Potential Pain

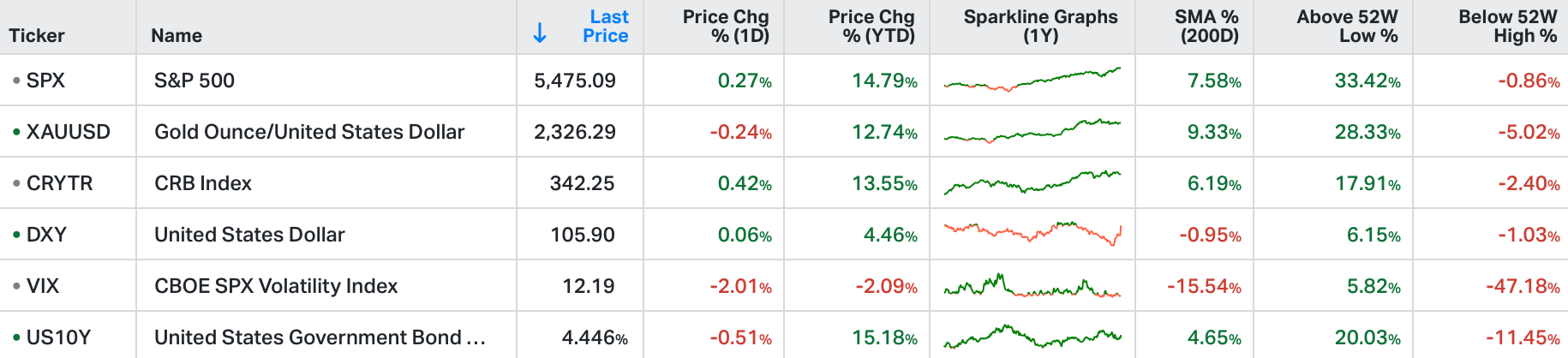

Stocks in the US closed higher to start the second half of the year.

The S&P 500 gained 0.3%, the Dow Jones added 50 points, and the Nasdaq rose 0.8% thanks to strong performances from tech giants like Apple (+2.9%), Amazon (+2%), and Microsoft (+2.2%).

Tesla notably surged 5.9%, while Meta booked marginal gains despite regulatory concerns in the EU regarding its ad-free services model on Instagram and Facebook.

On the data front, the ISM Manufacturing PMI showed a faster contraction in the manufacturing sector, with demand and employment declining while price pressures eased.

This week, traders monitor several other key indicators due this week to assess the economic performance and the monetary policy outlook, including the jobs report, JOLTS, and the ISM PMI, together with FOMC minutes.

Last week we talked about the potential for pain in sovereign bond markets if the government policy pendulum swings, from the globally coordinated climate agenda, to a more nationalist agenda (under leadership change) - given that trillions of dollars of deficit-funded investment in the climate agenda could be abandoned.

After Thursday night's U.S. Presidential debate, the bond market did indeed react.

The U.S. ten-year yield is 20 basis points higher than it was pre-debate.

In France, the elections have gone as anticipated, in favour of the nationalist party (Le Pen).

Yields across Europe were up.

As for the U.S., the narrative behind rising yields is that both candidates are fiscally profligate - both will lead to higher deficits. And if anything, they say Trump policies will be more inflationary.

But as we've discussed, the result of a policy swing, from the globalist agenda to a more nationalist agenda (in both the U.S. and France) would simply mean that the massive deficits and record indebtedness pursued to fund a radical transformation agenda (in both countries) would be abandoned. For the funding that can't be clawed back or redirected, it would be a returnless investment.

And that, my guess, would be penalised through higher bond yields - until the market gains confidence in a turnaround plan.