Retail Sales Ahead of Inflation

Macro Perspective: Fri 25 Jun 2021

Last month the great macro trader, Stanley Druckenmiller, criticised (this is not unusual for him) the Fed in an interview. While arguing his case for why the Fed should not only stop its emergency stimulus program and it should be tightening now, he brought up the recovery in retail sales.

With that, let's take a look at the point he was making. He said, the recovery in retail sales is "nothing we've ever seen," comparing the speed at which the losses were recovered in this crisis, to the Great Financial Crisis.

Let's take a look at that chart ...

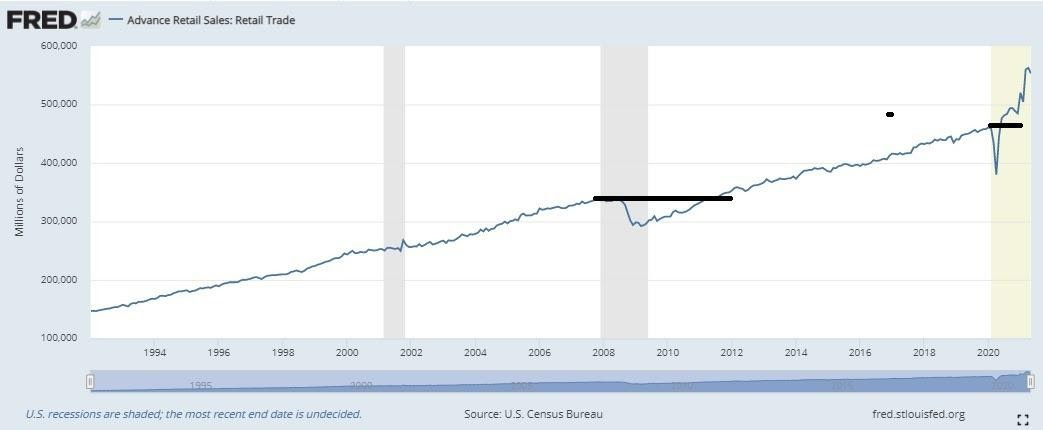

Now, we can see in the chart, the retail sales index peaked in November of 2007. It recovered to peak levels in July of 2011. That's a little less than four years.

Just recovering the losses is one thing, but getting back on "trend" (trend growth) is another. To recover to trend, if we compound the growth in retail sales by the long-term monthly average, my calculations show that we still have not recovered to pre-Great Financial Crisis trend (but getting close to doing so, now).

That said, this time around, the pandemic induced losses were fully recovered AND back on trend in just five months.

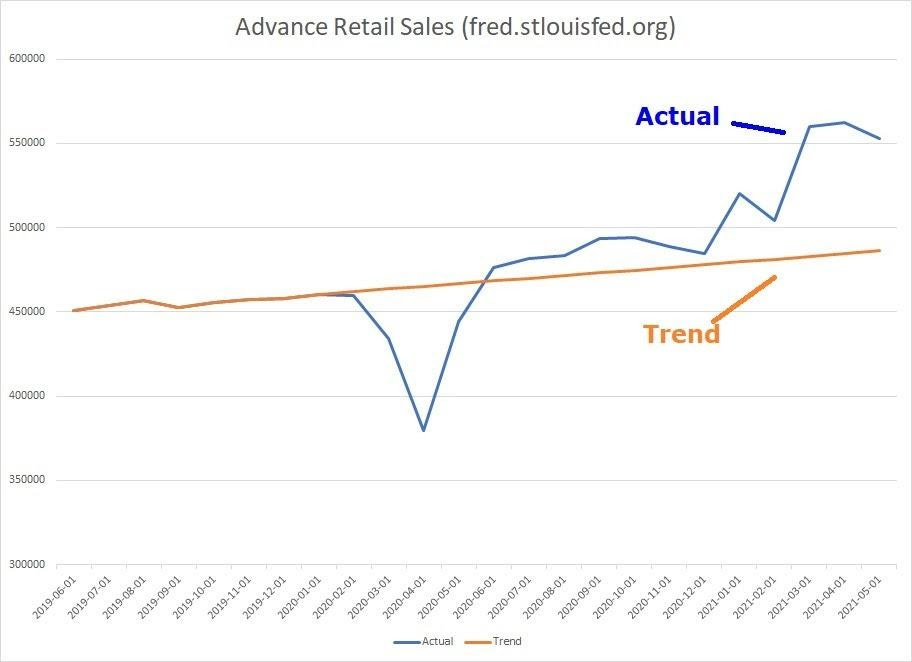

Here's the bigger point made by Druckenmiller: If we just look at the growth rate applied to the pre-pandemic highs in retail sales (January of 2020), the retail sales data is well above trend. It's running exceptionally hot. In this case, low inventories and strong sales will present the opportunity to raise prices. And with that, this sharp retail sales recovery will likely predict hot inflation.

Given the Fed has told us they will let inflation run hot, above their target until they deem it to be sustainable, we will likely see a similar chart in the inflation data in the coming months (i.e. overshoot).