Research Roundup: May 08, 2025

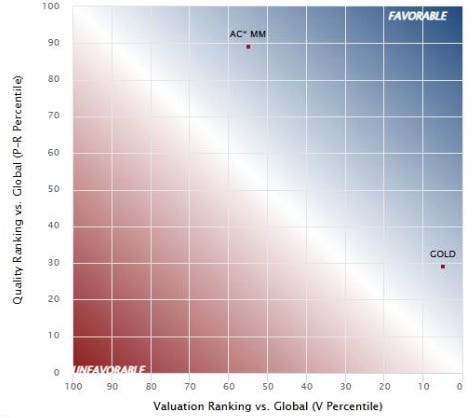

Our HEAT map is the visual trade-off between Quality and Valuation: companies in the favourable (blue) area offer higher quality and/or cheaper valuation than those in the unfavourable (red) area.

Names in the News: Barrick Gold (GOLD) & Arca Continental (AC* MM) - membership

This week, we look at two areas where investors have been focused on YTD, namely Gold and Latin America (LatAm). Within the Gold Space we look at the Canadian Gold miner, Barrick Gold Corporation (GOLD, rated ‘Overweight’) From Mexico, we look at the Coca Cola bottler, Arca Continental, S.A.B. de C.V. (AC* MM, rated ‘Overweight’).

Mag 7 & PRV Estimates - membership

The sell-side consensus has seen little in the way of adjustment for the Magnificent Seven (Mag 7) names (Apple, Microsoft, Alphabet, Amazon, Nvidia, Meta, and Tesla) this year. In this report we use the newly added ‘PRV Estimates’ metric to look at how good consensus has been at predicting the future, for each of the Mag 7 firms.

The red lines are the actual numbers, the blue lines are the projected 1-yearforward numbers, and the grey lines are the projected 2-year-forward numbers. This will be illustrated in the company analysis section starting on the following page. The blue shaded area is the absolute stock performance.

Communication Services: Entertainment - membership

Approximately 300 companies have reported earnings since our Global Communication Services 2025 Outlook roadmap was published in January. We look at the percentages of companies reporting a new positive inflection and a new negative inflection as well as the percentages of companies with positive PRV Momentum and negative PRV Momentum. The Entertainment industry has seen the highest percentage of new inflections up (32.4%) – these are companies that had been seeing declining momentum but in the latest quarter saw momentum improve.

Industry Snapshot: Global Industrial Conglomerates - membership

The aggregate industry PRV Margin (profitability) has significantly deteriorated over the past 2 years, trending near zero percent at the end of March. PRV Momentum (growth) had seen some recovery in H2 2024 but remains negative, given a continued contraction in EBITDA Margin and worsening capital intensity. Investor expectations for a recovery in value creation are relatively elevated at a time when economic Profitability is depressed. A potential recovery in Profitability could see expectations being met going forward, however, we are yet to see a bottoming in PRV Profitability and the Quality-Valuation tradeoff remains unfavourable.

Quant Corner: May 1, 2025 - membership

PRV spreads were positive in Europe, the United Kingdom, Asia ex Japan, Emerging Markets, and the Global universe through the final week of April. Quality continued to work everywhere as investors sought out safe havens. Cheap Value outperformed expensive Value in AxJ, the Emerging Markets, and the Global universe.