ZEW Experts Shift Forecasts: Less Pessimistic on Europe

The ZEW Forcast

In this month’s ZEW survey, there is an example of what I consider to be somewhat quizzical forecasts being offered by the ZEW financial experts, who are largely European experts, at a time that the United States is threatening tariffs. Now this, of course, makes the U.S. the aggressor in this campaign, and according to the ZEW experts, the U.S. is going to suffer from this more than European economies. However, the U.S. is much less trade-dependent than Europe and certainly far less dependent than Germany, which is one of the most trade-dependent large, advanced economies in the world. We measure trade dependency by looking at exports plus imports as a percentage of GDP. By this measure, trade dependency is around 90% to 95% for Germany; U.S. dependency is around 30% to 35%. The ZEW experts see the tariff situation making the U.S. economy much worse off than the European or the German economy- why?

Tariff impact

To put this in perspective, in the U.S., high tariffs, if they are binding, will cause imported goods to be more expensive. U.S. firms and consumers will have the choice of deciding whether they want to pay the higher costs to consume those items or to replace them in consumption or their production process. In the case of consumers, it's probably easier because a consumer can switch from an expensive French champagne to a less expensive but still quite good California sparkling wine or Chardonnay - or pay the higher price and enjoy French champagne! However, if U.S. consumers shift, that is going to leave France with a lot of unsold champagne, and they need to sell it someplace else, and that's a problem since the U.S. is a huge high-income market; that’s the reason that it's sought after by so many countries who export to the United States. U.S. consumers may choose to be satisfied with a different product. In this example, the French, or it could be the Germans, or anyone whose exports are distained because of higher prices, might find that they have goods piling up in the shelves that they are not selling. This could cause an unemployment problem that could really snowball - a more severe problem than drinking Chardonnay instead of French champagne!

The U.S. side

On the U.S. side, if people continue to buy these goods, the U.S. will have more inflation that may cause the Fed to stop cutting rates. The Fed might even raise rates, and this could slow the economy down. However, as we know, tariffs are a one-time increase in the price level, and it's only if the Fed runs ‘bad monetary policy’ that the price bump caused by the tariffs would become inflation… inflation is a persisting increase in prices.

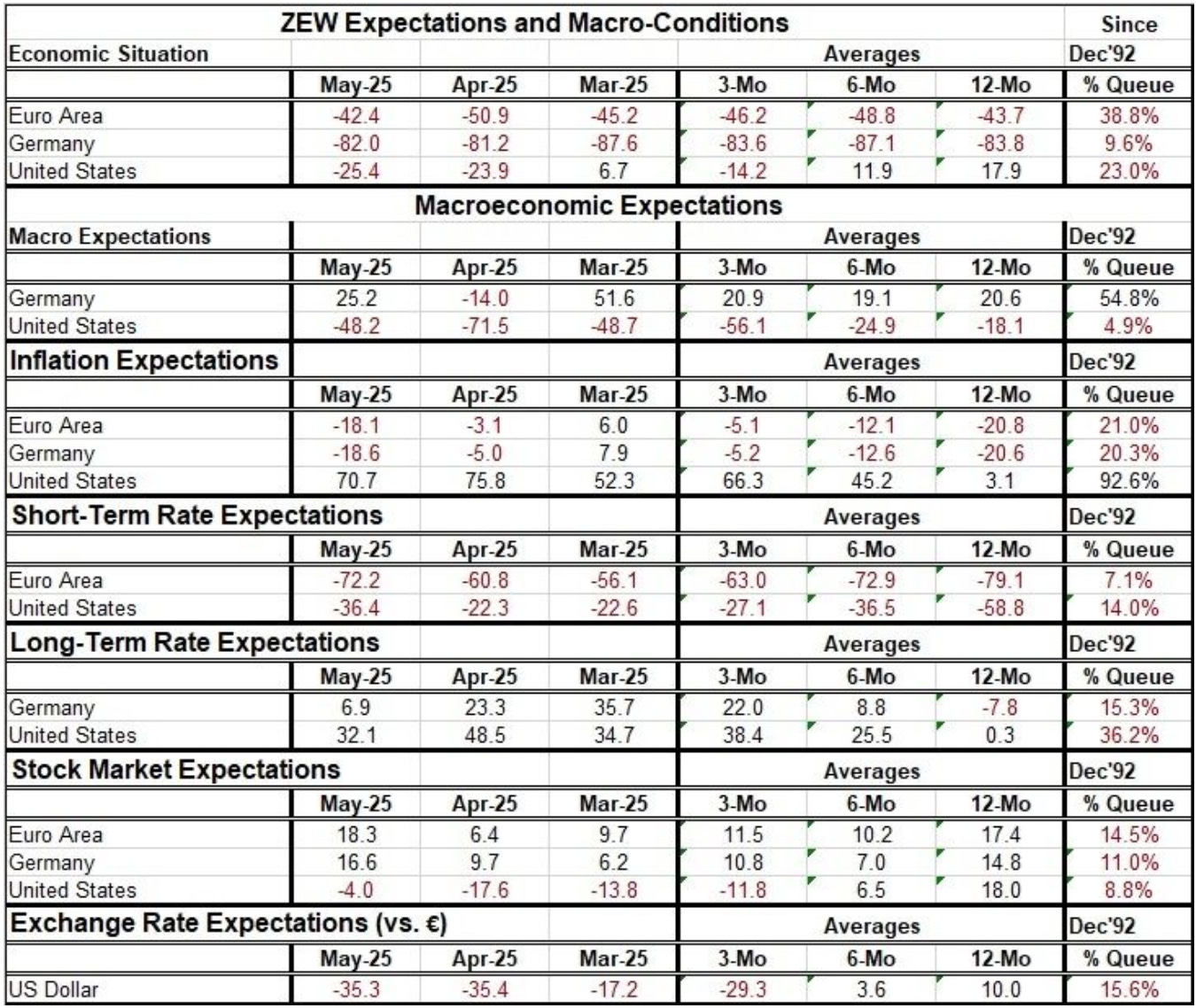

The new ZEW in May

In this new survey, we see the economic situation in May improving relatively substantially in the euro area, as well as worsening slightly in the U.S. and in Germany. We see macroeconomic expectations sharply higher in Germany in May and while they also improve substantially in the U.S., the U.S. is left with economic expectations that are weaker less than 5% of the time, while German macroeconomic expectations are above their historic median (above a ranking of 50%).

Got inflation?

Inflation expectations are falling in the euro area in May and in Germany, and while they edged slightly lower in the U.S., they rank very high - higher only 8% of the time in the U.S. Whereas inflation expectations are lower only about 20% of the time in the euro area and in Germany. What's interesting is that we see a big decline in inflation expectations in the euro area and in Germany despite the fact that growth conditions either improve or hardly change and macro-expectations for Germany get sharply higher, and yet inflation is improving. This has to be viewed as a curiosity.

Interest rates

Short-term rate expectations in the euro area are more negative than they are in the U.S. with both the euro area and the U.S. having low rank standings for short-term interest rate expectations. Long-term rate expectations in Germany and the U.S. show a decline both in Germany and in the U.S., but the German rank-standing is at its 15th percentile and the U.S. standings in its 36th percentile. That, at least, matches with the inflation expectations outlook.

Through all this, stock markets are improving in May compared to April. The European stock market and the German market are doing better than the U.S. on a queue-standing basis. And the dollar is expected to get weaker.