On a Tear

Both the S&P 500 and Dow Jones hit record highs on Wednesday, climbing 0.7% and 1%, respectively, while the Nasdaq gained 0.6%.

Investors assessed the latest Federal Reserve minutes and braced for key inflation data.

The Fed’s September meeting minutes revealed a "substantial majority" of officials supported a significant 50-basis-point rate cut, but left future cuts uncertain, causing some traders to raise the odds of the Fed holding rates steady in November to 21%.

Tech giants like Apple (1.7%), Amazon (1.4%), and Microsoft (0.7%) led the market higher.

The rally helped offset concerns around Alphabet, whose shares fell 1.5% after the US Department of Justice suggested it may ask a judge to force Google to divest key businesses, including its Chrome browser and Android operating system, to address its monopoly in search.

We talked about the interview with Jamie Dimon yesterday, and his expectation that we will see more episodes of volatility in the Treasury market, driven by the Fed's quantitative tightening (QT).

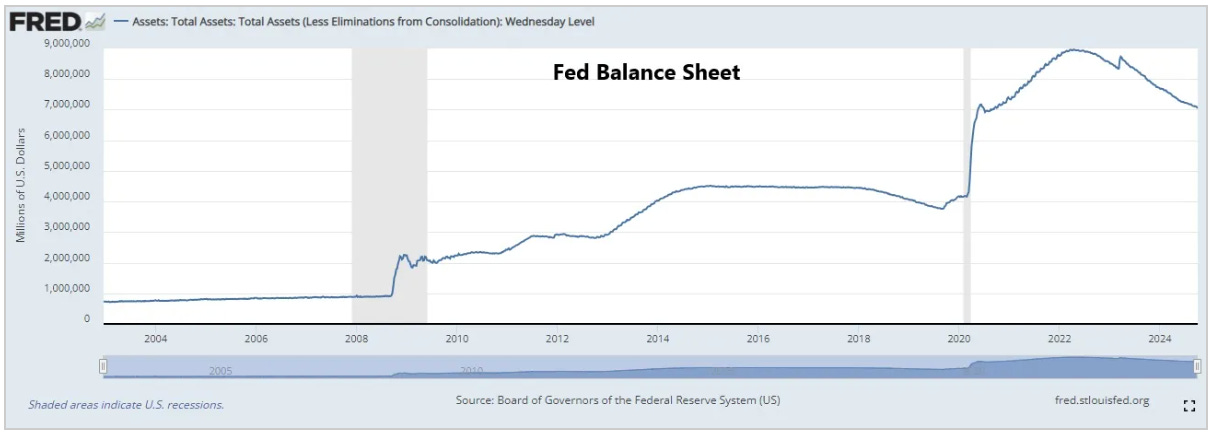

The Fed's minutes were released from its September meeting, where they decided to start the easing cycle with a larger than expected 50 basis point cut. They said nothing to change the ongoing reduction of the Fed's balance sheet (QT).

As you can see in the chart above, the Fed has reversed nearly $2 trillion of the securities it added to its balance sheet in the Covid QE response.

That said, in line with the commentary from Jamie Dimon, most of the major bank economists came into the year expecting the Fed to end QT between this past summer and the first quarter of 2025 — with the concern of doing so before any signs of stress emerge.

So far, no signs of stress translates into record highs for stocks.

With that, let's take a look at the divergence (yellow box) developing again between small caps (the Russell 2000) and the big tech led, cap-weighted S&P 500.

If we look back at the last two months of 2023, when Jerome Powell signalled the end of the tightening cycle, the Russell 2000 (small caps) went on a tear — rising 24% by year end.

Now we have the easing cycle officially underway, and yet the underperformance between small caps (pink line) and the S&P on the year is double-digits.