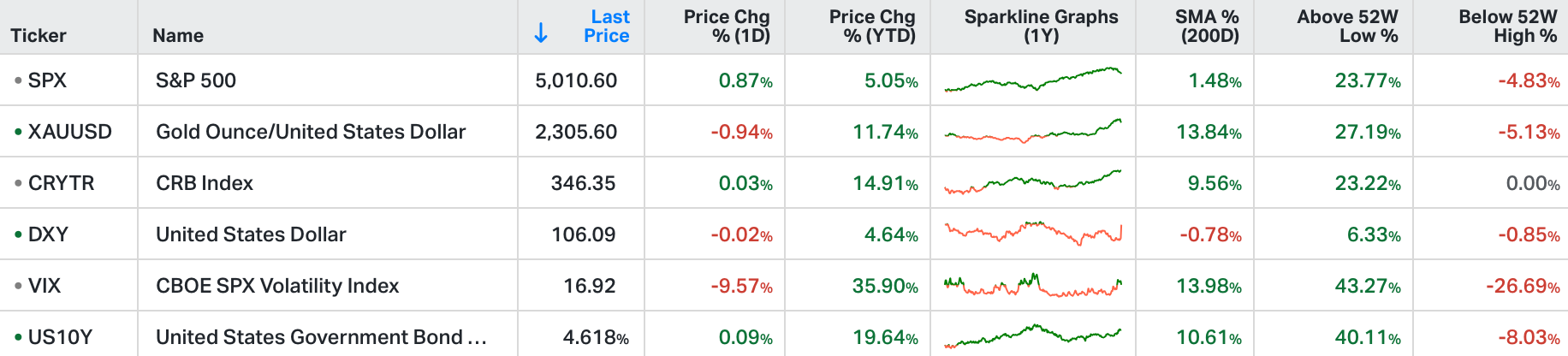

All three major US stock indices ended Monday's session higher, rebounding from their worst week of the year.

The S&P 500 and the Nasdaq added 0.8% and 1.1%, breaking their 6-day losing streak, and the Dow advanced 254 points.

Microsoft, Meta, Alphabet, Tesla, and American Airlines are set to report their quarterly results this week.

In addition, market watchers will closely monitor US GDP growth figures, PCE inflation data, and S&P Global PMIs.

Nvidia shares bounced back, rising 4.3% after a 10% decline on Friday.

We've now had an 8.5% drawdown in Nasdaq futures over the past month. S&P futures have lost 7% peak-to-trough. The small cap index, -11.6%.

That brings us to earnings week for half of the tech giants. We'll hear from Meta on Wednesday, Microsoft on Thursday and Alphabet (Google) on Friday. And the "not-so-giant" (at the moment), Tesla reports today.

With the exception of Tesla, they will all put up big numbers. Keep in mind, these are the companies working on the frontier of generative AI, a technology expected to be so life transforming that it has been compared to the advent of electricity.

These tech giants are investing tens of billions of dollars in AI infrastructure - they're developing the AI models, and products and services surrounding those models, that will power the Fourth Industrial Revolution. They are building the products and services we will all be using for the foreseeable future.

With that, as we've discussed, from the Nvidia moment of last May, the competitive moat only grew wider for these monopolies.

Why? They are among a limited class that can afford to buy the computing power to meet the demands of generative AI. Moreover, they control the deepest and most diverse data in the world, with world class talent. If they weren't modern day oil and rail barons before generative AI, they are now.

So, we've now had a correction in the broad stock market. Is it over?

As we've discussed here in my daily notes, the technical reversal signal in stocks, back on April 1, was triggered by Israel's strike of the Iranian consulate in Syria. With that, the market correction may have ended with what appears to be the end of the tit-for-tat Israel/Iran attacks, with Thursday night's "limited" strike on Iran by Israel.

That presents a catalyst, in this week's earnings from the AI barons, for a resumption of the economic and stock market boom (at least in nominal dollar terms).

On the economy: We'll get a first estimate on Q1 GDP on Thursday, which the Atlanta Fed GDP model projects to be a strong 2.9% annual rate.

Then we'll get March PCE on Friday (the Fed's favoured inflation gauge). On that note, the pendulum on rate path expectations has swung from one extreme to the other, over the past four months. That sentiment extreme means the risk of a negative market outcome from the data should be very limited, which means a positive surprise would provide a burst of fuel for markets.

I encourage you to check out Gryning AI and Gryning EDGE - your personal quant(s) that allow you to make smart, data-driven decisions.