QT and Unknown Outcomes

Macro Perspectives

June 2022 was the official start of the Fed's quantitative tightening (QT) program - this is taking liquidity out of the system.

NB: QT really starts on June 15 - that's when securities above the monthly reinvestment cap start to mature.

The Fed plans to allow the securities they bought at the depths of the pandemic (which injected liquidity into the financial system), to mature from this point forward, without reinvesting the proceeds. With this plan, they think they will extract $1 trillion from the financial system over the next year, and they estimate that a trillion dollars worth of QT will be the equivalent of about a half of a percentage point rate hike.

The Fed first disclosed that they had discussed plans for QT back on January 5th, when they published the minutes from their December meeting. Here's an update of what stocks have done since the minutes hit the wire (back in early January).

So, the anticipation of reversing QE has already contributed to a steep decline in stocks. Now actual QT is officially upon us.

With that in mind, let's take a look at how stocks behaved during the Fed's first experiment in shrinking the balance sheet, following the Great Financial Crisis period (GFC).

Stocks went up!

Over 535 days, stocks gains 22% - this measures the period of time from when the Fed signaled balance sheet normalisation (June 2017), up until the day they ended it (July 2019).

On that note, as we've discussed over the past couple of months, the historical track record of QE exits is not good. We know that in each case (globally and domestically), the "quantitative tightening" experiments ended with more QE. From the chart above, clearly the Fed's return to QE wasn't because of a crashing stock market.

Why did they restart QE back in 2019?

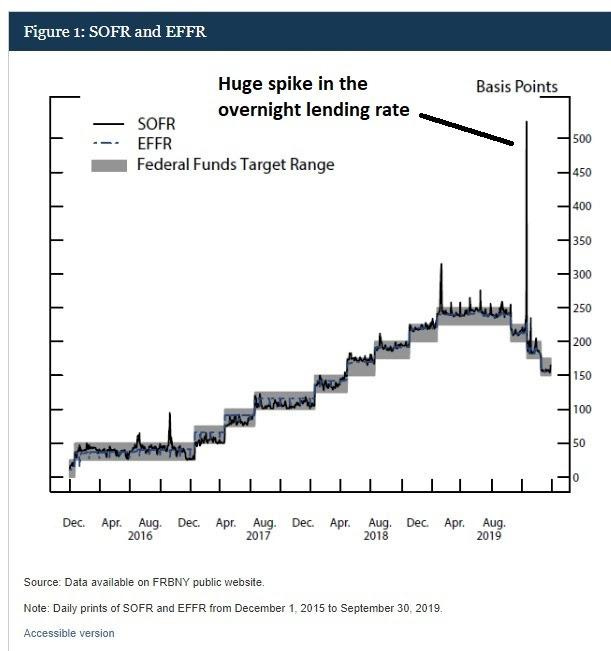

Things started breaking in the financial system. Building on my note from 07 April ( click here ) - we had this 300 basis point spike in the overnight lending market.

Here's how the Fed explained what happened (my emphasis) …

"Strains in money market in September occurred against a backdrop of a declining level of reserves, due to the Fed's balance sheet normalisation and heavy issuance of Treasury securities."

So, the Fed was forced to rescue the overnight lending market (between the biggest banks in the country) because of an unforeseen consequence of balance sheet normalisation.

It's important to understand that reversing the Fed balance sheet is an experiment with unknown outcomes.

Alpha Idea: Investment Long $KAP & $BTU

Thesis: The Stone Age did not end because we ran out of stone; rather the creating of superior products closed the quarries. Similarly, regulations that restrict nuclear & fossil fuel use investment may serve as good public policy over the long-term. However, over the next few years as we navigate the changing geo-political landscape (Russia/Ukraine and whatever may come next), I suspect “traditional energy” earnings will cover their above market dividend and may well have price appreciating via P/E expansion.

$BTU chart shown below: