Overreaction

US Stocks closed significantly lower on Wednesday, as hopes that the Fed might start cutting rates any time soon waned following another hotter-than-expected inflation print.

The S&P 500 declined 0.9%, the Nasdaq fell 0.8%, and the Dow Jones plunged by 422 points.

Besides the energy sector, all sectors ended in the red, with real estate posting the biggest decline.

On the corporate front, megacaps including Microsoft (-0.6%), Apple (-0.9%), Alphabet (-0.2%) and Tesla (-2.7%) were lower while Nvidia gained 2%.

Meanwhlie, Delta Air Lines pared earlier gains of 4% and finished 2.2% lower despite surpassing earnings predictions.

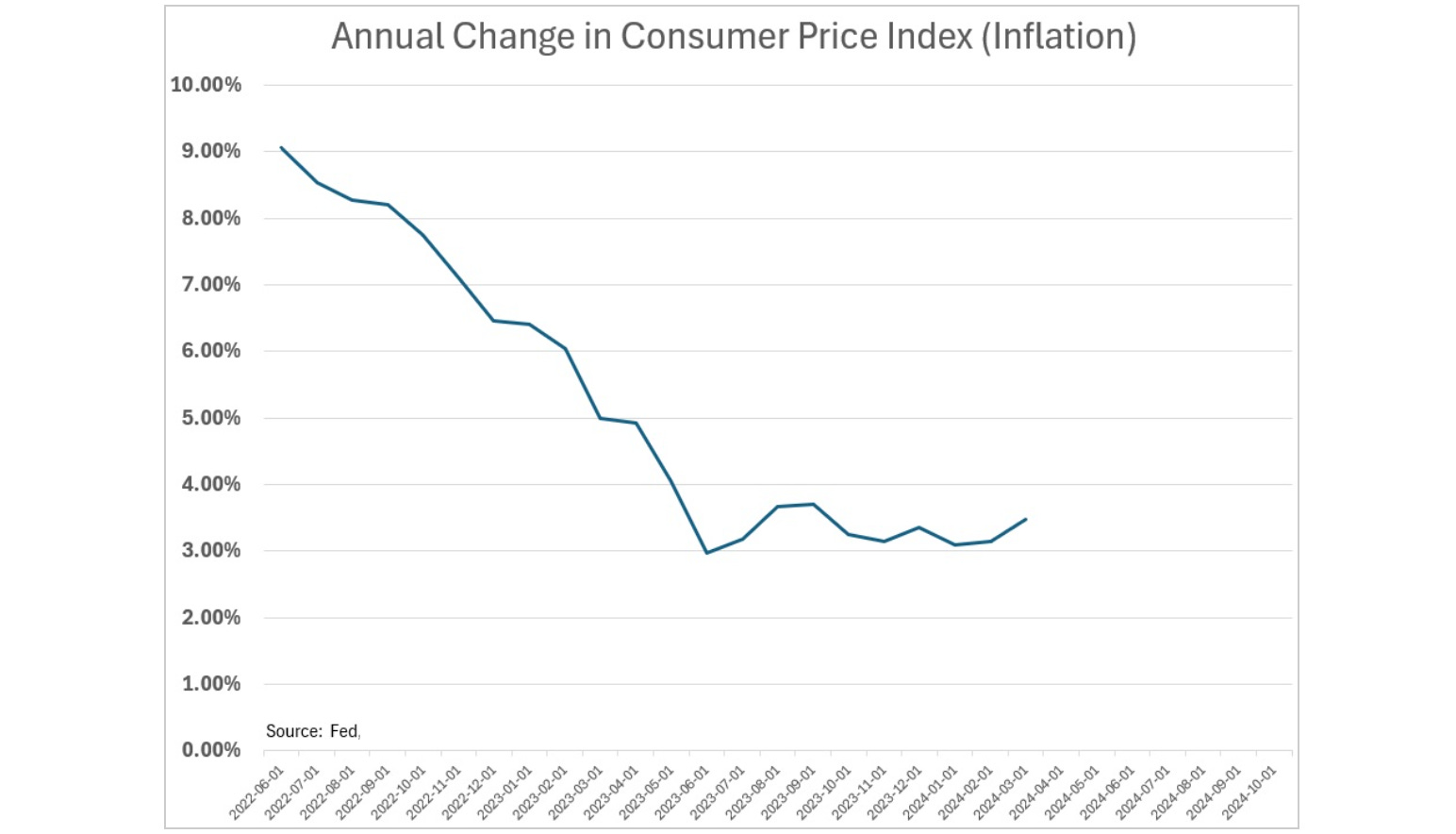

There was a lot of fuss about the inflation data - March CPI came in a tenth of a percentage point hotter.

Stocks were crushed. Yields spiked. Dollar rallied.

This reminds me of the inflation report back in February (the January inflation data). Similar to yesterday's report, both the headline and core inflation came in a tenth of a percent above expectations. Stocks were crushed. Yields spiked. And the dollar rallied - all of a magnitude similar to yesterday’s market response.

With that, back in my February 14th note ( here ) we discussed what looked like a clear overreaction, given the magnitude of the decline in stocks, rise in yields. And we looked back at the only two times, over the prior three years, that shared the features of 1) a down greater than 4% Russell 2000 and 2) at least a 14 basis point spike in the 10 year yield.

Let's revisit that analysis …

25 February 2021.

It was about inflation. The 10-year yield had risen from 1% to 1.6% in less than a month, and the move was quickening. This quickening was driven by the market's judgement that the additional $2 trillion fiscal package coming down the line from the new President and his aligned Congress was inflationary at best, and recklessly extravagant, at worst.

The $2.2 trillion Cares Act and the additional $900 billion in stimulus passed in December, before Trump's exit, had already driven a nearly full V-shaped economic recovery (by late January '21). The economy was projected by the CBO (Congressional Budget Office) to grow at a 3.7% annualised rate in 2021 (hotter than pre-pandemic growth), with an unemployment rate falling to 5.3% - about right at the average unemployment rate of the past 50 years.

The prospects of more, massive spending packages was an inflation bomb.

13 June 2022.

It was a Monday meltdown, following a hot Friday inflation report. The Fed had just started tightening and was way behind the curve. Inflation was near 9%, the Fed Funds rate was below 1%. With a Fed meeting just days away, the market ratcheted up expectations for an aggressive 75 basis point hike. History suggested they needed to take rates a lot higher in order to stop fueling inflation, and start curbing it.

So, in both cases (Feb of 2021 and June of 2022) stocks fell sharply and yields spiked on significant inflation fears. It's fair to say the circumstances are quite different today. And you can see it in the chart below …

This is the continuation of the "stall" in inflation progress we discussed yesterday. It's not a Feb 2021 or June 2022 "significant inflation fear" moment, far from it.

As we know, in the current case the stall in CPI is largely due to a couple of hot spots in the data (shelter and insurance). On the latter, the auto insurance component was up 22% year-over-year in the March inflation report. Just pulling that out, the headline CPI drops below 3%.

Bottom line, Fed policy remains "highly restrictive" (in the Fed's words). The next move by the Fed will (still) be easing - it's a matter of when and how much.

Yesterday's overreaction presents another opportunity to buy a dip in bonds.