Productivity & Compensation

Macro Perspectives: Mon 20 Dec 21

It looks like the Fed guidance last week served as confirmation of the end of globally coordinated easy money policies.

The question is how aggressive will the tightening cycle be?

Thus far, the Fed wants us to believe that the cycle won't be aggressive. To justify that, they keep our eyes on the supply chain disruption as the only factor driving inflation. They say it will ultimately normalise.

In their outlook, they ignore $5 trillion of new money supply created over the past 20 months, whilst also ignoring the wage growth, which is hot, and sticky (going higher, and will stick).

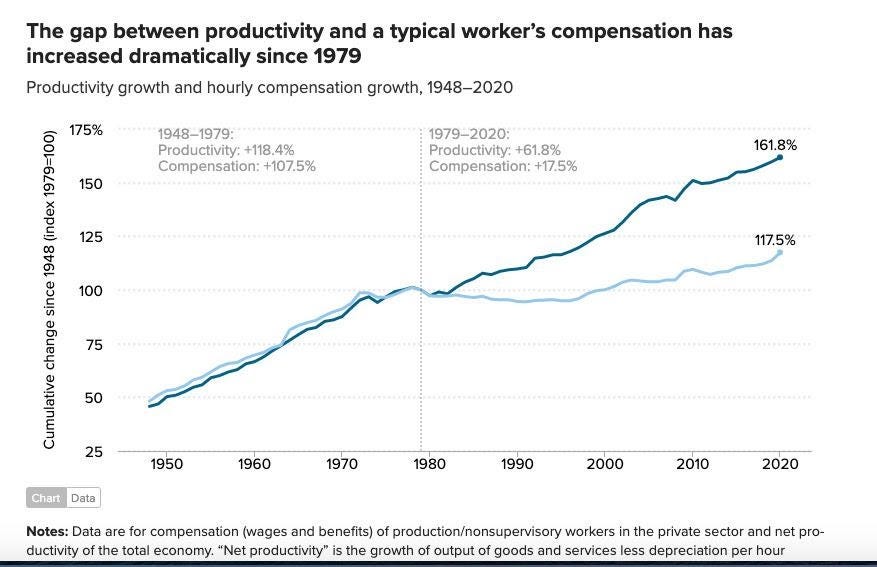

With that, let's take a look at this chart of wage growth vs. productivity...

As you can see, over the past forty-years, each hour of work generated far more income for all stakeholders, than it did for the average worker. Translation: The lion's share went to the few.

But this productivity/pay gap is about to narrow, thanks to hazard pay through the pandemic, overly generous and lengthy federal unemployment subsidies, and (subsequently and consequently) an imbalanced job market (more jobs than job seekers). Wages are going up, fast.

With that in mind, the gap in the above chart gave us nearly four decades of falling inflation and falling interest rates. Logic would tell us that rising wages and a narrowing of the wage/productivity gap will fuel the opposite.