As we near the end of year, let's take a look at year-to-date performance of global assets.

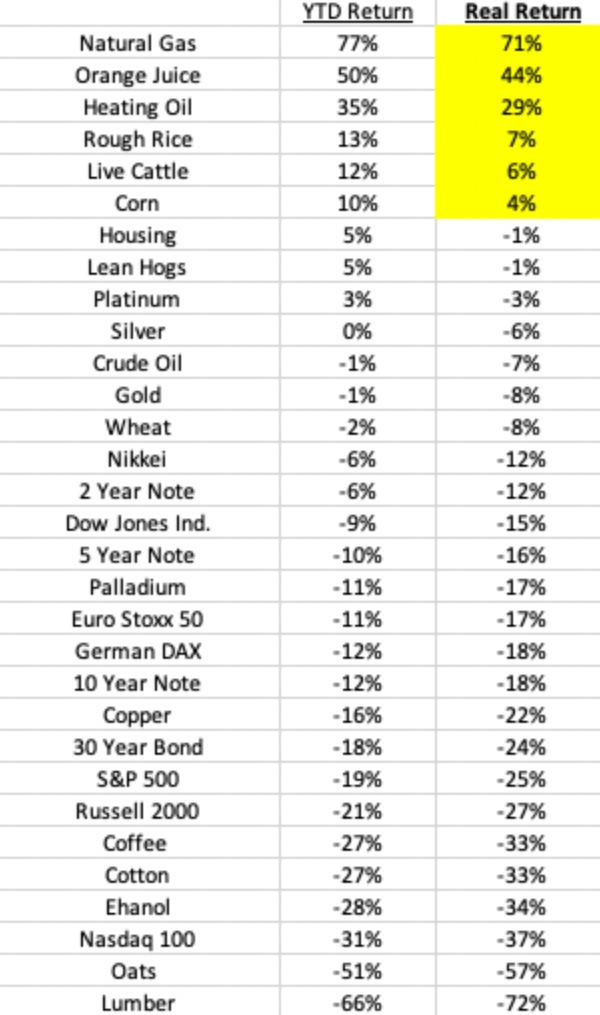

As you might have expected, there are a lot of negative return assets on the year.

But things become even uglier when we adjust for inflation (the "real return"). In that case, we see fewer positive returning assets on the year, and those positive real returns are largely driven by the supply disruption in energy and grains, associated with the Russia/Ukraine conflict.

So nothing in this table of returns would suggest an over-demand problem in the economy (certainly not now). However most of what we see in this table is caused by the Fed's policy actions to act on their stated goal (disclosed in their March meeting) to "bring demand down.”

Meanwhile, wages, after adjusted for inflation, are negative on the year. Personal savings, as a percent of discretionary income, have gone to just 2% (almost nothing). That's record lows, going back over 60 years of history.

The question isn't "will the Fed cut rates next year?" The question is, how soon will they be forced back into quantitative easing - the Hotel California of monetary policy ("you can check out, but you can never leave").

If you havn’t yet, you should pick up The GRYNING | Essays - the clearest way to see the financial markets of 2022.

You should probably join The GRYNING | Portfolio - you get access to hedge fund strategies for less than a coffee a day.