Risk On & perhaps some Hedging

Macro Perspectives: Mon 8 Nov 21

The jobs numbers on Friday confirmed what should be a reasonable assumption: When you stop paying people to stay at home, they will go find a job.

In this case, from July onwards, more than half of the states have rejected the federal unemployment subsidy. So whilst the August and September job’s growth came in under expectations, those numbers have since been revised UP and Friday’s October numbers came in better than expected.

Averaging the job growth over the past six months, we get 665k jobs added a month. That's big and that's on an unemployment rate that came in at 4.6%.

That's more than three times the job growth underway when the Fed started normalising rates back in 2015, with a lower unemployment rate (currently), by 40 basis points. Add to this, the health czars are touting the trial success of another oral therapeutic against Covid.

This should all signal a sustained, strong economic recovery, which should be a greenlight for stocks, commodities and interest rates (yields).

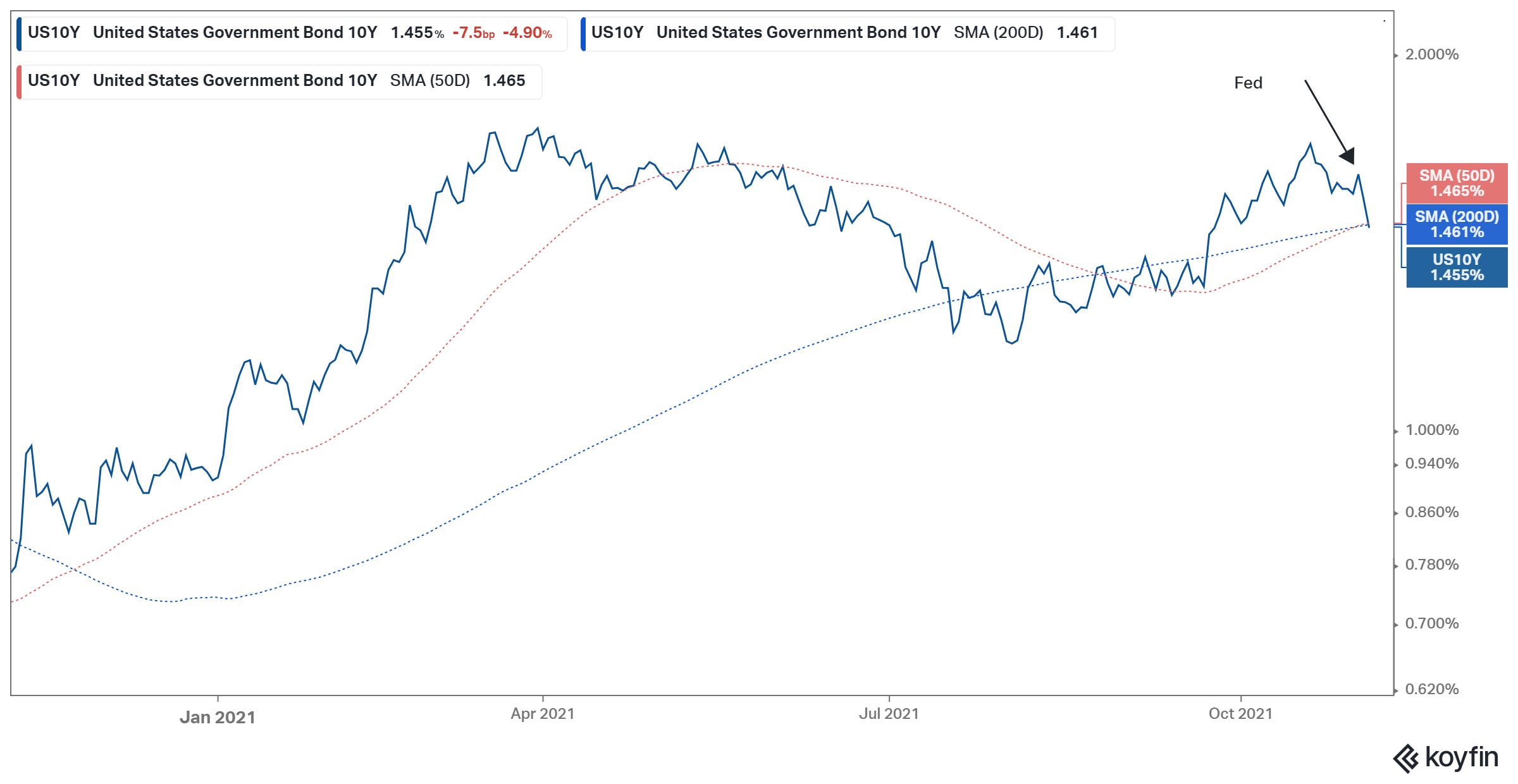

Stocks and commodities played ball, but yields went the wrong way sharply.

As you can see in the chart, there was a lot of bond buying (price goes up, yield goes down), despite the positive news on the economy and on the pandemic front. The move in yields was global, European yields were down sharply on the day too (note the hump in the yield performance chart below).

Not only that, but gold had one of its best days of the year (only 12 days better) - finishing on two month highs. Whilst the vix was up 5% on the day, despite broadly positive stocks.

Bottom line: It looks like there was some hedging of risk going into the weekend.

Perhaps there is some fear of an ugly unwind, of some of the bubbly tech stocks that have done so well in the pandemic period. This one comes to mind...