Seem's Likely

US stocks closed mixed on Wednesday, after marking their worst day since early August in the previous session.

The S&P 500 edged lower by 0.1%, the tech-heavy Nasdaq lost 0.3% while the Dow Jones gained 37 points.

Energy shares led the declines, with Exxon Mobil and Chevron falling 1.2% and 1.7%, respectively.

Tech shares also underperformed as Nvidia’s stock dropped 1.6% amid AI concerns.

Intel lost 3.3% after Reuters reported that the company's silicon wafers failed tests conducted by Broadcom.

As we head into Friday's August jobs report, we had another signal that the labour market has chilled.

The job openings data (JOLTS) kicked off what should be a series of soft employment data through Friday. The JOLTS report is of particular interest because Jay Powell specifically isolated this data point early in the tightening cycle.

After the first rate hike in March of 2022, he launched a verbal attack on demand, and when asked what mechanisms he would use to reduce demand, he said this:

"If you look at today's labour market, what you have is 1.7-plus job openings for every unemployed person. So that's a very, very tight labour market — tight to an unhealthy level…. We're trying to better align demand and supply, let's just say in the labour market. So, if you were just moving down the number of job openings so that they were more like one to one, you would have less upward pressure on wages [and] you would have a lot less of a labour shortage" … "and that, over time, should bring inflation down."

So, where does yesterday’s report leave us? 1.07 job openings for every 1 job seeker.

So, the Fed has achieved its goal. The question is, will it come at the expense of an economic recession?

It seems likely.

For the past fifteen months through July the unemployment rate is up 9/10ths of a point above the cycle low (3.4%). The speed of this change in joblessness puts it in the unique company of the past four recessions (which came with, in each case, reactionary Fed rate cuts).

The 2-year yield is now 159 basis points lower than the Fed Funds rate. The bond market is telling us the Fed is way behind the curve — too slow to recognise the deterioration in the job market (and the economy).

With the plunge in the 2-year yield over the past month (down 65 basis points since July 31), the yield curve is nearing a return to a positive slope, after two years of inversion.

Yield curve inversions are historically predictors of recession. When the curve turns positive again, it tends to indicate an economy has either entered or is about to enter recession.

On that note, remember, during their respective tenures as Fed Chair, both Bernanke and Yellen said that economic expansions don't die of old age, the Fed tends to murder them.

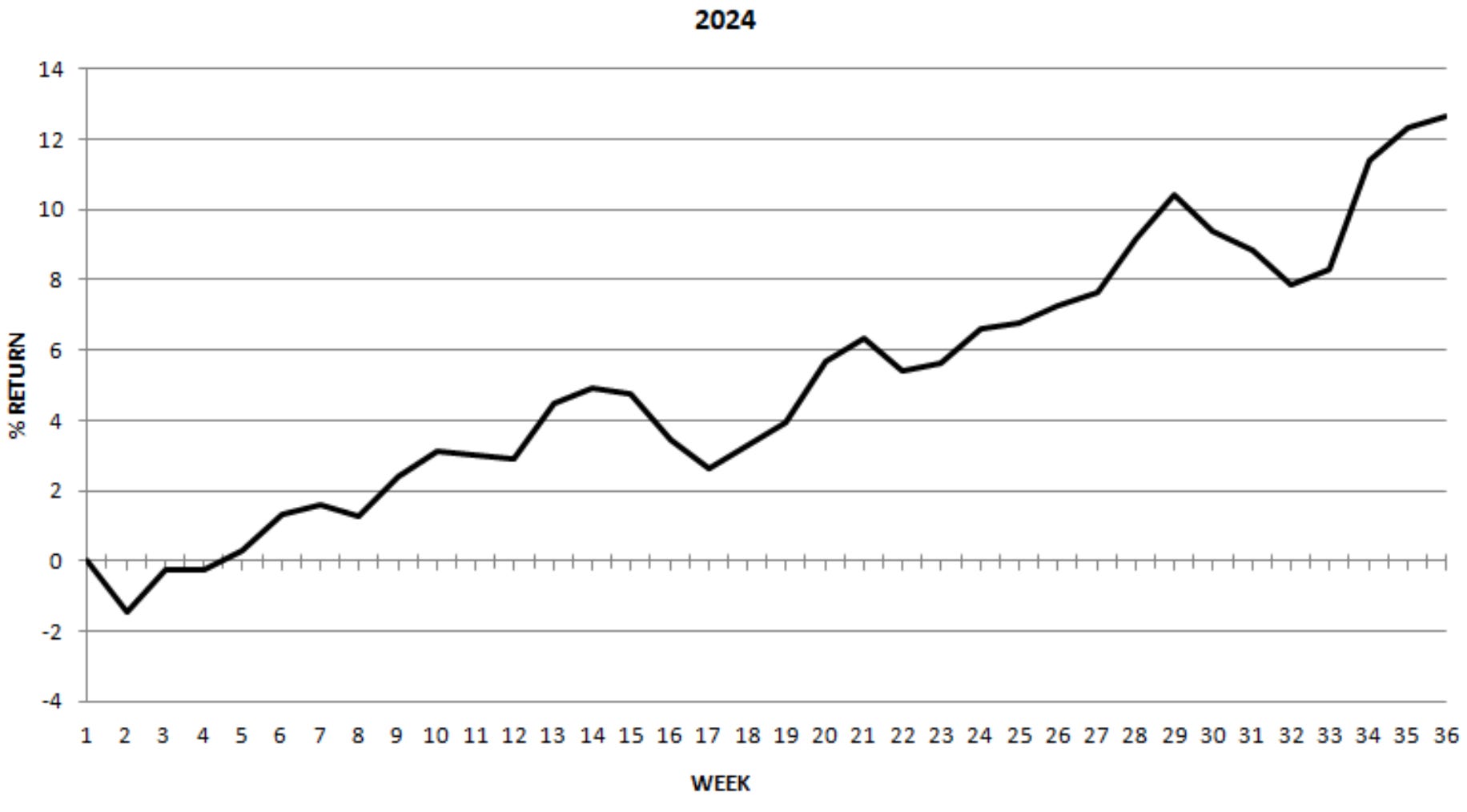

New equity highs for the year from the ensemble of six weekly strategies; +12.6% vs -2.5% drawdown.

This is for those who despise drama, but there are no guarantees.