The minutes from the May Fed meeting were released yesterday.

It was three weeks ago that the Fed made its second rate hike, and started what now projects to be a series of 50 bps rate hikes (probably three consecutive by July). From the meeting, they announced details on a quantitative tightening plan (i.e. reversing QE) - that's due to begin June 1.

This was all within the context of what the Fed described as a "very strong economy," "extremely tight labor market," and "very high inflation."

Since then, stocks have made new lows, gas prices have made new highs, rents and the cost of home ownership have continued to rise…Financial conditions have tightened. And with that, consumer psychology is changing.

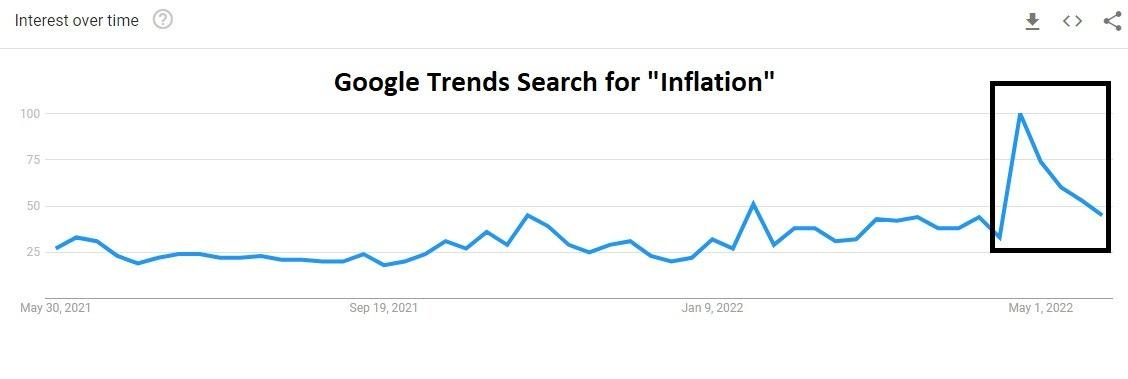

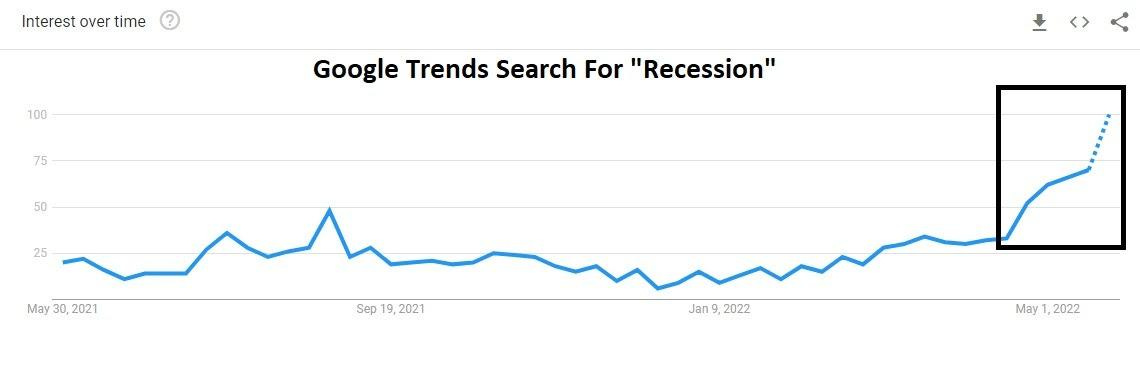

When the Fed last met, inflation was top of mind. Now it's this ...

This brings us back to my prior notes, where we've discussed the power of the Fed's tough talk.

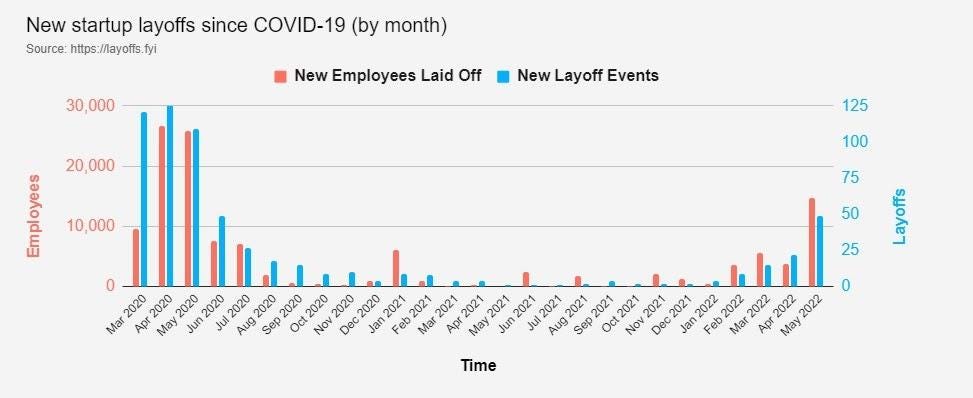

Back in March, Jay Powell explicitly said they were trying to better align demand with supply (i.e. bring demand down). Within that strategy, they have explicitly said they want to narrow the job opening to job seeker gap (which has been 2 to 1). As a proxy, this chart of layoffs in startups are happening (narrowing the gap)...

So, just months after telling us they want to bring demand down, the switch seems to have been flipped (per the charts above) - they haven't even gotten the effective Fed funds rate to 1% yet and they haven't even started their QT program.

But they have achieved the goal of knocking down animal spirits, curtailing inflation expectations, and extracting liquidity from the system (in the form of lower equity market valuation).

If we consider that, we have a Fed that should have the comfort to sit back and watch the inflation data come down. This is a slow down scenario, and it has been quick, but this is not the Volker-like inflation-fighting scenario (and hard landing).

It presents the very real possibility that the tightening effect from a stock market decline, high gas prices and an adjustment in mortgage rates, could be enough to bring inflation under control (without requiring sharply higher interest rates). This should be seen as positive for stocks.

With that, the S&P 500 sets up for a test of a trendline today (in the chart below). A break and close above 4,000 would be bullish, and give us a chance to see a break of the string of seven consecutive down weeks, each having had lower lows along the way.

PS: The Gryning Portfolio offers a nuanced approach to gaining equity market exposure. Subscirbe below for trading recommendations with a strong track record.