Within finance we talk about risk at great length, so it's worth spending a moment on exactly what we mean. As traders and investors, we usually talk about risk in terms of volatility – or the degree of uncertainty we have about future portfolio returns. This approach is also conveniently powerful in allowing us to model different possibilities and work from a simple set of assumptions about individual asset classes to make reasonable conjectures about how portfolios will behave.

The downside to this approach is that, while some people find it very intuitive, others find it alien.

For example, many investors argue – with some reason – that the uncertainty about future returns doesn't matter on the upside, only on the downside. "Surprises" relative to my expectations are only bad if they cost me money. For these investors, risk generally means the risk of losing money; their preferred risk measures will give them some sense of how much they will lose (or could possibly ever lose) in a bad outcome. Of course, the latter can be difficult (or impossible) to quantify – or, perhaps, be the not-very-useful "you could lose 100% in some shockingly worst case scenario that we can barely imagine."

The good news is that our standard volatility measure of risk is usually not unrelated to the "reasonable worst-case scenario," which means that investors can – and should – use both portfolio volatility and some notion of possible future loss in assessing the risk of various investment strategies.

The most important thing is not to take either of these measures as written in stone, but to give some thought to what they do and do not encompass. For example, volatility calculations assume a normal world ("normal" in the statistical sense and the common-sense one) – one in which a hundred-year-flood occurs every hundred years or so. But we know from experience that finance is not a "normal" world and that we seem to get a hundred-year-flood every decade or two.

Planning accordingly is key.

Likewise, a "worst-case" scenario based on how some investment (or group of investments) has performed over the last eighty years of recorded data may give us some intuition of what a worst-case scenario could be going forward, but is far from the definitive word on what the future might hold (it could be wildly pessimistic based on some never-to-be-repeated disasters, or optimistic based on some yet-to-be-seen disasters).

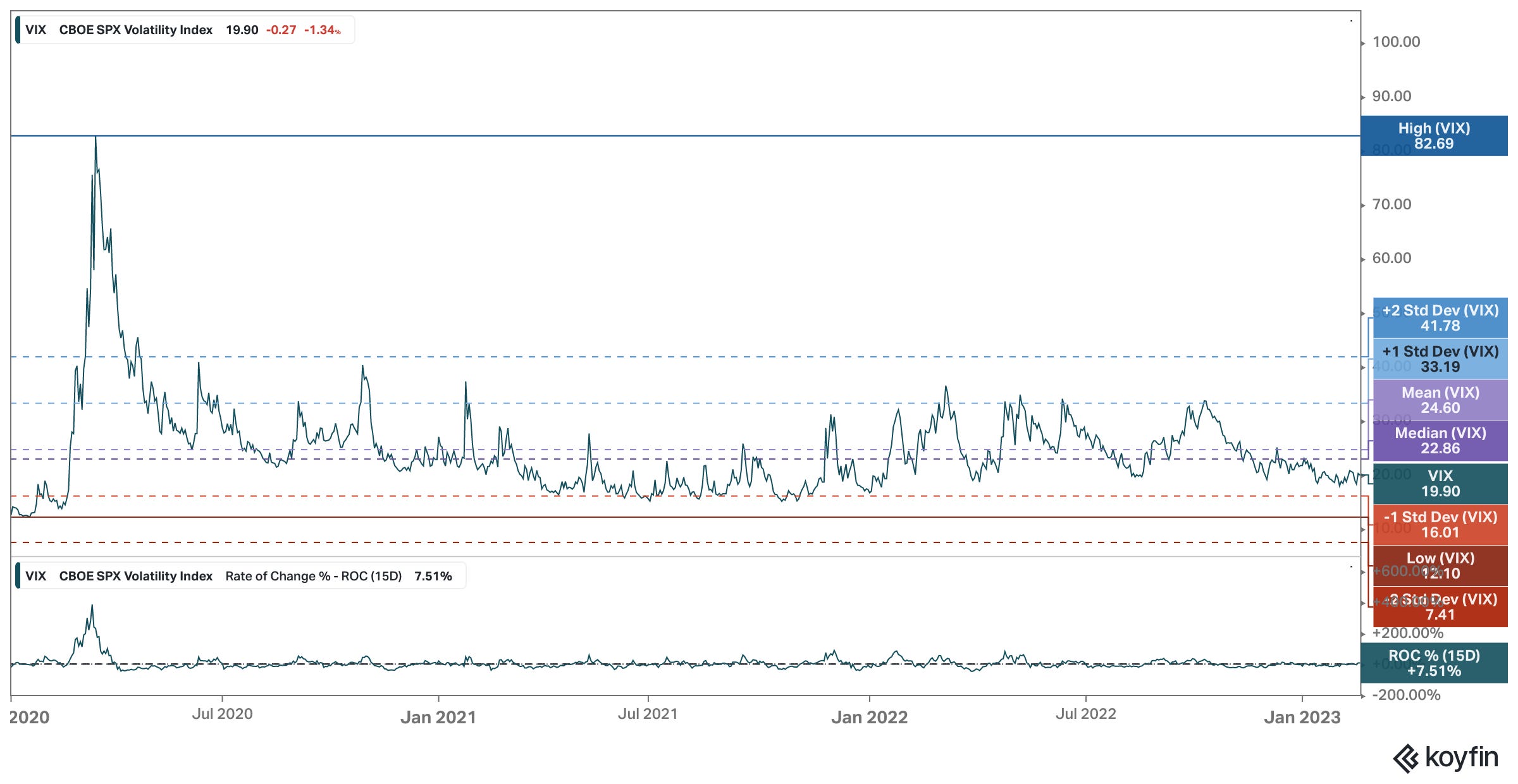

Today’s long form note looks at the VIX and how the increased use of very short-dated SPX options coupled with market maker concentration is likely making the VIX as sensitive as ever.