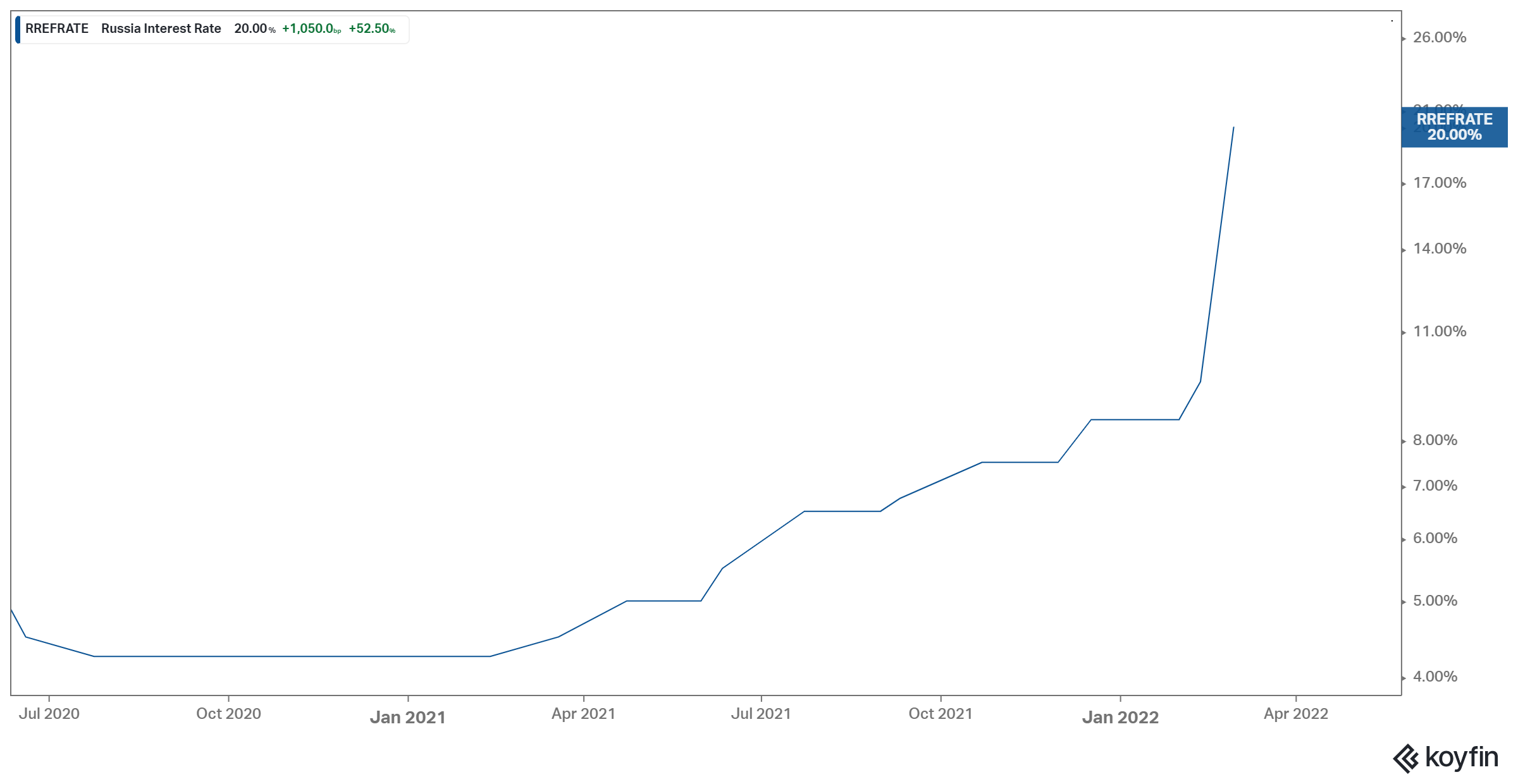

With the above in mind, Russia ratcheted up short term interest rates yesterday from 8.5% to 20%!

For any speculators now trying to short the ruble, they now have to pay an overnight interest rate of 20% - that will end a speculative rout quickly. That's precisely what the Bank of Thailand did to George Soros back in the late 90s, when he was trying to force a devaluation of the Thai baht. They chased him away by spiking the overnight interest rate, but, they ultimately did give way to a big currency devaluation.

Thus far, the Russian central bank comes into this crisis with a larger war chest of foreign currency reserves (as you can see in the above chart)...and a customer, in China, that will probably be happy to buy all of the oil Russia will sell them (if the West were to go farther down the road of sanctions).

So, this confrontation building between Russia and the West probably won't be short-lived.

A market related historical nuance: After initial risk aversion due to increasing international tension, markets tend to recover on actual conflicts on the first shot fired in anger. This trend tends to persist.