Real vs Financial

US stocks closed mixed on Friday, as recent data brought down expectations for Fed interest rate cuts.

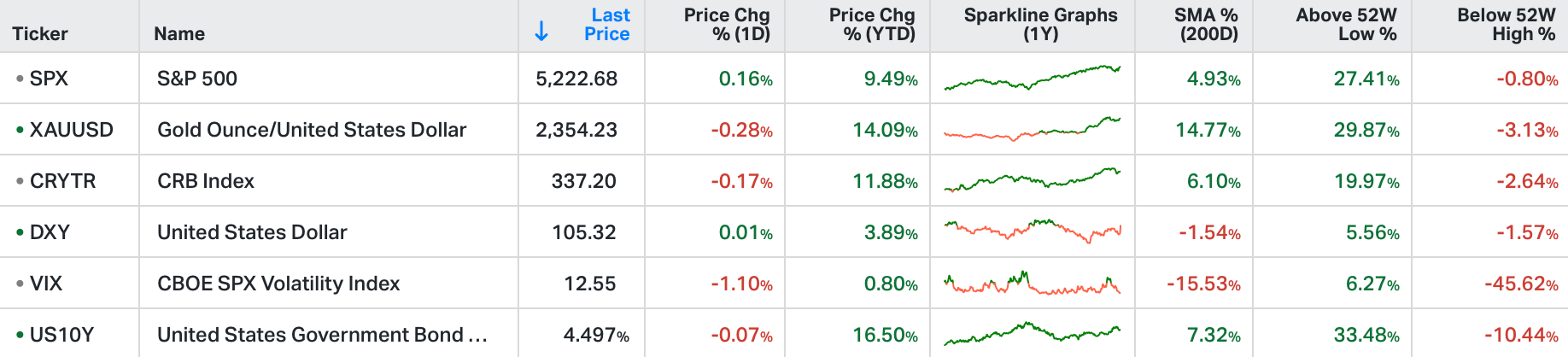

The S&P 500 added 0.1% and the Dow Jones marked an 8-day winning streak, advancing 124 points, while the Nasdaq ended marginally lower.

This added up to fresh comments from a Fed official advocating a cautious stance on lowering interest rates, as they weigh surprisingly strong inflation data this year.

Among megacap stocks, Nvidia gained 1.3% while Tesla dropped by 2%.

Novavax shares soared 98% after the vaccine maker announced a multi-billion dollar deal with Sanofi to co-commercialise its Covid vaccine starting next year.

Commodities (‘real’) are trading cheaply compared to equities (‘financial’), which may present an opportunity to prepare portfolios for higher and more volatile inflation.

The latest data – especially in the US – shows that disinflation has stalled. Core CPI rose at a three-month annualised rate of 4.5% in March and core PCE – the measure targeted by the Federal Reserve (Fed) – ticked up to a three-month annualised rate of 4.4%.

Both uncomfortably above central banks’ 2% target.

There is a growing risk that inflation will be both higher and more volatile than the market (and the Fed) currently expects - another uptick would threaten richly valued equity and credit markets.

Even with the strong rally we’ve seen over recent weeks – with history as a guide – commodities are as cheap as they have ever been. If one were to explore asset class performance during inflationary episodes across the US, UK and Japan over the past 100 years, bonds and equities tend to do badly . . .

. . . commodities perform very well.

Whilst investors have been loading up on bonds and growth equities in the hope of imminent rate cuts, if interest rates stay higher thanks to a motoring US economy, there is potential for commodities to be a key diversifying asset in a world where 2% is the inflationary floor rather than the ceiling.

It’s also worth noting that whilst gold played a role in the broader historical outperformance of commodities, it was found to be unreliable on its own, having returned 13% annualised on average, but with positive returns only two thirds of the time.

A diversified basket of commodities appears to be the key.