We looked at this chart, in my note “Skip”, last week ( here ) . . .

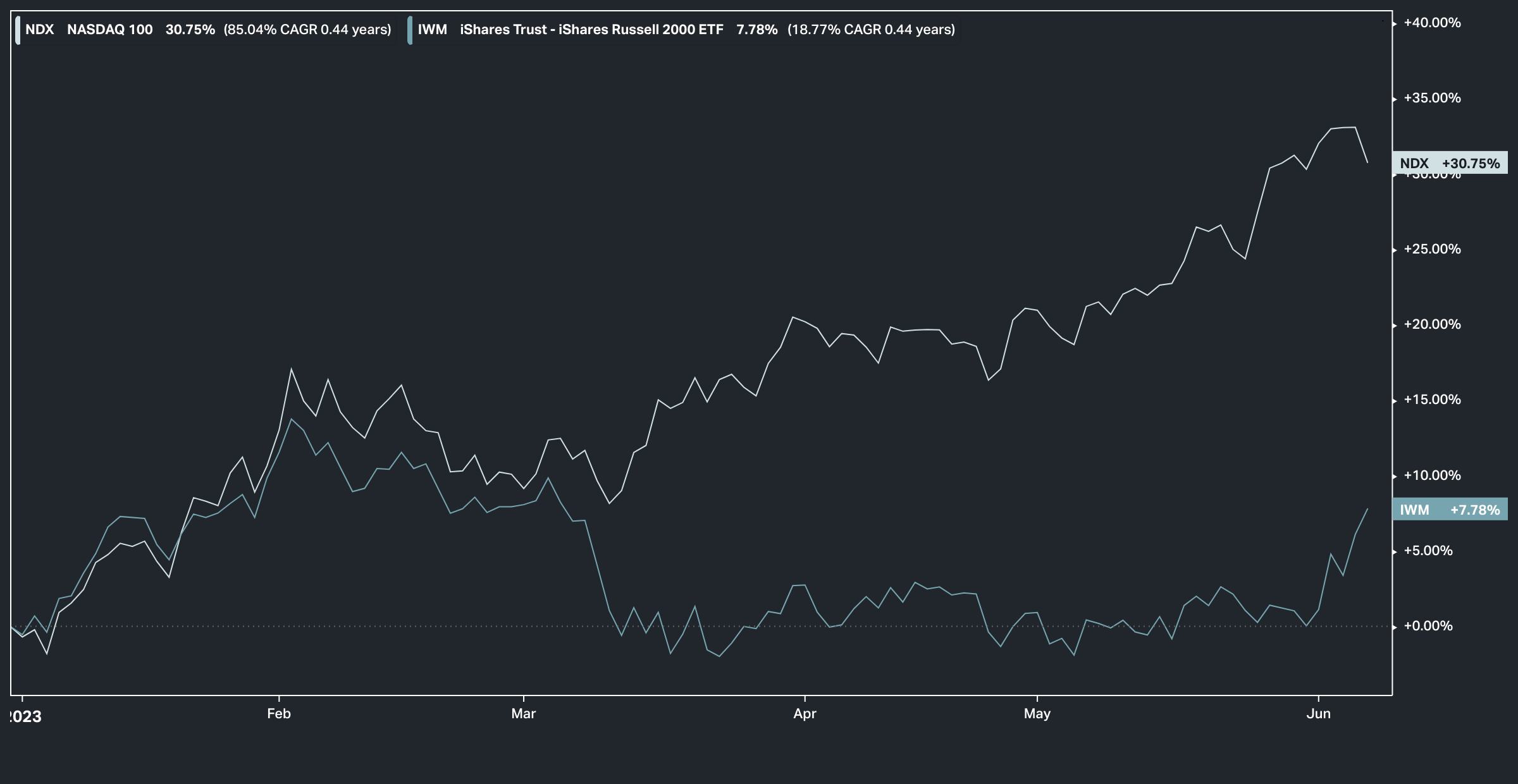

The big-tech driven Nasdaq was outperforming the broader small cap market by more than thirty percentage points on the year.

That gap is closing aggressively, helped by the nearly four percentage points of outperformance yesterday, by the Russell 2000.

We've had a market that has been positioned for a hard landing, bearish outcome. Yet, the overhang of risks have been removed one by one;

Debt limit decisions are now, not only pushed out to 2025, but the Treasury now has license to issue unlimited debt between now and then (a greenlight, if given an excuse).

By next month, we should be seeing a headline inflation number in the mid 3s (percent), thanks to the “base effect” - which inturn has the Fed chattering about a “skip” in the rate hiking campaign (otherwise known as pausing, more likely ending).

The bank shock has proven to be just that: a shock, not a crisis.

That said, there was news a couple days ago that the Fed may be looking to hike bank reserve requirements by 20%. The last time I checked ( here ), they took the reserve requirement to zero, during covid, and haven't changed it since. That gave banks a license to make unlimited loans. While twenty percent of zero is still zero, perhaps it's a signal that the Fed is cleaning up some bank risk.

So, with risks being removed, the investors that have been positioned on the wrong side this year (which includes underinvested in equities), seem to be buying the market laggards.

PS: In the 01June23 note, “Skip”, attached above I included the Chartbook sent out to members on the previous day. Within which was an actionable trade idea (shown below) allowing you to get MidCap exposure via $EZM.

For less than a coffee a day, Gryning Portfolio members received the above analysis on a ticker that is now up circa 8%.