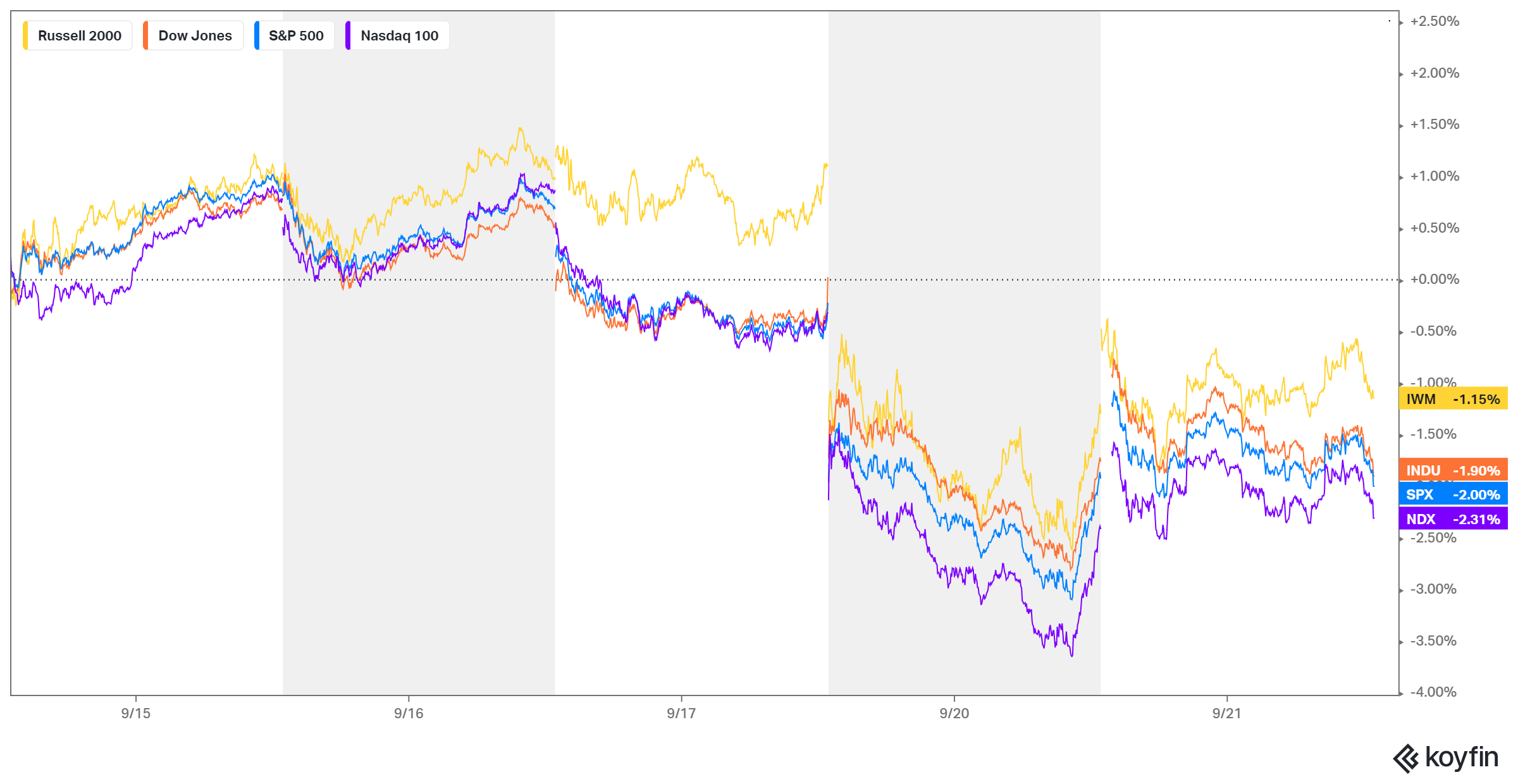

Profit Taking followed by Dip-Buying

Macro Perspectives: Wed 22 Sep 21

Global markets recovered some on Tuesday, after Monday’s price action down. However, this correction (now 5% peak to trough) probably has some more downside.

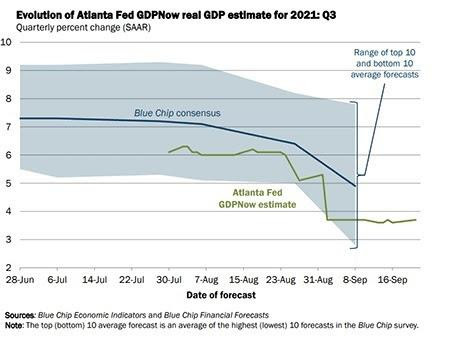

The drama surrounding a failing property developer in China has conjured up some financial crisis speculation. The vaccine mandates have introduced a catalyst for an uptick in unemployment and what has been extremely hot economic activity has softened some in Q3. As you can see Atlanta Fed models have nearly cut the GDP estimate for the quarter in half, since August.

These are all reasons to induce some profit taking in stocks, which we're seeing. But the most meaningful impediment to the asset price melt-up we've seen over the past eighteen months, is the Fed.

We have a change-in-policy-direction anticipated in today’s Fed announcement - the knee-jerk reaction in markets when the Fed changes directions (from easing to tightening) is selling.

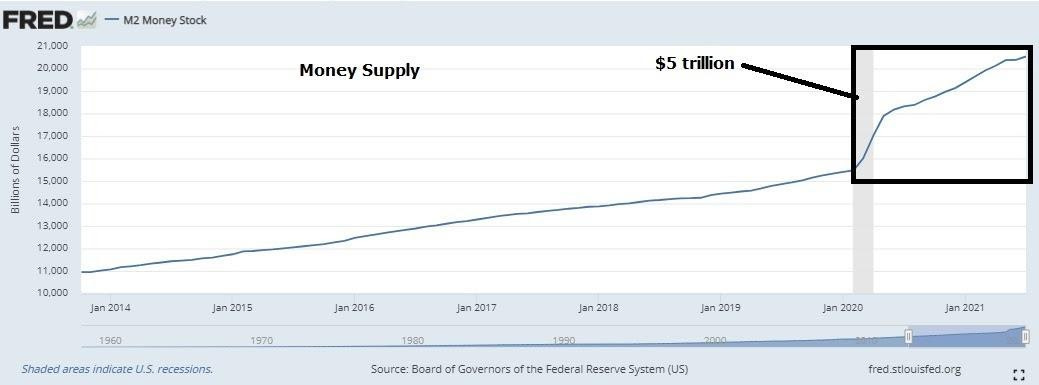

But, of course, this is a change of monetary policy direction with no reference points (not even the financial crisis). Beginning-the-end of QE, will still leave us with zero rates for quite some time and, as we discussed, we have a fiscal bazooka ($4.7 trillion) that will be fired soon. And we have this...

There is five trillion dollars of new money in the economy, with both monetary and fiscal policies still in a defensive position, against any destabilising events. Plus both monetary and fiscal policies are still heavily promoting spending, not saving. That makes the dip in stocks a gift to buy at lower prices.