Productivity Catching Wages

Macro Perspectives

We previously talked about the Nvidia earnings.

For the second consecutive quarter, they delivered shockingly big numbers, and CEO Jensen Huang delivered an education to the analyst community on the global transition to "a new era of computing," and the related trillion-dollar retooling of the world's data centers (from CPUs to GPUs).

That said, the stock gave up all of the post-earnings gains by the close yesterday. Concerning? For perspective, Nvidia is a trillion-dollar company now, but growing at a better than 100% annual rate, with 80% share of a new trillion-dollar market opportunity. If we look at Amazon, they developed the (new) cloud business (AWS) over the past decade, growing it at a 50% annualized rate, and the stock went up nine-fold.

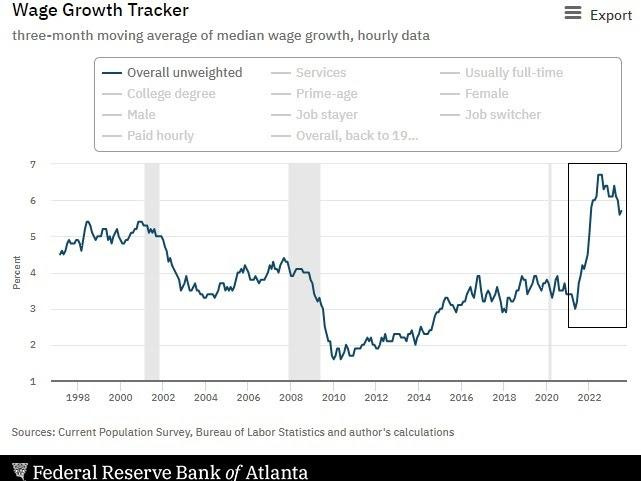

Building on our discussions over the past quarter, this (gen AI) technological revolution is productivity enhancing for the economy. It's a formula to grow the economic pie (and the size of the stock market). With that, productivity gains create the opportunity for much needed wage gains (to restore quality of life, which has been eroded by inflation).

We averaged just 1% productivity growth for the decade prior to the pandemic, and negative 0.7% since the fourth quarter of 2020. The most recent productivity growth report came in at 3.7% - thats a big deal as wages have been (relatively) hot.

This wage pressure is precisely why the Fed has focused on jobs in this inflation fighting cycle. Powell has talked endlessly about the mismatch between the number of job seekers and the number of job openings.

The concern? With leverage in the job market, job seekers and employees can command higher wages. The Fed has feared an upward spiral in wages, where wages feed into higher prices (inflation), which feeds into higher wages . . . and so the self-reinforcing cycle goes.

That said, we need wages to reset (higher) to the (higher) level of prices, not the other way around. A fall in prices to restore buying power would lead to a deflationary bust (low or contracting economic activity and falling prices) - that scenario is far worse than high inflation.

A deflationary bust is vulnerable to a self-reinforcing spiral, and very difficult to escape (ask Japan). It's far more dangerous, given that we've already exhausted two deflation-fighting tools: government spending, and expansion of the Fed balance sheet.

With all of the above in mind, while wages have indeed been on the move, we are already getting an offset from productivity gains. The cost per unit of output last quarter was just 1.6% - that's lower than the average unit labor cost of the 20-year period prior to the Global Financial Crisis.

The Fed should be very happy with the prospect of a productivity boom. We'll see if that factors into the messaging today at the St. Louis Fed economic symposium at Jackson Hole. As I've said, this event has a history of signaling policy adjustments.

PS: I have received inquiries regarding the AI Investment Portfolio - membership was limited to 100 and we are fully subscribed.

To access a fully comprehensive, quantitatively analysed, stock & etf breakdown of the Technical, Fundamental and Sentiment factors, affecting future ticker price’s - Click on the button below.