Productivity Outpacing Wages

Macro Perspectives

We are in the early days of what may be the most productivity enhancing technological advancement of our lifetime, in generative AI.

Q3 productivity data was reported yesterday - it was big, at 4.7%. That follows productivity gains of 3.7% (annual rate) in the second quarter. For perspective, we averaged less than 1% productivity growth for the decade prior to the pandemic.

These hot productivity gains create the opportunity for the continuation of much needed wage gains (to restore living standards, which have been eroded by inflation).

However, despite some of the hottest wage gains we've seen in decades, the annual growth in the cost per unit of output last quarter was actually negative (-0.8%) - this means wage growth is more than being offset by productivity gains.

That means increasing wages are not a problem in the inflation picture. Jerome Powell admitted as much.

So, we're in the early stages of a productivity boom. That's great news. Guess who presented on the importance of productivity growth as a driver of the long-term potential growth rate of the U.S. economy? Jerome Powell did, back in 2016 (here).

This all supports the path of both economic growth (hot) and inflation (falling).

With the above in mind, we've talked about the reversal signals in the bond market. With the Fed meeting now behind us, and the increasing likelihood that the next change will be in the direction of interest rate policy, yields continue to slide…

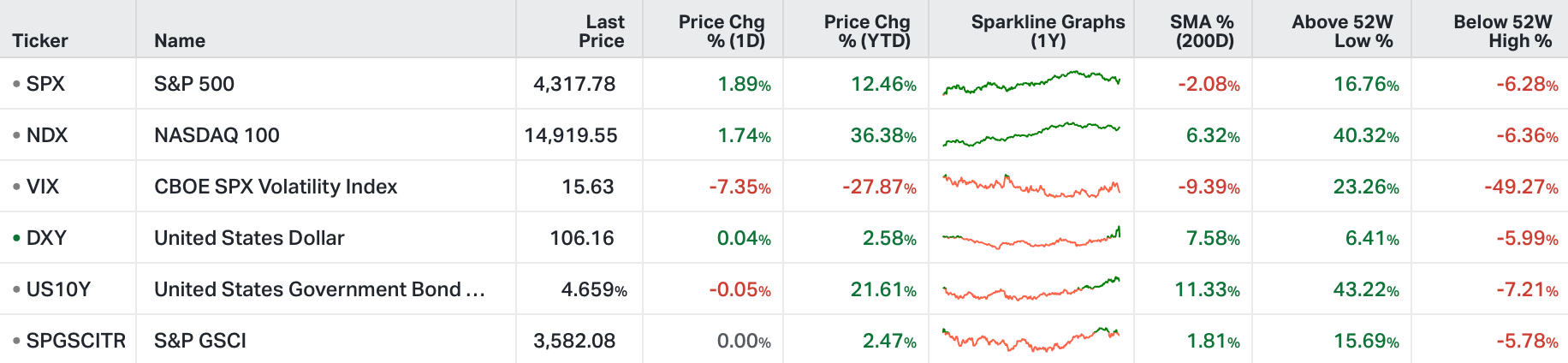

Stocks had a big day. The S&P is now trading back above the 200-day moving average. But small caps offer the big rebound opportunity - declining as much as 33% over the past two years, and currently down 2% year-to-date.

Thanks for reading The Gryning Times, have a great weekend.